New Money Study: How the Pandemic Is Changing Americans' Credit Card Habits, From Spending to Paying Down Debt

Key Highlights:

- 70% of Americans said they have no plans to cancel or close an existing credit card as a result of the pandemic, and 38% of credit card users say it’s the only way they ever make a purchase right now.

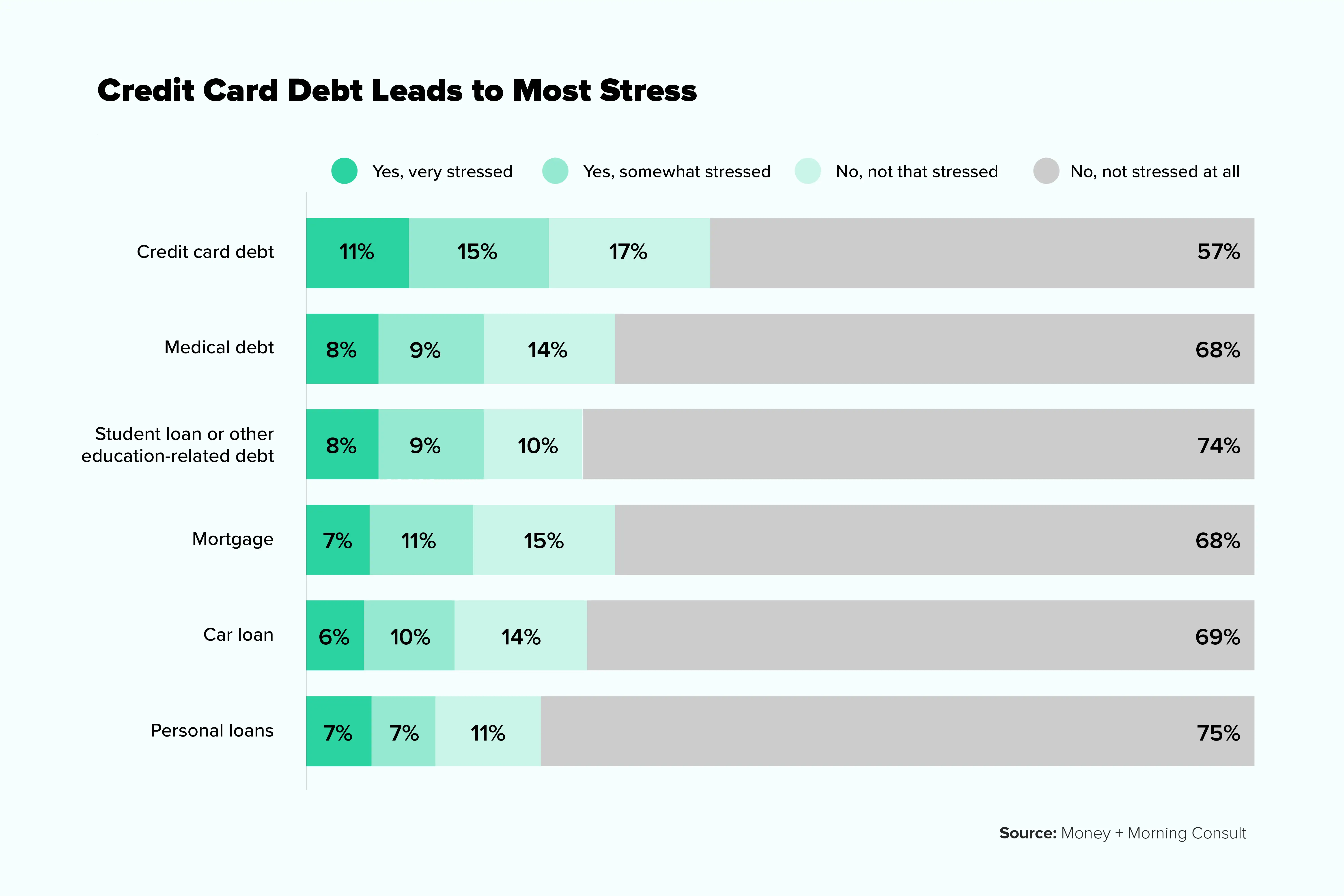

- Even with the total debt declining, 11% of Americans said they were “very stressed” about credit card debt as of September — more than any other type of debt, including mortgages, medical debts, or loans.

- 29% of credit card users said they’re using their credit cards more than they were pre-pandemic, particularly when it comes to food and self-care items (e.g. toothpaste).

- City dwellers were more likely to say they’re leaning on credit cards more now than they were pre-pandemic (39%), compared to suburban residents (25%) or rural residents (22%).

Americans are using their credit cards regularly despite the coronavirus pandemic that has engulfed the country this year, according to a recent survey by Money and Morning Consult. But they’re paying down debt and using their cards differently.

In March, when COVID-19 was declared a pandemic, American wallets took a hit. Uncertainty caused markets to plummet, entire industries came to a standstill, and within that first month more than 22 million Americans filed for unemployment for the first time. The consumer confidence index — a measure of consumer optimism, based on saving and spending patterns — hit a six-year low in April.

That figure is starting to regain its footing, with September numbers indicating that American consumers are more willing to spend now than any month since March. But they're not nearly at pre-pandemic levels just yet, as Americans continue to cope with job loss, pay cuts, and general economic uncertainty.

In order to understand how the pandemic has shaped our spending behaviors, Money and Morning Consult surveyed 2,200 U.S. adults from September 8-10, about their credit card usage and debt over the last six months, focusing on debt accumulation and psychological stress.

Nineteen percent of the respondents surveyed said they’ve been laid off or lost a job since February 15, 2020, and 33% said they have lost pay or income. At the time of the survey, 27% said they don’t own a credit card, with a little over half saying they own two or more. Half of those surveyed had a credit score of 660 or more.

Here’s how the pandemic has impacted America’s relationship with credit cards.

Top-line Results: Credit Card Debt During the Covid-19 Pandemic

A 70% majority of Americans surveyed said they have no plans to cancel or close an existing credit card as a result of the pandemic. Among Americans who said they own a credit card as of September, only 2% say they never use it, while 38% said it’s the only way they ever make a purchase.

This was more common for Americans with higher incomes or higher credit scores. And among the different types of credit card owners, ones receiving travel rewards were particularly likely to say they relied completely on credit cards for purchases.

Credit card debt, meanwhile, has been decreasing steadily since March.

In 2019, 45% of families in the U.S. had an outstanding balance on their credit card, according to the Federal Reserve's Survey of Consumer Finances. That made it the most widely held type of debt in the country, with the median family owing $2,700.

Going into 2020, Americans owed an all-time high of $1.09 trillion in credit card debt, according to the Federal Reserve. But by July, Americans had put a $99.5 billion dent in that balance, owing less than $1 trillion for the first time since September 2017.

Americans aren’t necessarily canceling their cards. But they are using this opportunity of reduced discretionary spending and lifelines provided by the CARES Act to chip away at their credit card balance. As part of the legislation, Americans received a round of stimulus checks valued at up to $1,200 per filer, and eligible unemployment recipients could collect an extra $600 per week through the end of July.

“Sometimes you need a crisis to wake you up to what you need to be doing, and I think a lot of people are experiencing that right now,” said Bradley Klontz, a Boulder, Co.-based CFP and financial psychologist.

Over half of those surveyed in September said that they’ve put money towards a debt as a direct result of the pandemic, or plan to in the future. That’s more than any other post-pandemic plan Money asked about, including meeting with a financial advisor, opening or cancelling a credit card, refinancing a loan or mortgage, applying for a loan, or making a large purchase like a house or a car.

Credit Card Debt and Pandemic Stress Levels

Even as Americans decrease their balances, however, there’s anxiety around it: 25% of Americans say credit card debt is a source of daily stress right now.

In normal times, this debt-related stress can be managed by chipping away at your balance or adjusting your spending habits, according to Shelle Santana, assistant professor of marketing at Bentley University. But during the pandemic, a lack of job security — highlighted by an 8.2% unemployment rate as of August — complicates things.

Paying off credit card debt is less likely to bring relief if you’re not sure whether you’ll have another paycheck to help pay the next bill. That stress is even more prevalent among Americans who already lost their job or are dealing with a pay cut, with 37% of these Americans saying they’re stressed about their credit card debt.

“This notion of being indebted is so aversive,” Santana said.

Experts like Klontz say that it's likely that the high interest rates credit cards carry is one of the root causes of the stress.

In Money's study, a majority of Americans say they’re paying interest on their credit cards regularly. Thirty-five percent said they spend up to $300 in interest in a typical year and 20% said they spend more than $300, with half of this second group citing interest at a thousand dollars or more.

People with a credit score between 620 and 659 were the most likely of any subgroup to be paying interest on their credit cards. They were also twice as likely to say they were “very stressed” about their credit card debt, indicating a correlation between interest paid and stress levels.

Interest, combined with ease of use and attainability, can make it easier to get in trouble with credit card debt than any other kind of debt, adding to the stress of simply owning a credit card. It can be particularly alarming for someone who got a new line of credit during a more financially secure time, and paid little attention to the interest rate or the terms and conditions around it.

“I do think that consumers are getting smarter about interest rates and [annual percentage rates],” said Santana. “What I’m concerned about is that we don’t pay close enough to these teaser rates and introductory rates.”

Ten percent of Americans said they weren’t sure if or how much they were paying in interest — a figure that stayed fairly constant across demographics and job status. Dr. Santana’s concern is that consumers often get lured in with a really low interest rate, only to find it increases later, or worse: The rate gets retroactively applied to previous years.

“That’s where people get into trouble a lot of times,” she said.

Pandemic Spending & Credit Card Behavior

Only a quarter of Americans said they’re spending more now than they were pre-pandemic. This was more common for people living in cities (34%) and less so for suburban residents (19%).

When it came to credit card usage, there was a similar trend: Urban residents were more likely to say they’re leaning on credit cards more now than they were pre-pandemic (39%), compared to suburban residents (25%) or rural residents (22%).

Overall, 29% of Americans said they were using their credit cards more now, particularly in two categories: food and self-care.

Thirty-two percent of Americans also said they’re swiping more at grocery stores and restaurants than they were before at-home-measures began. And nearly 20% said the same about toiletries like toothpaste and lotion.

And across all categories, Americans who lost a job or saw a decrease in pay since February were more likely to spend more on their credit cards. People of color were also more likely to spend on their credit cards, while at the same time more likely to be out of a job (and kept out of a job) than White Americans.

This spending behavior is in line with what happened in the last recession, when the unemployment rate reached 10% at its height and Americans started off by leaning heavily on credit. The difference between then and now is that they didn’t pay as much attention to debt, showing signs of lessons learned.

In the first five months of the last recession (December 2007 to May 2008), total credit card debt increased by $18 billion, compared to the $104 billion decrease in credit card debt in the same amount of time (February 2020 to July 2020). In 2007, the median family owed $3,700 compared to $2,700 in 2019, held by a similar percentage of families. And based on the averages, the maximum amount owed was also lower this time around.

These good practices are also reflected in our survey. People who started a new job as of February 15, 2020 were actually more likely to reduce their spending on discretionary items like electronics, recreational goods, furniture, or shoes, than they were to increase their spending on these things. And those who were laid off or lost a job were twice as likely as the average American to have cancelled or closed an existing credit card.

If faced with a large and unexpected expense right now, only 6% of Americans said they would open a new credit card to cover the expense, while 21% said they would pay for the expense with an existing credit card. Almost half said they would take money out of an existing emergency savings account.

The Top Features People Want in Credit Cards Right Now

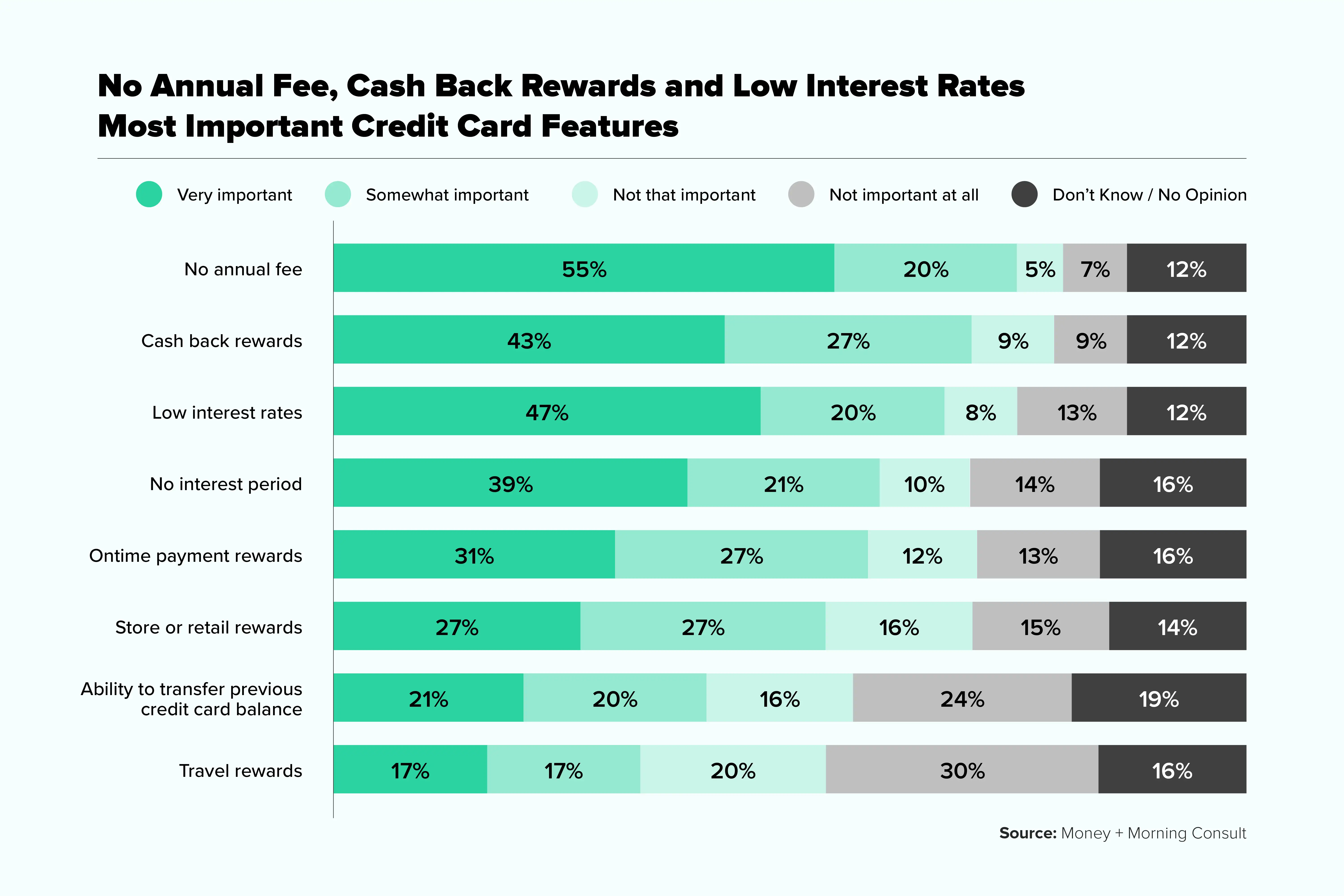

As of September 2020, Americans primarily owned credit cards with cash back rewards (41%), according to the survey. But many also lean towards ones with a general rewards program (27%) or ones from a store or retailer (26%).

Given the pandemic and the resulting economic downturn, a significant 75% of Americans felt that having no annual fee was a critical component for them personally. It was the only feature that a majority of Americans felt was “very” important in the current state of things. Other features that received high votes were low interest rates and cash back rewards.

Not surprisingly, travel rewards were the least favored feature, with half of Americans feeling it was unimportant and another 16% saying they don’t really have an opinion. Owners of this type of credit card were also the ones most likely to say they always used their credit card for purchases.

More From Money:

The Best Credit Card Deals of 2020

The Ultimate Guide to Ditching the City and Moving to the Suburbs