The 5 Essential Retirement Moves to Make in Your 20s and 30s

At every stage of your journey to retirement, you need to know the essential money moves you should be making, the savings target you're aiming for, and the ideal mix for your investment portfolio. Those change as you move into your peak earning years and pre-retirement red zone. When you're starting out, use these checkpoints to set your course.

1. Saving: Collect your full 401(k) company match

Why it's key • If you start saving at age 35, you'll have to put away 16.6% of your income for 30 years to retire well at 65, according to research by Wade Pfau, professor of retirement income at the American College. Begin at 30, and your target drops to 12%. At 25, a steady 8.8% a year until 65 is enough—including the match.

How to do it • Typically you need to save 6% to earn the full 50¢-on-the-dollar match. Too much? Start at 3% and go up a point every year.

2. Work: Ask for $5,000 more in pay

Why it's key • What you earn in your first decade on the job has a lasting impact on your wealth. The typical worker's wages grow the most between ages 25 and 35, according to research by the Federal Reserve Bank of New York. A pay boost of $5,000 when you're 25 adds up to $634,000 more in lifetime earnings, a study by researchers at Temple and George Mason universities found.

How to do it • Whether you're fielding job offers or angling for a raise, negotiate. First, speak up. Only 37% of millennials have ever asked for a raise, reports salary site PayScale.com, but nearly half of those who did got the desired hike. Don't wait until review time. Put in your request right after you've pulled off a major project.

3. Investing: Be dogged about paying low fees

Keeping investing costs down is always smart. Locking in low fund expenses when you're young is especially rewarding over time. For example, if you invest $1,000 a month in a retirement account for 30 years, you'll end up with $761,000 assuming average mutual fund fees of 1.3% a year and 6% annual returns, according to Bankrate. With an index fund's average 0.5% expense ratio, you'd have $874,000. Better yet, pick an ultra-low-cost fund that charges just 0.2% a year, and you'll retire with $921,000.

4. Lifestyle: Balance saving and student loans

Why it's key • A third of millennials say that student-loan debt is delaying saving for retirement, a survey by the Investor Protection Institute found.

How to do it • To free up cash, switch to an income-based repayment plan (for federal loans only), which caps loan payments at 10% of income. Then contribute enough to get your 401(k) match, says Mark Kantrowitz, publisher of Edvisors, a college finance site. That's free money. When you start earning more, you can step up repayments to be debt-free faster. Learn more at StudentLoans.gov.

5. Mindset: Get to know the future you

Picturing your future self can put you in a savings mind-set. When Prudential Retirement installed a photo kiosk to let workers see what they might look like at 65, the number who enrolled in the retirement plan or hiked contributions rose 60% from a year earlier. Run your own aging experiment at faceretirement.merrilledge.com.

Once you've made these five moves, you're on your way. To see how you're doing, use these benchmarks to measure your progress:

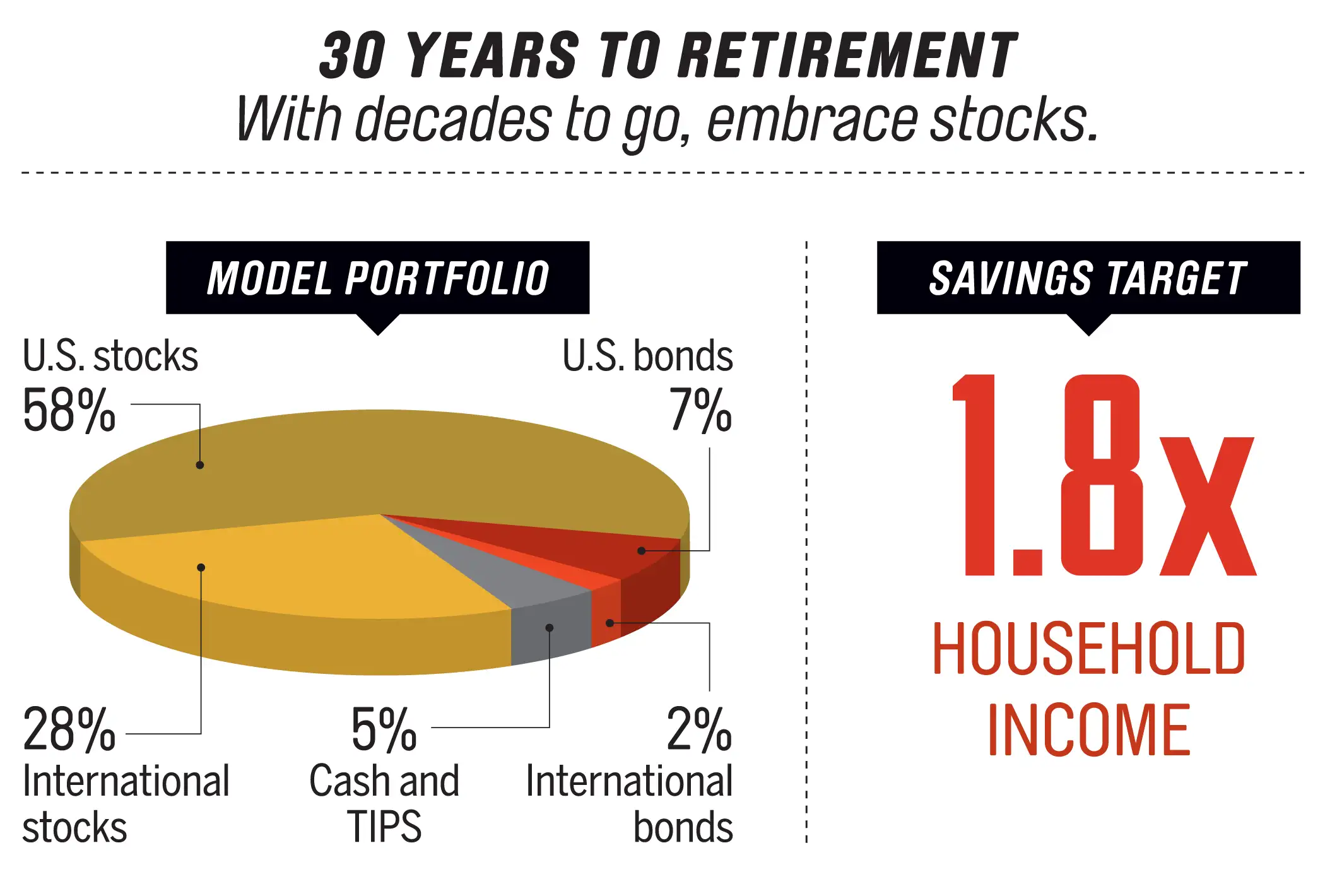

Notes: Savings rate assumes retiring at 66, replacing 75% of your pre-retirement income, with Social Security covering 20%; average annual real rate of return of 4%; and 4% initial withdrawal rate, adjusted for inflation. Sources: Morningstar, Northstar Investment Advisors

Read More:

- 5 Ways to Power Up Retirement Planning in Your 40s and 50s

- Do These 5 Things Now If You Want to Retire in 5 Years

- 5 Smart Things to Do the Minute You Retire