How Social Security Works

In 1935, amid the Great Depression, President Franklin D. Roosevelt signed The Social Security Act, which established a national plan to provide economic security for the nation’s workers.

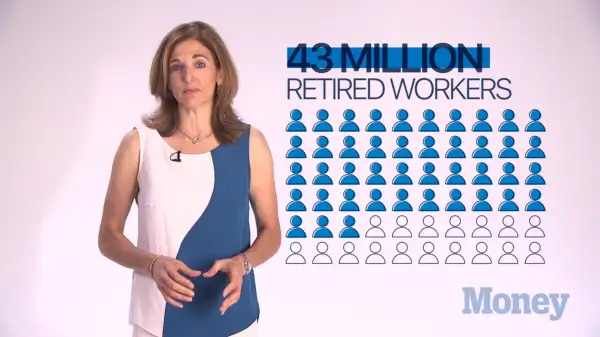

About 60 million people now receive Social Security benefits: 43 million retired workers and their family members, 6 million survivors of deceased workers, and 11 million disabled workers and their family members.

U.S. workers pay for Social Security through payroll taxes. The earnings of every employee in the Social Security system, up to a certain amount, are subject to a 6.2% tax. In 2016, that taxable amount is $118,500. So, as an employee, the maximum you’d pay into Social Security is around $7,350 -- while your employer has to pay another 6.2%.

If you’re self-employed, you have to pay as both the employer and the employee, for a total of 12.4% of your earnings, or a maximum of about $14,700.

Social Security is a pay-as-you-go system, meaning that money that workers put into the system today is intended to be paid right away to people who have qualified for benefits. When the government receives more money from taxes than is necessary to fund Social Security obligations, as it did in the 1990s, it creates a surplus -- one that exists to this day. But with baby boomers retiring in large numbers, the surpluses are on track to shrink and eventually disappear.