For a Huge Chunk of Millennials, Net Worth Has Tanked in the Last 3 Years

- Gen X Could Learn a Lot About Saving for Retirement From Millennials

- #MillennialRetirementPlans Is the Saddest, Truest Hashtag on the Internet Right Now

- Student Loan Changes 2026: New Repayment Options, Taxable Forgiveness and More on the Way

- New Study Finds You Need More Than Just Money to Save for College

- Survey Shows High Schoolers Vastly Underestimate Their Future Student Loan Needs

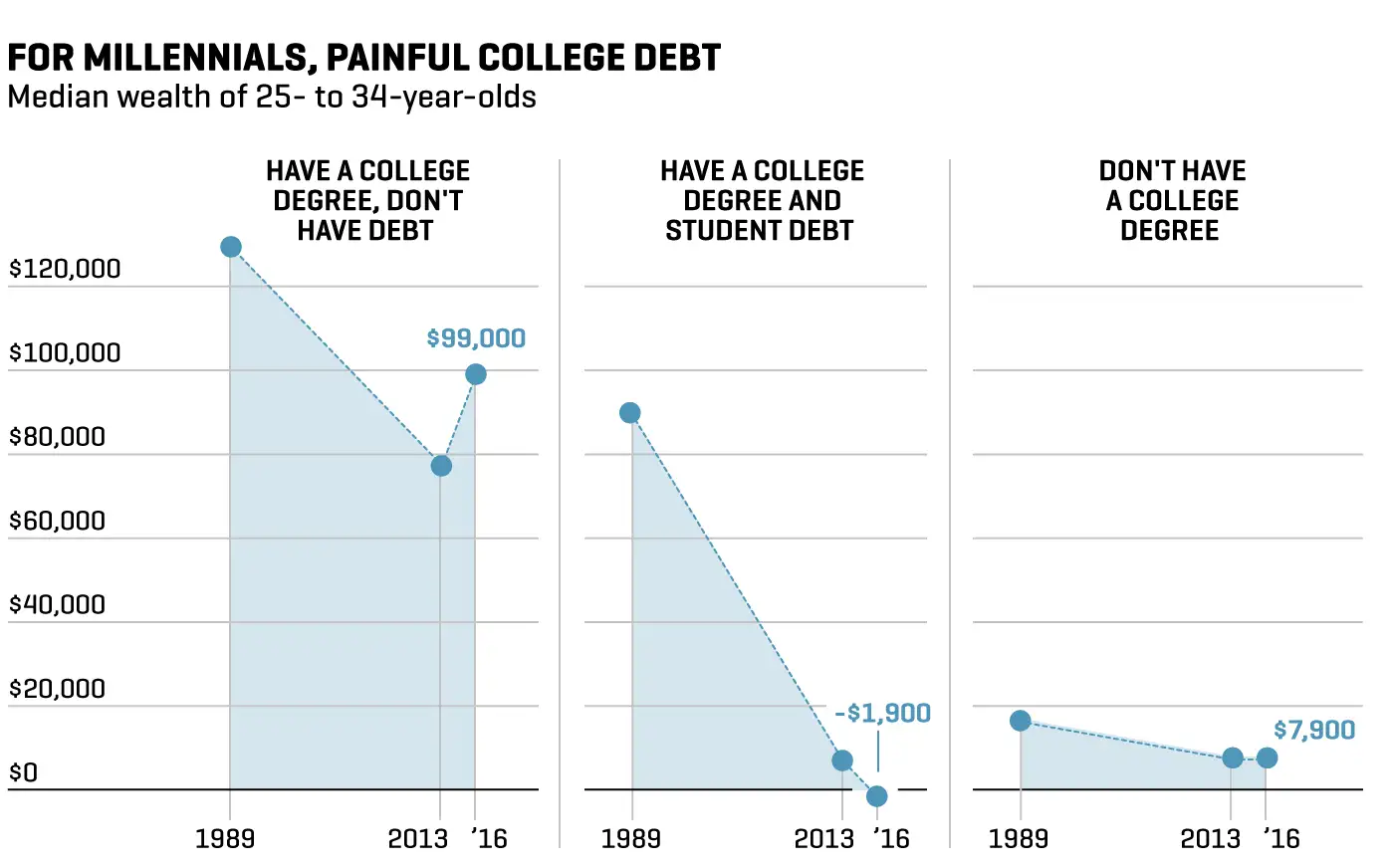

Young adults with student debt are falling even farther behind their parents' generation in financial well-being.

That's the takeaway of a report out today comparing the overall wealth of current 25- to 34-year-olds with the same age group in 2013 and 1989. Compared with three years prior, young adults in 2016 made small gains in median income, retirement savings, and assets. Yet across the board, those gains have barely put a dent in the larger gaps in earnings and wealth accumulation between young people today and 25 years ago.

The decline in net worth is particularly acute for young adults who have a college degree and debt. As you can see from the following chart, that group now has a median net worth of negative $1,900—down about $8,700 from three years ago and more than $90,000 from 1989, according to the report.

Despite low unemployment and seven consecutive years of growth in the stock market and gross domestic product, young people are still struggling financially, says Tom Allison, deputy policy and research director for advocacy group Young Invincibles and author of the report. Allison analyzed data from the Survey of Consumer Finances, a nationally representative survey conducted every three years, to look at financial assets and debts for young people over time.

Among young adults with debt, student loans made up 10% of their total amount owed back in 1989. By 2016, that had grown sevenfold, to 74%.

For young adults who don’t have college debt—either because they didn’t need to borrow, because they've already paid off their loans, or because they didn’t go to college—net wealth still plummeted between 1989 and 2013. But between 2013 and 2016, that decrease slowed, and even reversed direction for the group with a degree but no debt.

There are those who argue that the decline in net worth isn't necessarily a bad thing, if it's due to a long-term investment in education. After all, argues Matt Chingos—director of education policy at the Urban Institute and co-author of Game of Loans: the Rhetoric and Reality of Student Debt—when you buy a house, your net worth doesn't change much, at least at the beginning. You likely have mortgage debt, but you also have the value of that house, and those tend to balance each other out.

College, he says, is different.

"You're buying something, but its value isn't going to be on an asset sheet," Chingos says.

Homeownership also declined among young adults between 2013 and 2016, according to the Young Invincibles report. Allison attributes much of that decline to college graduates with student debt, because the homeownership rate among college graduates without debt and those who didn’t attend college remained steady between 2013 and 2016.

Yet other studies about the effect of student debt on major financial milestones, including home ownership, are less conclusive. That’s because there are a lot of demographic differences between individuals who can afford to attend college without borrowing and those who cannot.

A paper published last year in The Journal of Consumer Affairs, for example, found that, after controlling for those factors, young adults with student debt are just as likely to own a home as those without debt. Paying off student debt, though, is positively linked with a higher likelihood of owning a home.

All that research may feel far removed for a young adult dealing with day-to-day budgeting choices around debt and other major purchases.

Samantha Budzyn is about to face several of those decisions. The 24-year-old will graduate next month with a master’s degree in public health. She worked several jobs during undergrad and received enough financial aid to make it through a state university without taking out any loans. But she’s had to borrow about $60,000 for graduate school.

She’s worried her impending student loan payments will keep her from replacing an old, hand-me-down family car that frequently needs repairs.

“I want to have more stability in my life as a young professional,” she says. “And I think that means meeting my basic needs, which are housing and a car.”

Saving for retirement and buying a condo would be great, she says, but those are further down the list.

Growing up in rural Iowa, Budzyn saw her dad laid off from more than one factory job. She knows higher education has opened up opportunities for her that her parents, who didn’t attend college, never had. But it’s also hung a debt around her neck that her parents also never had.

A college degree, on average, still more than pays for itself. It's still the right path to go down, Allison says.

"But when you’ve got stratification between those that have to use student debt to finance that education and those that have other means of paying for it, you’re driving the wedge of inequality in our economy even wider."