Make Your Kid an Investing Genius

A woman once told me she had come up with a great idea to educate her 14-year-old son about investing: She gave him $500, opened a brokerage account in his name, and told him to buy some stocks.

Smart? Errrrr, not so much.

If the stocks went down, her kid would be likely to conclude that investing is a sucker's game and avoid the market altogether. That's a problem. If the stocks went up, he'd think he was a genius and start placing bigger, bolder bets. Which could be an even worse problem.

Now, I do think kids should learn about investing. They just need to be taught what really matters, and they need to be taught in ways that correspond to their age and their interests.

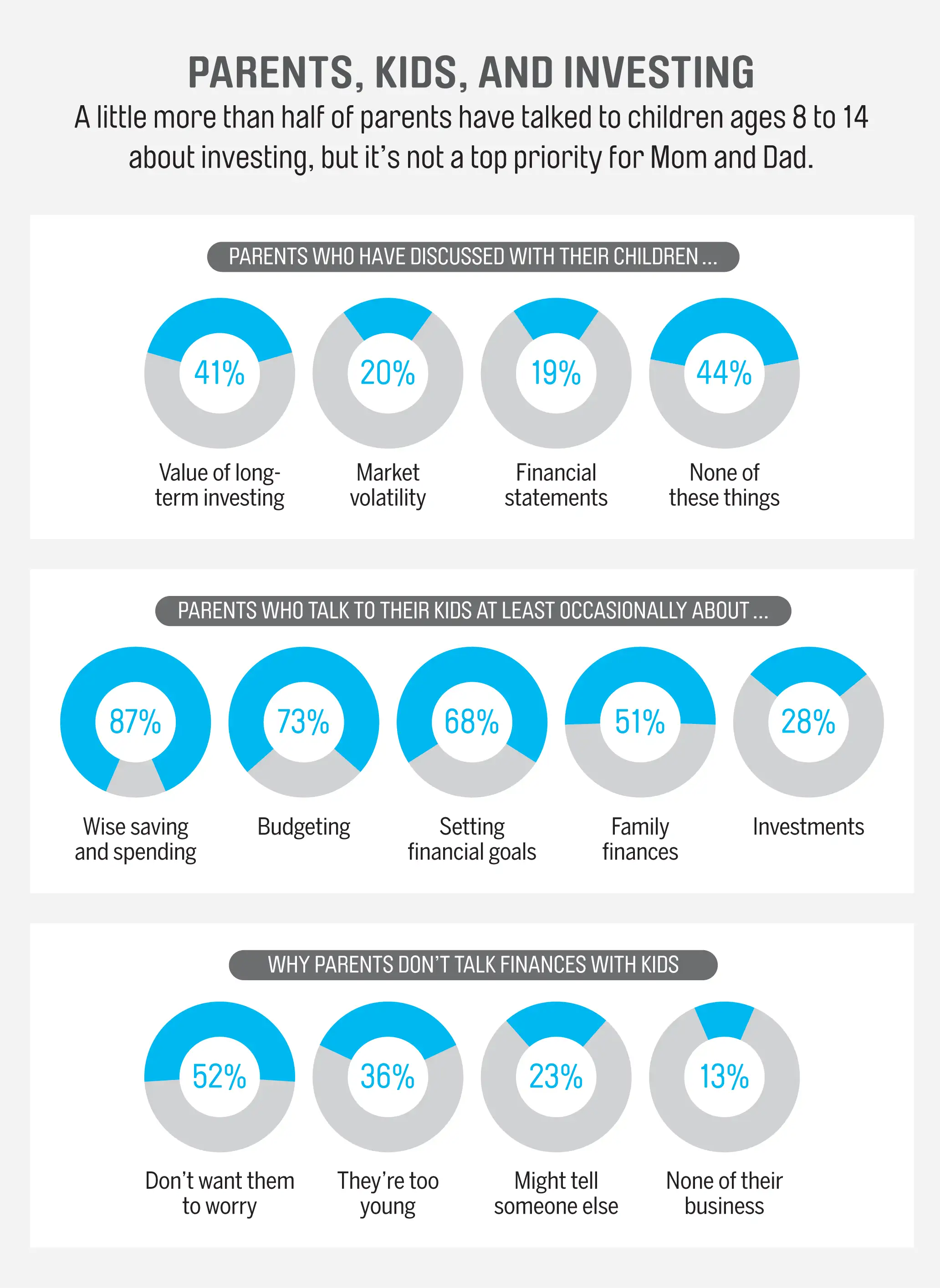

You might be tempted to put off investing discussions until your kid is grown up and has money to invest. But don't. Making sure that your child learns the fundamentals early will be a valuable gift. Even if your kid is flat broke, getting comfortable with the market will help him when he does have money.

So get started now, with these easy, age-appropriate lessons.

In Preschool: Plant the Seeds of Knowledge

You can't teach price/earnings ratios to a toddler. But with some other concepts, she can start making important connections between current efforts and subsequent results.

An investment is something that pays off in the future. Get a copy of The Little Red Hen and read it to your child. The gist of this old fable: The hen invested the time and effort to turn wheat into bread—sowing the grain, harvesting it, and making the dough. The lazy animals who were her friends blew her off and didn't help until it came time to eat. But that Little Red Hen was no pushover. She refused to share her bread with the slackers, and everyone learned a lesson.

The Little Red Hen was thinking long-term and reaped the rewards of her investment of time and hard work. Introduce the concept of being an "investor" when your kid completes a puzzle or an art project: "Wow, you really invested time and effort—and look at what you've done!"

Investments take many forms. Because young kids have a hard time understanding the concept of the future, wrapping their little minds around investing can be tough. So relate it to something tangible. Help your child plant a garden or put some seeds in a flowerpot. Talk about the time the plant needs to grow and the water you need to "invest" in it so that you get the payoff of a beautiful sunflower or a ripe tomato at the end.

In Elementary School: Play the Lottery (Really!)

Kids this age are able to absorb more than you might think about simple investing concepts—and are more interested than you'd guess.

A stock is a small piece of a company that you can own. The next time you watch a Disney movie or sip a Coke with your kid, you can use the occasion to teach him about stocks. Start by saying that a lot of the stuff he likes is made by companies. The Coca-Cola Co., for example, makes that drink he loves (but may not be allowed to have very often). It needs money to make that Coke, and to get that money, many companies sell what is called stock. When people buy stock in a company, they own a little piece of it.

Don't put all your eggs in one basket. Tell your kid to imagine opening a restaurant that sells only hamburgers. (That shouldn't be hard.) As long as people really like hamburgers, she'll make lots of money. But what if people hear that some cows got sick, and those people decide that burgers aren't safe to eat anymore? Or what if they want French fries, too, and start going to a restaurant that sells more than just hamburgers? That hamburger-only restaurant could go out of business.

This illustrates the crucial investment concept of diversification. When you buy the stock of a single company—say, Krispy Kreme—you're making a big bet on that one company and the future popularity of doughnuts. If, however, you own stock from many different companies, you're reducing the risk that you'll lose all your money. That's because if some companies' stocks do poorly, some other companies' stocks might do well.

The lottery is not an investment. Ask many kids how to make a lot of money fast, and they'll answer, "The lottery." If your kid has lottery fever, let him learn the hard way. Buy some lottery tickets for him the next time there's a big jackpot. When your kid doesn't win (and he won't), explain that the chance of winning a lottery jackpot can be less than one in 250 million. That's so small, it's a waste of money to play at all.

In Middle School: Teach the Power of Stocks

Making money is a subject that captures middle schoolers' attention. So show them how their own money can do it for them.

Compound returns can make you rich. When you invest, you can earn returns on the initial money you put in, known as the principal. That's great. But what's really great: If reinvested, your returns can earn returns too—what are known as compound returns. That keeps happening over time, and the longer your money compounds, the faster it grows.

Use the compound interest calculator on Investor.gov as a demo: Let's suppose your child sets aside $7.50 a month starting at age 10, earning an average of 7% a year. By the time she's 65, she would have $51,800. If she didn't begin until age 35, she would have only $8,250. The moral: Starting early pays off.

Doubling your money is a realistic goal—over time. Show your kid the "rule of 72," which is a neat trick for figuring out how many years it will take to double her money if it's earning interest or is invested in the stock market. Divide 72 by the rate your money is earning. The result is the number of years it will take to double your principal. So, for instance, if your investments earn an average of 7% a year, you'll double your money in a little more than 10 years (72 divided by 7 is 10.3). There's a mathematical explanation for this (and if you really love math, do an online search for "rule of 72" and knock yourself out explaining it to your child). But all your kid needs to know now is that the rule works.

Inflation can smother your buying power. This concept can be a yawner, but you can explain it this way: Over time the price of all the stuff we buy tends to increase. For example, today a Hershey bar might cost $1, but in 1970 that same bar might have cost 10¢. So $1 buys you much less today (one chocolate bar) than it did back then (10 bars).

How can your kid protect his money from losing value? By putting it where it will grow at least 3% a year—roughly the average rate of inflation over the past three decades. Since savings accounts pay much less today, that's why investing in stocks is so important.

Stock picking is a losing game. Stock market contests are all the rage: Kids create an imaginary portfolio that tracks real stocks. The idea is that with some research you can pick stock winners. But there's one big problem: Thousands of analysts follow a company's stock trying to predict whether it will rise or fall—and they often get it wrong. In order for your kid to pick winners consistently, she'd need to know more than all these analysts combined. And that just isn't possible, even if your kid's favorite channel is CNBC.

As mentioned earlier, diversifying—or investing in lots of stocks rather than just one—is a better approach. The simplest way to do that is to invest in a so-called index, which is simply a grouping of stocks, like the Standard & Poor's 500. And the easiest way to invest in an index is to buy what's called a stock index mutual fund, which holds the stocks that make up a particular index.

Girls are investors too. No matter how progressive a parent you are, make sure you aren't subconsciously skipping the investment talk with your daughter. A study out of North Carolina State University and the University of Texas found that parents are much more likely to talk to boys about investing than to girls. And that may have consequences: In a poll of adults ages 22 to 35, just 56% of women had begun saving for retirement, vs. 61% of men.

In High School: Get Real About Investing

Many teens have some money from part-time jobs or other sources. You can help your child turn his cash into some practical lessons.

Taxes and matches are your friends. If your high schooler has a job, have him open a Roth IRA. The money in a Roth grows tax-free, which will make it multiply like crazy, especially if your kid starts early. And a Roth is particularly helpful for someone who will be in a higher tax bracket at retirement age (a safe bet for most teenagers). If your high schooler opens up a Roth, he can withdraw the money that he has put in at any time—without paying any taxes or penalties. (He'll have to pay taxes and penalties, in most cases, on earnings he withdraws before turning 59½; after that, withdrawals are tax-free.)

If you can afford it, match your kid's IRA contributions. Say he makes $3,000 over the summer as a lifeguard and puts $500 of that in a Roth. With a $500 match from you he can deposit a total of $1,000. This will not only double his principal, but also prime your kid for the day he gets offered an employer's 401(k) match. The most your kid can deposit, however—his money plus anything you contribute—is what he earned during the year, up to an annual limit (currently $5,500).

Indexing is the best strategy. Okay, so now you know that your kid should put part of his paycheck into a Roth IRA. Then what? He'll need to pick investments that will allow it to grow. Here are two good choices:

Option A is an index mutual fund. As you can explain to your kid, not only do such funds give you diversification, but they also tend to cost less than actively managed funds. And, on average, they do better than funds in which an expert picks the stocks. One inexpensive choice is Schwab Total Stock Market Index (SWTSX), which has a 0.09% expense ratio and requires a $1,000 initial investment (unless you set up automatic monthly contributions).

Your kid doesn't have $1,000 to invest? Option B is an index exchange-traded fund, which can have a much smaller initial buy-in than a mutual fund requires. For about $100, he can invest in an ETF like the Vanguard Total Stock Market (VTI). Some companies, including Schwab, E*Trade, and Fidelity, offer commission-free ETFs.

You can invest for good. Recent studies have found that young people really want to buy from companies supporting causes they think are worthy. So your kid also might want to sink her money into what are called socially responsible funds. Some don't invest in certain industries, such as tobacco or firearms, while others seek out corporations that treat employees well. Still others focus on companies involved in energy conservation or environmentalism. At SocialFunds.com, find lower-cost funds such as Vanguard FTSE Social Index (VFTSX) and iShares MSCI KLD 400 Social ETF (DSI). Then your child can feel even better about making money in the market.

Excerpted from Make Your Kid a Money Genius (Even if You're Not): A Parents' Guide for Kids 3 to 23, by Beth Kobliner. Published by arrangement with Simon & Schuster Inc. Copyright © 2017 by Beth Kobliner.