Top Stock Picks From 4 Professional Investors Who Keep Beating the Market

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Consistency is the rarest of qualities in the mutual fund world. Managers come and go. So, too, does market-beating performance.

But the four stock funds featured below are among the rare exceptions. In each case, the managers have been in place for a decade or more and have stuck with their investment strategy during that period. What's more, that consistency has paid off throughout the market's ups and downs: Each of the funds has beaten the majority of its peers over the past one-, five-, and 10-year periods.

So we decided to ask these extraordinary managers to do what they do best: think about the long term, and share with us the three stocks they feel most confident will outperform for at least the next few years. Follow their lead, and you may come out ahead too.

The Pros: Charles Pohl and team, managing since 1992

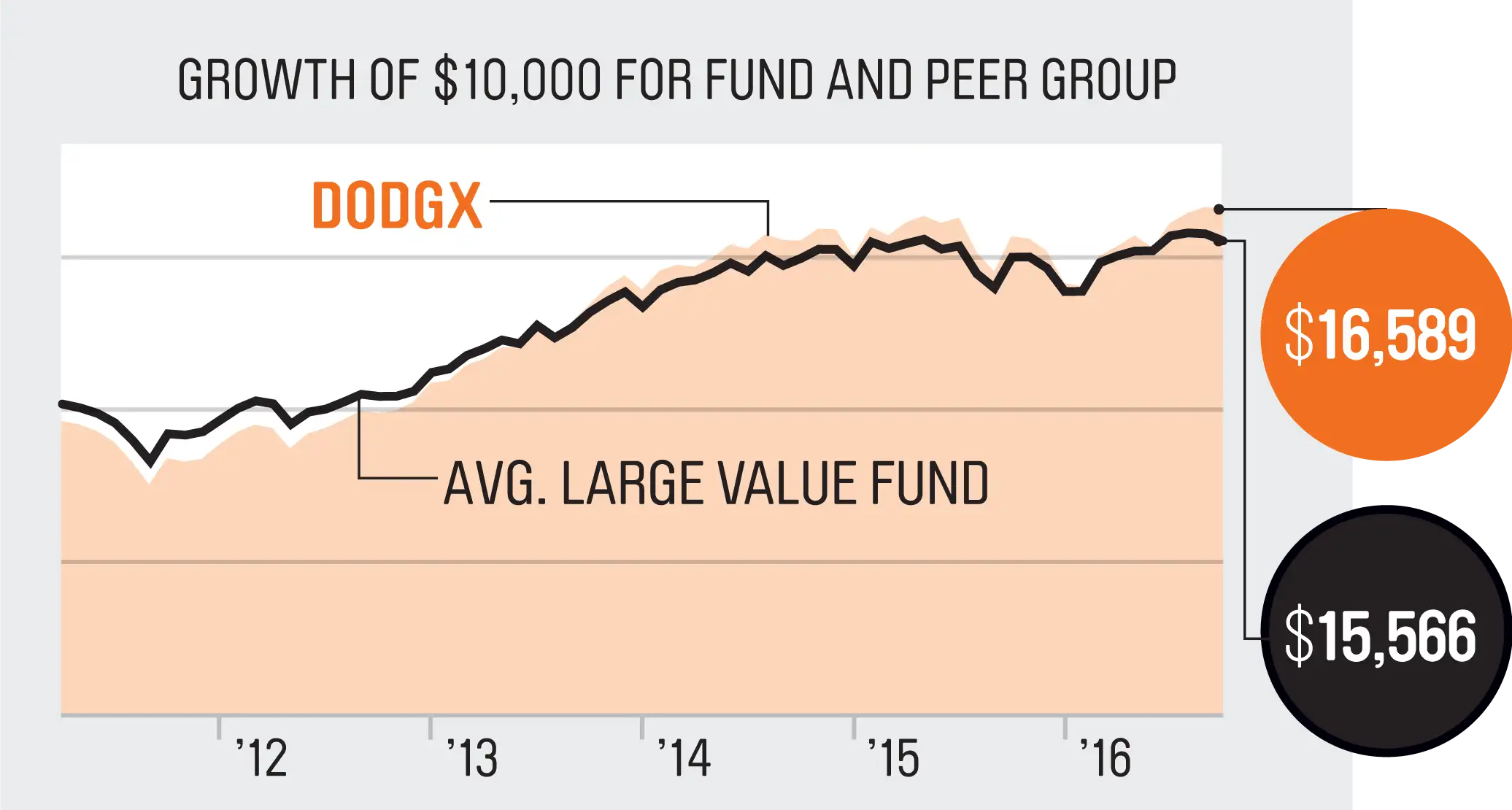

DODGE & COX STOCK (DODGX)

Expenses: 0.52% | Minimum: $2,500 | 5-year annualized return: 17.1% | 10-year: 6.1%

Launched in 1965, Dodge & Cox Stock has a long tradition of buy-and-hold investing. A team of eight managers—some of whom have been with the fund for more than 20 years—looks for shares of large businesses under a temporary "cloud," dampening their prospects, such as low oil prices or near-zero interest rates. The stocks are bought at depressed prices and typically held for six or seven years, allowing time for the air to clear. "You don't know exactly when things will turn around, so you have to have staying power," says chief investment officer Charles Pohl, one of the fund's managers.

To improve the odds of finding success stories, Pohl and his colleagues favor companies that dominate their industries, and that have strong management teams and in-demand products and services. "That helps us get confident about the stock," he says.

THE PICKS

Charles Schwab (SCHW)

The discount brokerage is attracting new investments, thanks to low-cost offerings such as ETFs. In fact, Schwab's fees are lower than other full-service brokers', so the company continues to take market share, Pohl says. Case in point: Schwab now has more than 10 million brokerage accounts, up 4% from a year ago. Meanwhile, more than 40% of its revenues come from reinvesting its $186 billion in bank deposits and other cashlike accounts into short-term investments. That return now averages 1.73%—roughly half what it did before the financial crisis. Pohl says that once low rates start to rise, Schwab's profits will jump meaningfully.

National Oilwell Varco (NOV)

The stock of this oil-drilling equipment maker has plummeted—along with energy prices and profits—falling 57% since 2014. But Pohl and his team note that global oil supplies are expected to fall short of demand as early as 2018. "At some point supply will have to catch up," Pohl says.

When that happens, National Oilwell Varco should benefit. The firm is the leading supplier of rig equipment used for both offshore and onshore drilling. In recent years, two-thirds of new oil exploration has been done offshore, putting the company in an enviable position for when oil prices recover, Pohl says. Meanwhile, the stock is priced at only 96% of book value (the company's assets minus liabilities), when normally it trades at a premium. "The company is quite cheap relative to its long-term strategic position," he says.

Union Pacific (UNP)

Low prices for natural gas, coal, and other commodities have weighed on Union Pacific, whose trains transport goods across 32,000 miles of tracks in the Western U.S. Since early 2015, the stock has declined 16%. But Pohl & Co. point out that commodity prices will eventually bounce back. Until then, Union Pacific is taking steps to become more efficient, such as improving scheduling to reduce train bottlenecks. Union Pacific enjoys a profit margin of 21%. But Pohl notes that margins for Canadian railroads, the gold standard for profitability, are as high as 30%. "There's room for improvement, and management's efforts are being masked by a difficult commodities market," he says.

The Pro: Todd Ahlsten, managing since 2001

Parnassus Core Equity (PRBLX)

Expenses: 0.87% | Minimum: $2,000 | 5-year annualized return: 14.0% | 10-year: 9.2%

It's hard to put Parnassus Core Equity into a box. The fund invests in stocks of large companies, and manager Todd Ahlsten, at the helm for more than 15 years, looks for firms in expanding industries with strong management teams and a competitive advantage. But the stocks must also be priced well relative to their underlying value.

"We look at a range of outcomes for a stock, and we make sure there's more upside than downside before buying," Ahlsten says.

In addition, each company must meet certain environmental, social, and corporate governance principles—a mandate for all funds that are run by Parnassus. What's more, three-quarters of Core Equity's stocks have to pay dividends.

The result is a portfolio of around 40 holdings that, Ahlsten says, targets high-quality companies and serves investors well over the long run.

THE PICKS

CVS Health (CVS)

CVS is one of the leading retail pharmacies in the U.S., commanding nearly a quarter of the market. And sales at existing stores continue to climb, rising 3.4% in the most recent quarter compared with the year before. The stock has fallen 32% since 2015, however—largely, says Ahlsten, because CVS's pharmacy benefit management business (which negotiates prices for prescription drug plans) has lost customers to competitors. But he's optimistic long term, noting that customer retention was still 96% at the end of the most recent quarter. He also expects that CVS will partner with other PBMs, offsetting recent losses. Wall Street analysts agree, estimating profits will climb an average of 10.9% annually for the next five years vs. 8.2% for other consumer staples stocks.

Gilead Sciences (GILD)

Gilead Sciences is a biotech company best known for its groundbreaking hepatitis C treatments. But competing therapies have pressured sales, and the stock is off 39% since 2015.

Ahlsten still sees opportunity. Some 31,000 new cases of hep C are diagnosed in the U.S. each year, and roughly half of the 3.5 million Americans infected are unaware they have the virus, creating a "long runway" of demand.

In addition, Gilead makes leading therapies for HIV/AIDS, and the launch of three popular new drugs boosted sales in this category by 21% in the latest quarter, to $3.5 billion, vs. the year before. That, says Ahlsten, helps Gilead generate plenty of cash for research and acquisitions. The stock also yields a healthy 2.5% and trades at about half the industry's average price/earnings ratio of 12.2.

Intel (INTC)

PC sales are declining in the mobile era, but Intel isn't slowing down. The chipmaker is focusing on new markets like data centers, cloud computing, and the Internet of things, the catchall term for everyday objects that connect to the web. "The Internet uses a tremendous amount of data, so energy-efficient chips are critical," Ahlsten says. "Intel is one of the few companies with the manufacturing capability to build them."

With a P/E that's 20% lower than its peers', the stock is cheap. Still, investors earn a hefty 3% yield, and sales tied to the Internet of things jumped 19% in the last quarter vs. a year ago. Ahlsten says Intel's profits could rise an average of 10% a year for the next decade.

The Pro: Sudhir Nanda, managing since 2006

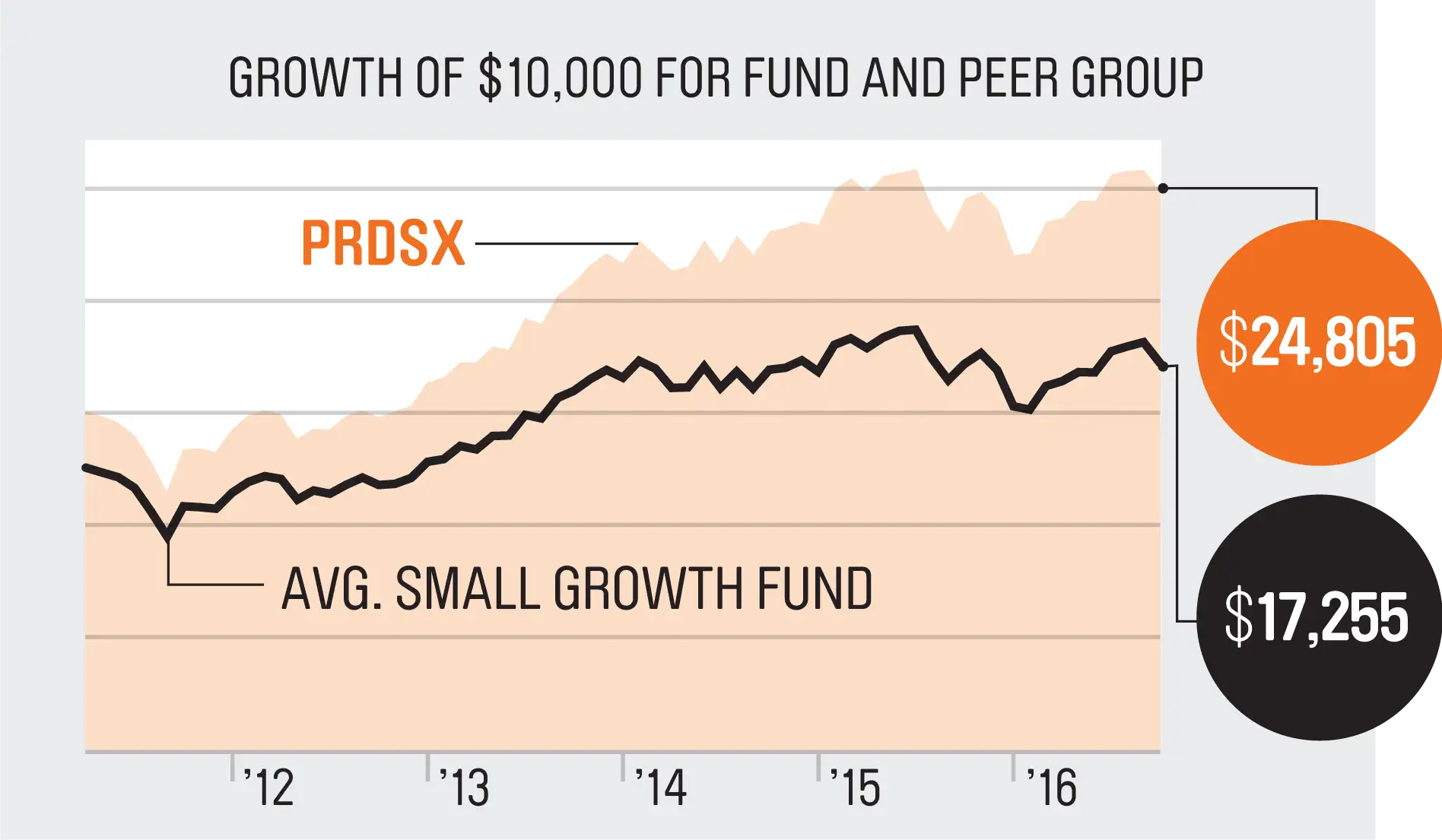

T. Rowe Price QM U.S. Small-Cap Growth Equity (PRDSX)

Expenses: 0.82% | Minimum: $2,500 | 5-year annualized return: 14.6% | 10-year: 10.0%

Stocks of small growth companies are susceptible to both big highs and big lows. To minimize the impact of those swings on his portfolio, Sudhir Nanda—who has run QM U.S. Small-Cap Growth Equity for the past decade—uses quantitative screens to zero in on quality businesses that outperform over time.

Starting with about 1,200 stocks, he ranks companies by their price relative to free cash flow, the money left over after covering obligations. "You can't manipulate cash flows as much as earnings, so it's a better measure of quality," Nanda says. He also looks for firms with a stable return on equity, as well as a record of smart acquisitions, share buybacks, and dividends. Of the stocks that pass this screen, Nanda and his team use independent research to actively pare the list further, ending up with about 300 holdings.

This approach also minimizes risk, which is one reason the fund has been added to the Money 50, our recommended list of funds.

THE PICKS

Service Corporation International (SCI)

Service Corporation International is the largest provider of funeral services in North America, with more than 2,000 cemeteries and funeral homes. But the company still controls just 16% of the market. "Buying some of the mom-and-pop operators could be a source of growth" as they achieve scale and expand their geographic footprint, Nanda says. Meanwhile, an aging population is driving higher revenues. From 2012 through 2015, so-called pre-need sales (where people pay for their own burial services during their lives) climbed an average of 10.5% annually. Service Corp. was also able to raise the average price of those contracts. In the past quarter alone, that helped boost revenue by $1.9 million. That trend is likely to continue, Nanda says, resulting in more contracts and higher prices per contract.

Over the past decade, the stock has beaten the return on the S&P 500 by nearly five percentage points a year.

The Toro Co. (TTC)

Turf equipment maker Toro is broadening, well, its turf. Last year, Toro announced it would buy a German competitor, helping Toro offer service to more sports facilities and agricultural areas. In 2014 it expanded into snow and ice removal with the purchase of BOSS, a maker of snowplows. The acquisitions have helped diversify the business and boosted profits: For the first nine months of 2016, earnings climbed 13% to $201 million. Even though Toro has gained 38.9% over the past 12 months, Nanda believes there's still room for the stock to run. Analysts project that profits will rise an average of 19.5% annually for the next five years. "That's a very healthy rate in a slow-growing economy," Nanda says.

Vail Resorts (MTN)

Vail Resorts is the largest ski operator in North America and still growing. In 2016 the company—which runs resorts including Vail and Breckenridge in Colorado, and Park City Mountain Resort in Utah—bought Whistler Blackcomb, Canada's preeminent ski destination. The acquisition is likely to increase visits from both skiers and other vacationers: Whistler is spending $345 million on facilities to attract visitors in any weather conditions, including an indoor sports complex. Not surprisingly, analysts expect profits to be robust, rising an average of 24% annually for the next five years.

Vail, in turn, is rewarding investors. Since initiating a dividend in 2011, the firm has lifted its quarterly payout from 15¢ per share to 81¢. Nanda expects Vail will keep raising that and buying back shares. "Management is making all the right moves," he says.

The Pros: William Browne, Thomas Shrager, John Spears, Robert Wyckoff, and team, managing since 1993

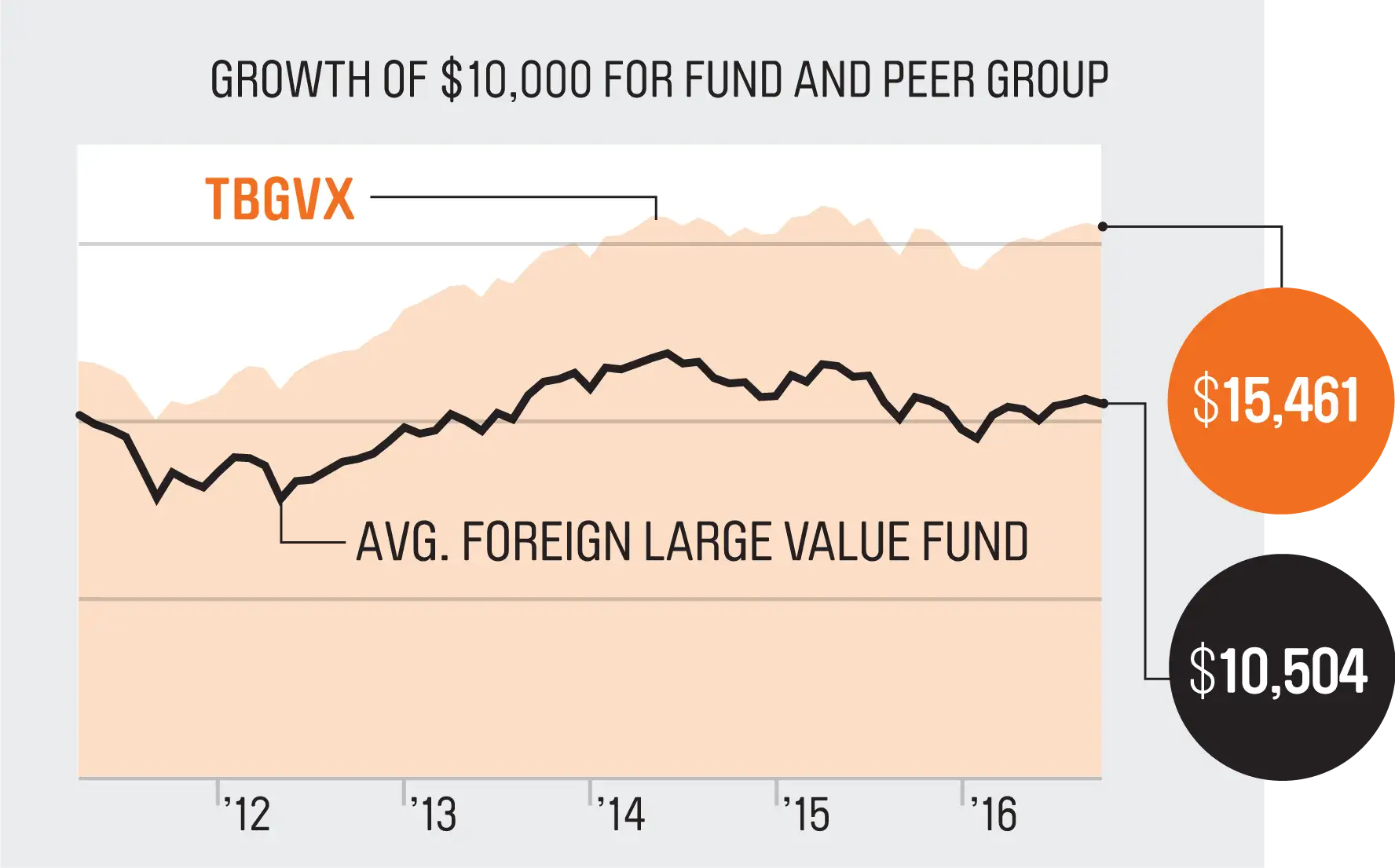

Tweedy, Browne Global Value (TBGVX)

Expenses: 1.32% | Minimum: $2,500 | 5-year annualized return: 8.0% | 10-year: 4.2%

The seven managers of this foreign stock fund are champions of value investing. They scour the globe for discounts, often favoring stocks trading below a company's tangible book value (its assets minus its liabilities and nontangible assets). To give themselves plenty of options, the managers will invest in firms large or small without regard to borders; that means U.S. companies are fair game too.

As such, they sometimes wade into stocks that have been beaten up because an event or market scare caused investors to overlook a company's true worth. "In many instances, we feel like the odd man out," says William Browne, who, along with three of the other managers, has been leading the fund since its launch in 1993.

The strategy has worked. Since inception, the fund's average annual return has trounced the MSCI EAFE index of foreign developed stocks, by 3.7 percentage points (adjusted for currency swings)—and with significantly less volatility.

THE PICKS

AGCO (AGCO)

Although this agricultural equipment maker is based in the U.S., roughly three-quarters of its sales are generated overseas. In recent years, low crop prices have limited demand for AGCO's products, which include tractors and combines. The stock is down 12% since 2013.

Tweedy, Browne's managers say AGCO's diversified lineup will help it get through the slump. For example, AGCO sells equipment to pig and poultry farmers—and with consumers in emerging markets eating more meat, sales are rising. While it's unclear exactly when demand for farm equipment will hit bottom, anticipation of that is likely to drive the stock higher in the near term. For AGCO, which commands 45% of Brazil's tractor market and 30% of Europe's, a rebound will boost profits fast. "Those are very valuable positions," says comanager Thomas Shrager.

Hyundai Motor (HYMLF)

Kia Motors (KIMTF)

Korean automakers used to be the butt of car jokes, thanks to poor engineering. Today sister companies Hyundai and Kia—Hyundai owns 33.88% of Kia, and the two share parts and technology—are having the last laugh. In 2016, Kia got top ranking in J.D. Power's annual U.S. Initial Quality Study. It was the first time in 27 years that a nonluxury brand headed the list. Hyundai came in third.

Such accolades have not protected the automakers from the economic slowdown in emerging markets. The stocks have sold off, and Kia now trades at just 58% of tangible book value; Hyundai at 44%. Browne says investors are overly pessimistic. "These stocks have gotten too cheap," he says. "The cycle will turn."

United Overseas Bank (UOVEY)

Loan defaults in the oil and gas sector have weighed on this Singapore bank, which is down 26% since 2014. Shrager says the concerns are overdone. UOB has an unusually strong balance sheet with ample reserves for nonperforming loans. And it is growing loans by about 5% a year. "It's generating a healthy amount of income," Shrager says. Meanwhile, the stock is priced at only 1.1 times tangible book value, compared with a long-term median price/book value ratio of 1.5.

Sources: Morningstar, Yahoo Finance