Should I Roll My 401(k) Into an Annuity?

As you head into retirement, you need lasting income that keeps up with rising costs, just when safety seems paramount.

Enter the insurance industry’s favorite silver bullet: a variable annuity that pairs an income guarantee with the potential for appreciation. “Grow your income without worrying about downturns,” a VA pitch from Prudential goes.

The money you put in, invested in stock and bond funds, builds until you start collecting checks, after which time your withdrawals are guaranteed not to fall below a certain level. Today for a 65-year-old those levels are typically 4.5% to 5% of your balance when you start taking money out. With a guaranteed investment return—a common feature—your balance could be higher for the purposes of calculating withdrawals (but not for cashing out). The problem is, you could pay well above 2% a year in investment and other fees for an annuity with those perks, and the guarantees have gotten considerably less generous since the financial crisis forced insurers to make good on them.

Investors nevertheless poured $141 billion into variable annuities last year, with more than three-fourths of that sum going into annuities with such guarantees.

A Better sales tool

VA sales dwarf those of a far simpler, cheaper, and, for most people, better alternative. With a traditional single-premium immediate annuity, you pay a lump sum to get a lifetime income but give up access to the money. That’s a tough sell for advisers. “To say we’re going to give you a check every month for the rest of your life and that’s it—it’s a hard discussion,” says Jeremy Alexander, president of industry researcher Beacon and a former financial planner.

It’s also not as lucrative a proposition. Sales commissions on variable annuities run as high as 6%, according to the Aite Group. Payouts on fixed annuities typically top out at 4%. “Advisers pay attention to the products that maximize their pay,” says Aite analyst Todd Eyler.

Insurance companies can potentially make out better by selling VAs too. Most U.S. insurers don’t break out the difference between what they earn and what they expect to pay out—what’s known as the spread. Jackson National, the largest seller of individual annuities by assets, however, is owned by a company in the U.K., where insurers disclose more. Based on the numbers Jackson does release, Morningstar analyst Vincent Lui estimates that Jackson’s spread on variable products is 3.8%, vs. 1.5% on fixed ones. (Jackson declined to comment.)

Best Moves

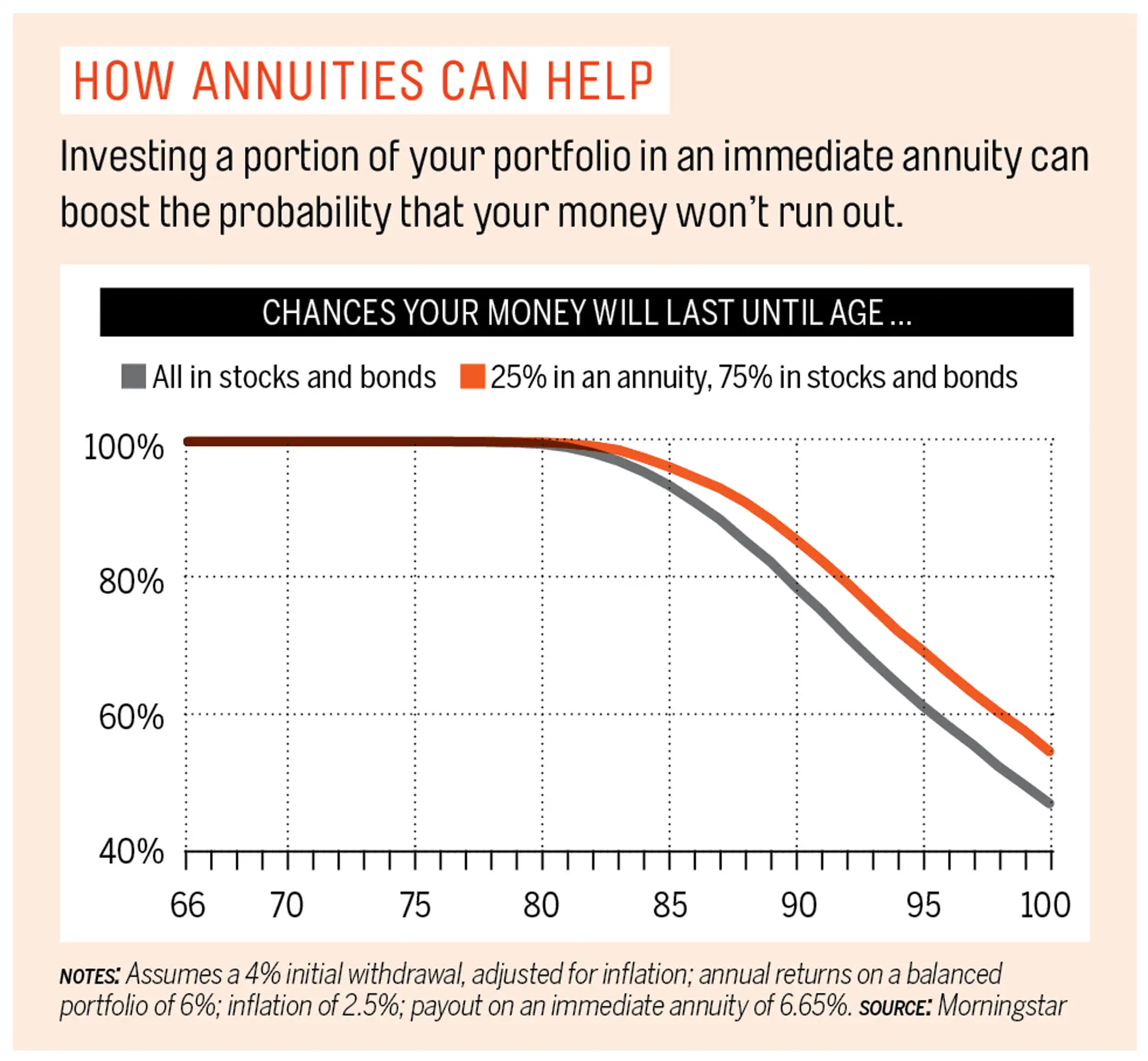

— Keep it simple. To help ensure that your money lasts, opt for a low-cost immediate annuity that, along with Social Security and any pension, will cover fixed retirement costs. You can price them at immediateannuities.com. Today a 65- year-old New York man can lock in $591 in monthly income for $100,000. You can then invest the remainder of your portfolio in low-cost mutual funds or ETFs. Academic research shows that pairing a fixed annuity with stocks can top a VA.

— Shop on price. If, on the other hand, you’re sold on the notion of guaranteed income with a chance for growth, aim to pay no more than 1.5% of assets a year for a VA, says David Blanchett, head of retirement research at Morningstar Investment Management. Once fees top 2.5%, you’re likely to be paying more than the income promise is worth. Start at low-cost providers such as Vanguard and Ameritas.