Why Low Job and Wage Growth is Worse Than Rising Inflation

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

As the economy added another 248,000 jobs in September, pushing the unemployment rate to a post-recession low of 5.9%, investors are feeling more confident.

In fact, investors are more optimistic than they’ve been since the recession, per a recent Wells Fargo/Gallup survey which measured the mood of those with more than $10,000 in investable assets. Of course the so-called Investor and Retirement Optimism Index is still only at around half the levels of the 12-year average before the 2008 recession. Investors may be more sanguine than three months ago, but that doesn’t mean they think the economy is going gangbusters.

Nevertheless, there was one particularly interesting data point in the survey: “Half of investors (51%) think the pressure on American families’ ability to save is due to rising prices caused by inflation.” Meanwhile only 37% said the pressure was inflicted by stagnant wage growth.

Which is strange.

What inflation?

If you look at the Federal Reserve’s preferred measure of core inflation (which strips out volatile energy and food prices), prices have risen around or below the Fed's stated 2%-target since the recession.

The Consumer Price Index, a gauge of inflation released by the Labor Department, actually fell on a monthly basis in August for the first time in more than a year, and only grew at an annual rate of 1.7% since this time last year.

Proclamations of rising inflation ever since the Federal Reserve started buying bonds and lowering interest rates in response to the recession have yet to materialize. And those advanced economies that did raise interest rates a few years ago (like Sweden), have come close to deflation.

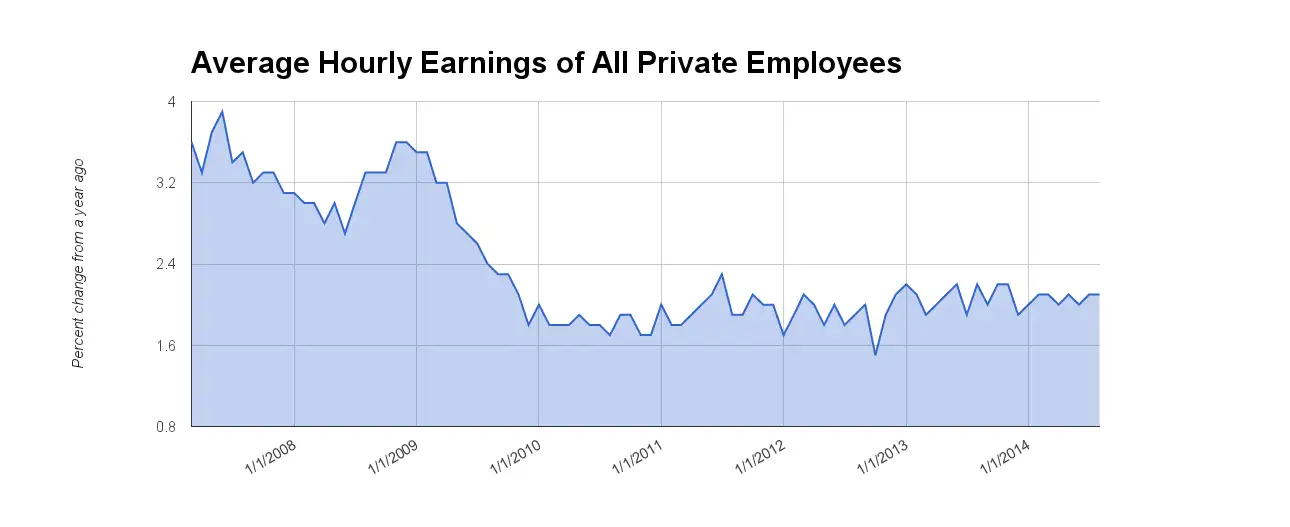

Meanwhile wages aren’t growing at all. Average hourly earnings in August rose 2.1% versus the same period last year, and the growth rate has been stuck at around 2% since the recovery. The same is true for the employment cost index, which measures fringe benefits in addition to salaries. Ten years ago the index increased by 3.8%.

While the unemployment rate has fallen considerably this year, other gauges of jobs are still troubling. Long-term unemployment has tumbled since its post-recession peak in 2010, but there are still almost 3 million people who’ve been unemployed for 27 weeks or longer. If you include workers who’ve recently stopped looking for a job and those working part-time when they’d rather be full time, the unemployment rate is 12%, more than four percentage points above the pre-recession level.

The Fed has implemented an easy monetary policy in order to attack this problem. "The Fed is keeping interest rates low as long as they can and maintaining very loose policy in support of jobs," says USAA Investments's chief investment officer Bernie Williams. "They will only tighten up with great reluctance."

Pick your poison: stronger wages or rising inflation?

In a battle between pushing wages higher and the risk of inflation, the Fed is willing to err on the side of rising wages, says Williams.

BMO senior investment strategist Brent Schutte agrees. "As a society, you decide what is good. Economics is a choice between two things. We’ve clearly decided that higher inflation and rising wages is a good thing."

Despite years of effort, though, the Fed hasn't been able to bring back rising wages.

If you're still unconvinced that a lack of salary increase and slack in the labor market should be more of a concern to your finances than the threat of inflation, check out new research by former Bank of England member David Blanchflower.

Along with three other co-writers, Blanchflower recently published a study titled, "The Happiness Trade-Off between Unemployment and Inflation."

The researchers found that unemployment actually has a more pernicious effect on happiness than inflation. "Our estimates with European data imply that a 1 percentage point increase in the unemployment rate lowers well-being by more than five times as much as a 1 percentage point increase in the inflation rate."

In an interview with the Wall Street Journal, Blanchflower said, "Unemployment hurts more than inflation does.”

As the economy gently improves, and people start going back to work, the hope is that wages will start to rise. Inflation might then rise above the Fed's 2% target, and Yellen and Co. may raise rates in effort to cool off the economy. But we're not there yet. And investors, for the sake of their wallets and psychology, would do well to remember that.