5 Ways to Power Up Retirement Planning in Your 40s and 50s

At every stage of your journey to retirement, you need to know the essential money moves you should be making, the savings target you're aiming for, and the ideal mix for your investment portfolio. Between when you start out and the pre-retirement red zone, those checkpoints change. In your peak earning years, take these steps to adjust your course and set yourself up for comfortable retirement.

1. Saving and Investing: Capture big ticket savings

Why it's key • Once you hit 50, you can make catch-up contributions to your retirement plans: another $6,000 in a 401(k) in 2015, and $1,000 in an IRA.

How to do it • A new Center for Retirement Research study found that after children leave home, retirement savings barely go up. Enjoy some of your newfound cash, but also increase your 401(k) contribution or set up automatic transfers to an investment account.

2. Work: Master an in-demand skill

Why it's key • Pay for women peaks at age 39 on average, and age 48 for men, according to PayScale. To keep moving up (and making more), demonstrate that you are continuing to build expertise.

How to do it • Scan job listings in your field to ID valuable skills you need to learn. At Coursera, you can earn a certificate in social media marketing from Northwestern University ($79) or a business analytics certificate from the University of Pennsylvania ($95).

3. Planning: Hold out for tax savings

Even 10 years from retirement, a Roth IRA or 401(k) can beat the upfront tax savings of a traditional IRA or 401(k). You get no tax deduction now, but all your earnings are tax-free—even when you withdraw them in retirement. That's a powerful advantage. According to an analysis by T. Rowe Price, picking a Roth over a traditional IRA at age 40 can give you 14% more income in retirement if your tax rate stays the same (the study assumes a 25% bracket). If your tax rate drops by 5%, you still get a 7% boost with a Roth. At age 50, picking a Roth can mean 11% higher income if your tax rate is level, and 4% more if your tax rate falls by 5%.

4. Lifestyle: Resolve to live healthier

Why it's key • A National Bureau of Economic Research study found that those who were among the healthiest 20% in their fifties retired with three times the assets of the least healthy. Plus, you'll pay less for health care each year if you head into retirement reasonably fit. The average annual health care cost for a 65-year-old in excellent health is $4,450, vs. $4,760 for someone in poor health, according to HealthViews, and that gap rises with age.

How to do it • No need to be a gym rat. Just 2½ hours of moderate exercise a week can do the job, the Centers for Disease Control and Prevention reports.

5. Mindset: Ignore the Joneses

When it comes to retirement saving, peer pressure may be powerless. A recent study in the Journal of Finance found that knowing how your nest egg stacks up against your co-workers' doesn't motivate you to save more. In fact, it can backfire. According to the researchers, learning that you are behind your peers is discouraging and tends to lead you to simply ignore the problem.

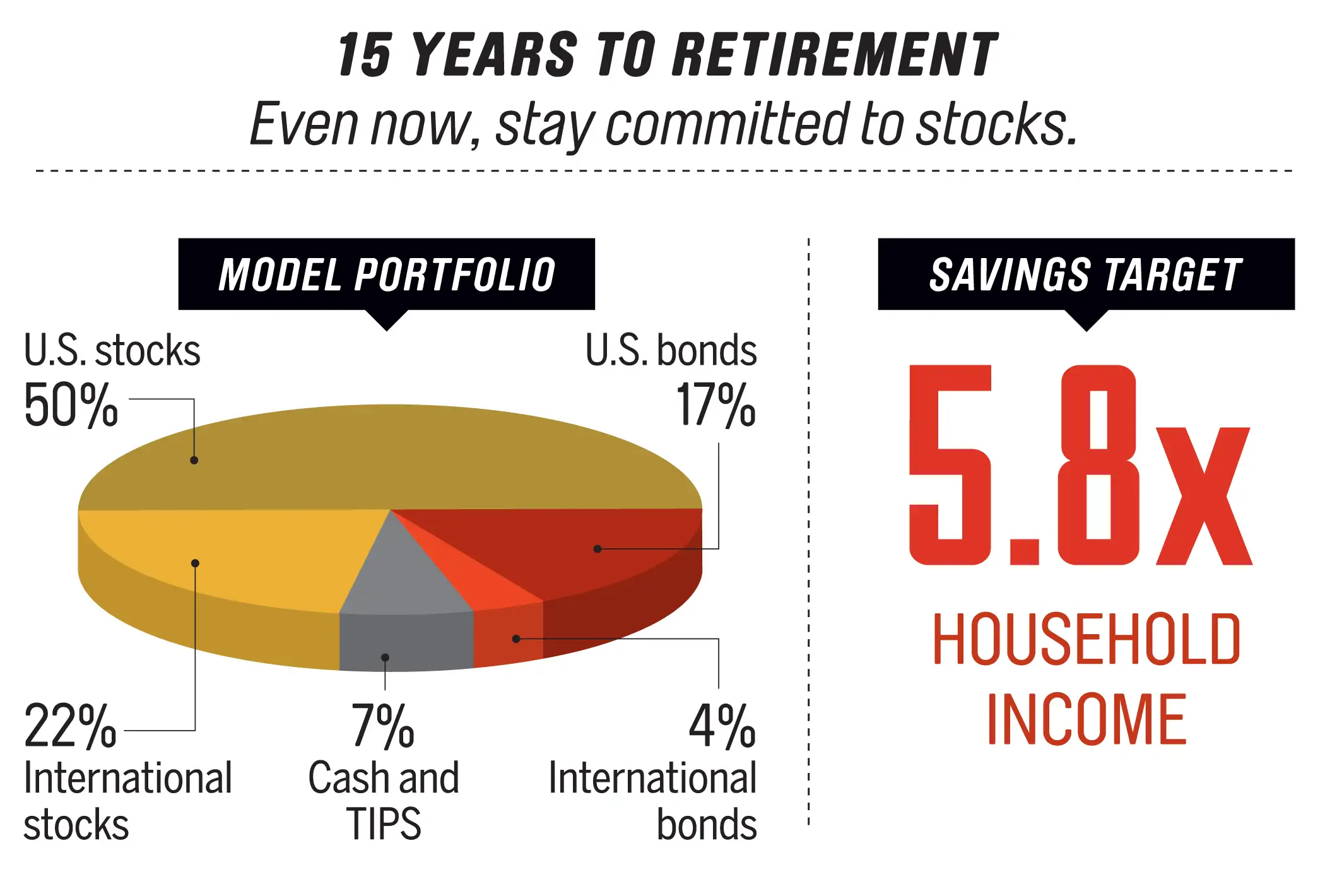

Once you've made these five moves, you should be squarely on track. To double check how you're doing, use these benchmarks to measure your progress:

Notes: Savings rate assumes retiring at 66, replacing 75% of your pre-retirement income, with Social Security covering 20%; average annual real rate of return of 4%; and 4% initial withdrawal rate, adjusted for inflation. Sources: Morningstar, Northstar Investment Advisors

Read more: