Big Bank Fees You’re Paying Now

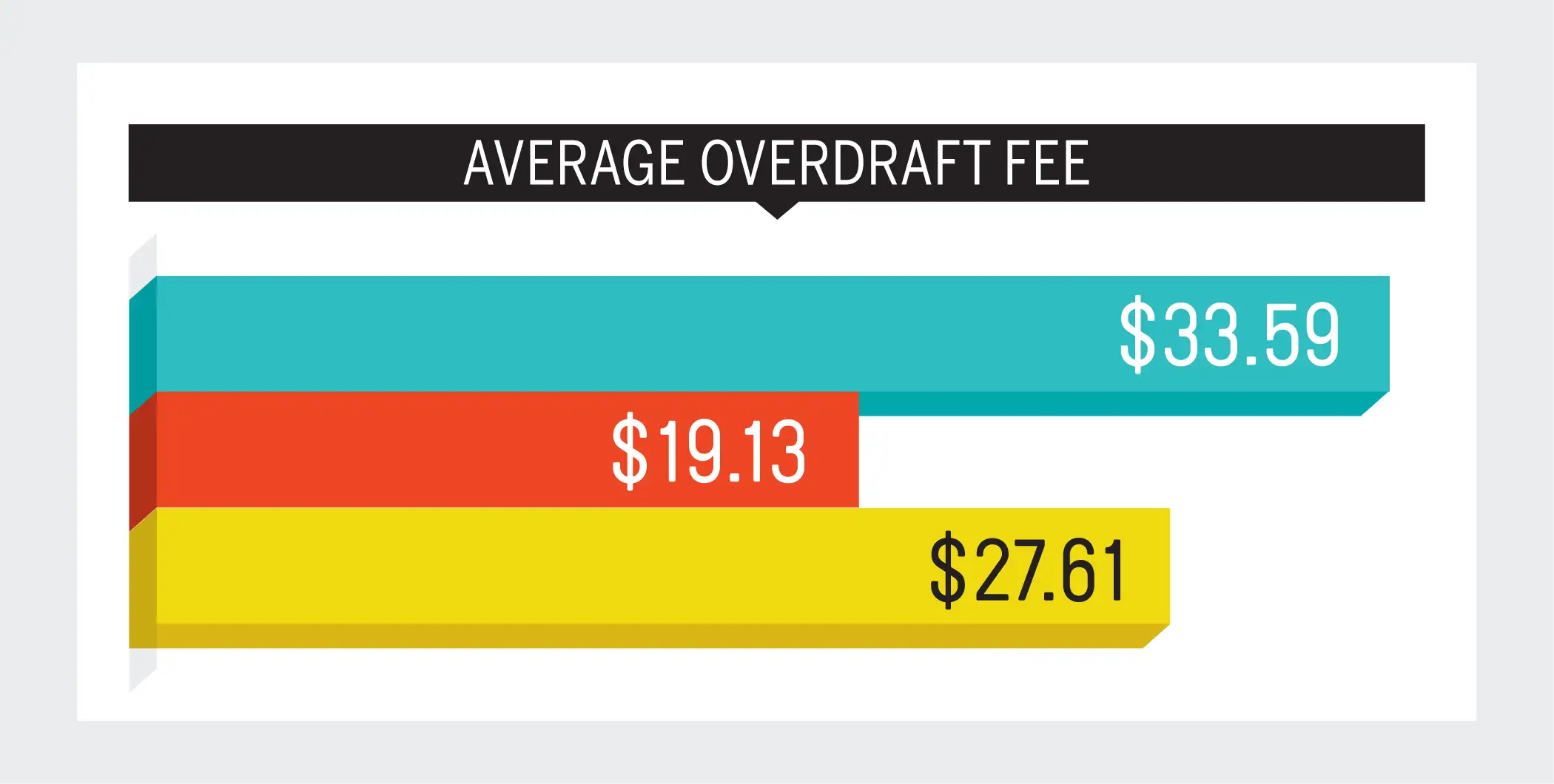

With interest rates low across the board, it's now fees that can have the greatest impact on your account balance at any given bank. To get a sense of what customers are paying now, consider this: Last year, the three largest U.S. banks—Bank of America, Wells Fargo, and JP Morgan Chase—made $6 billion in ATM and overdraft fees alone.

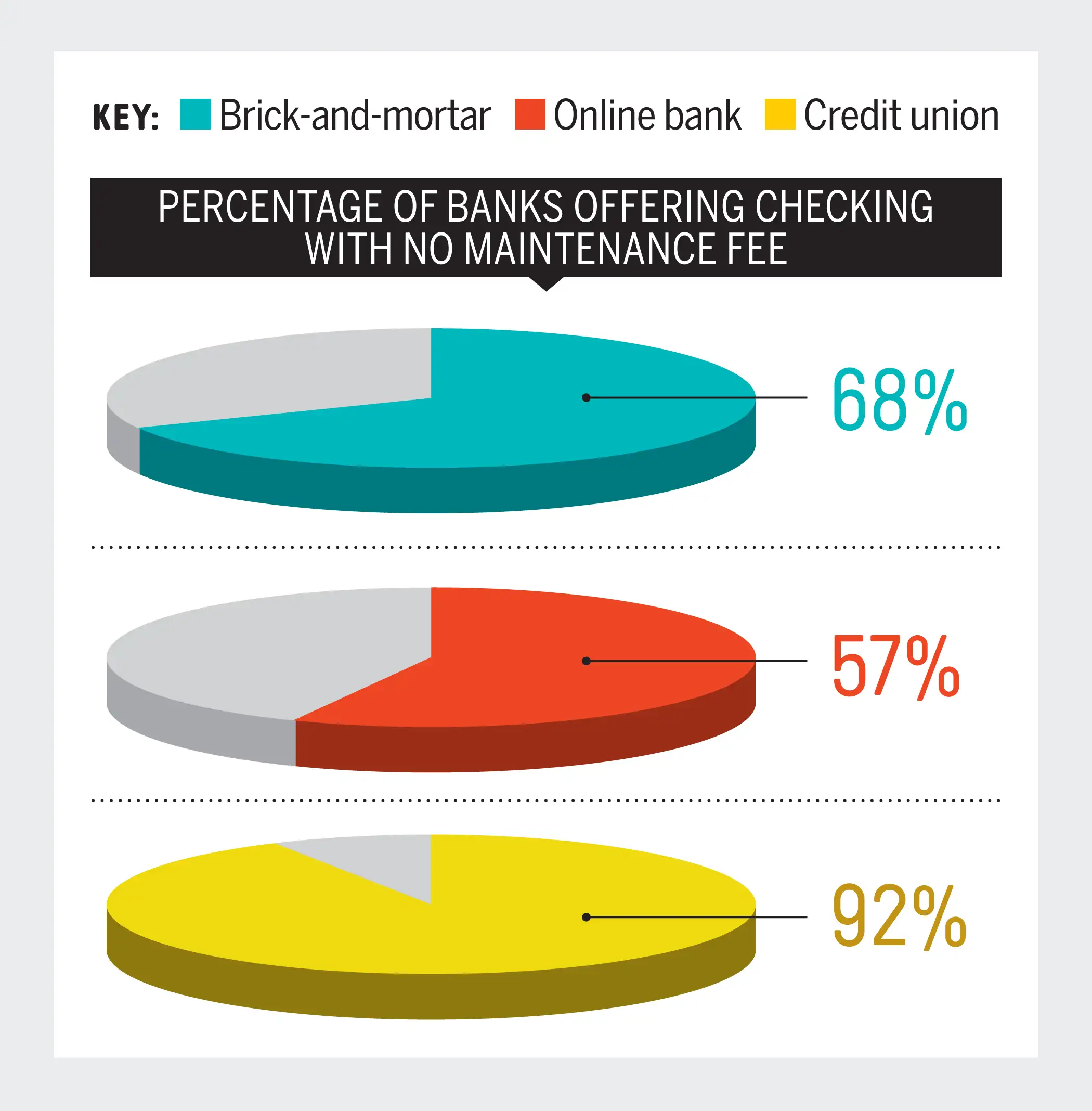

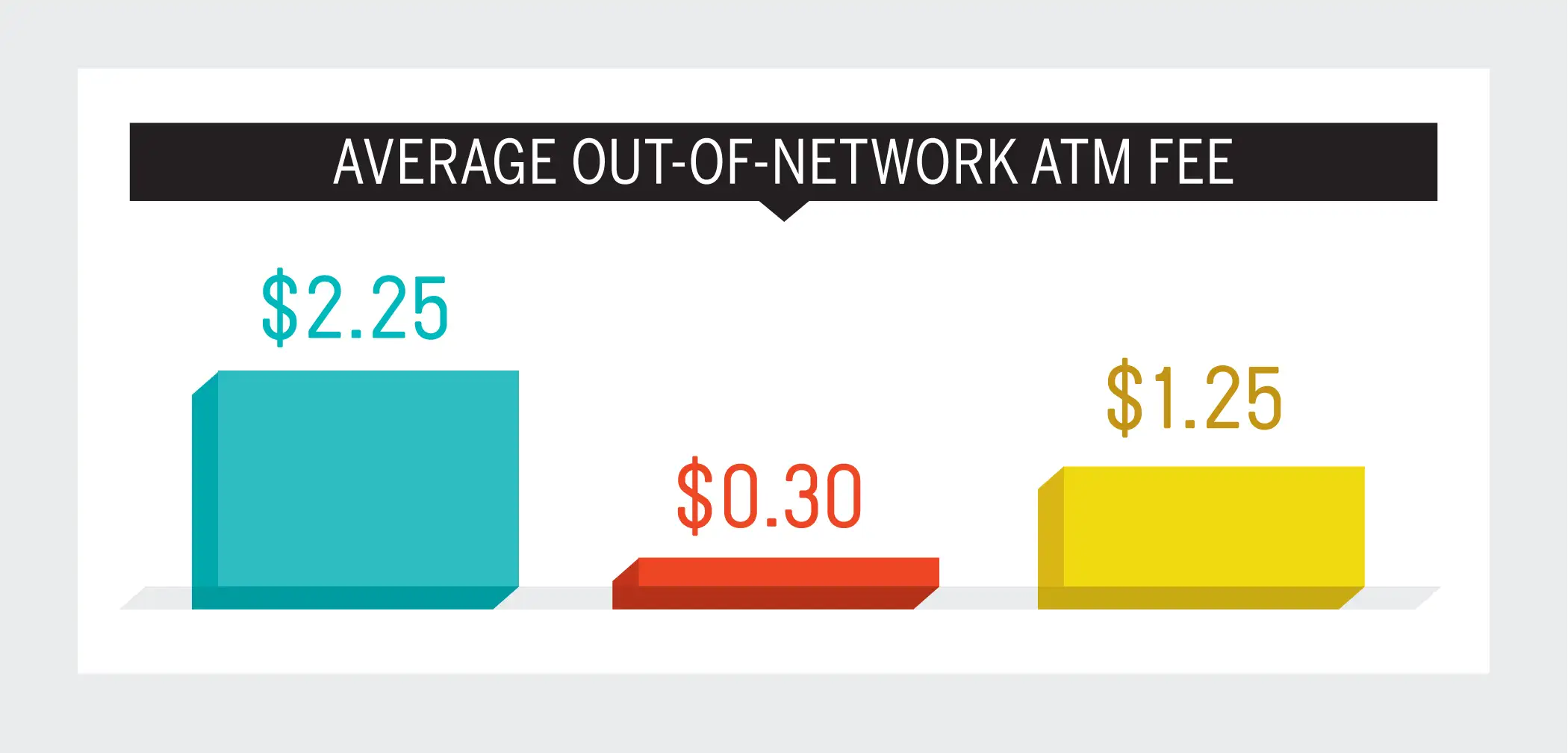

No one should have to pay these—that’s why Money’s annual Best Banks analysis takes a serious look at what your bank charges you. All of Money’s winning banks had to offer a checking account without a maintenance fee, or one that was waived with no more than a $5,000 average balance. We also prioritized banks that don't charge outside ATM fees, or reimburse some of those fees each month.

Fees may be out of control. But, with Money’s help, you can avoid them.