IRA Contribution Deadline: There's Still Time to Lower Your Taxable Income for 2021

- You'll Need Way More Money Than You Think for Health Care Costs in Retirement

- Counting on Working in Retirement to Boost Your Income? Here's Why That Strategy Can Backfire

- Can You Be 'Too Old' to Save for Retirement? Nearly Half of Americans Think So

- The Gender Wage Gap Can Add up to $1.6 Million in Lost Retirement Savings for Women

- Today's High Inflation Will Increase Retirement Health Care Costs...Forever

Taxpayers have a few more days to file their taxes this year, and that means you also have some extra time to contribute to your individual retirement account (IRA) for 2021.

The deadline to file your federal income tax return for 2021 is April 18, 2022. It's usually April 15, but this year that falls on Emancipation Day, a holiday recognized by the nation’s capital. So the tax filing deadline was pushed to the next business day. And since the tax deadline is also the last day you can make a contribution to your IRA for the prior year, that deadline is also April 18.

Here's what you need to know about IRA contributions for 2021.

For 2021 and 2022, the IRA contribution limit is $6,000 for those under 50 or $7,000 if you’re at least 50-years-old. You may be able to deduct the contributions you make to your traditional IRA from your income, which can ultimately lower your tax bill or boost your tax refund.

So how do you know if you can claim tax benefits based on your traditional IRA contributions? Here’s how it works.

If you aren't covered by a workplace retirement plan such as a 401(k) — and if you're married, your spouse isn't either — your deduction is allowed in full up to the contribution limit for the applicable tax year.

However, tax-deductible contributions may be limited depending on your income if you (or your spouse) have a workplace retirement plan such as a 401(k). In such a case, you may be able to take a partial deduction or none at all.

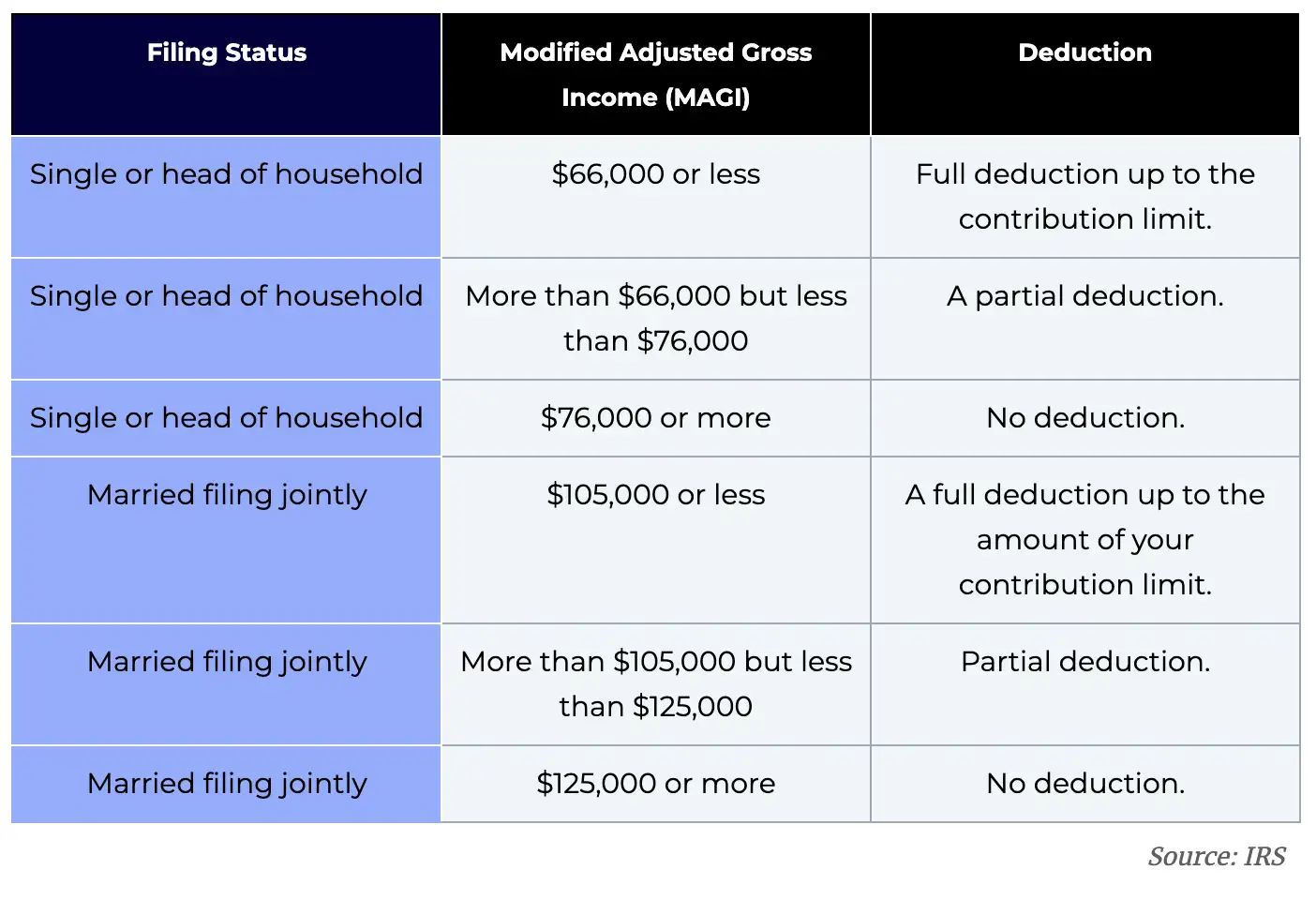

Here’s how it works if you alone are covered by a retirement plan at work and you want to make tax-deductible contributions for the 2021 tax year.

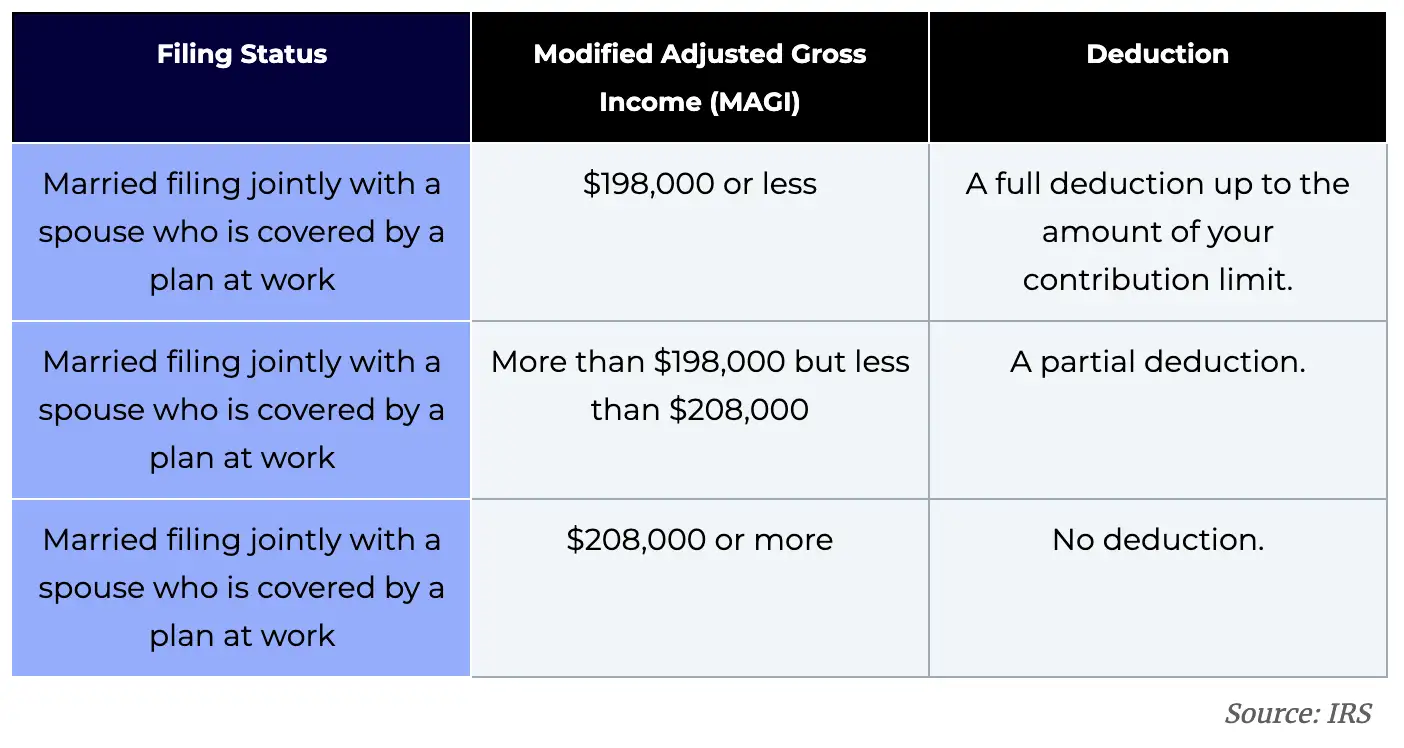

Here's how it works if you aren't covered by a retirement plan at work, but your spouse is. This also applies to contributions for the 2021 tax year.

If you believe you're eligible for a partial deduction, you can calculate it by using the worksheet on Page 17 of IRS Pub 590-A. Some tax software may calculate this for you too.

If you have a Roth IRA, you won’t be able to make tax-deductible contributions to your retirement account. Roth contributions are post-tax, and while you don't earn a tax-deduction in the contribution year, you can withdraw your contributions tax-free at any time (earnings may be subject to taxes and penalties under certain circumstances).

More from Money:

7 Big Tax Changes That Could Affect Your Return — and the Size of Your Refund