5 Smart 401(k) Moves to Make Now

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Blissfully, making your 401(k) grow hasn't been that hard in recent years. Since March 2009, the S&P 500 index of U.S. stocks has more than tripled in value. And thanks to the Pension Protection Act—now celebrating its 10th anniversary—many workers are automatically enrolled in 401(k)s. "Inertia has led to some pretty powerful results," says Katie Taylor, director of thought leadership at Fidelity.

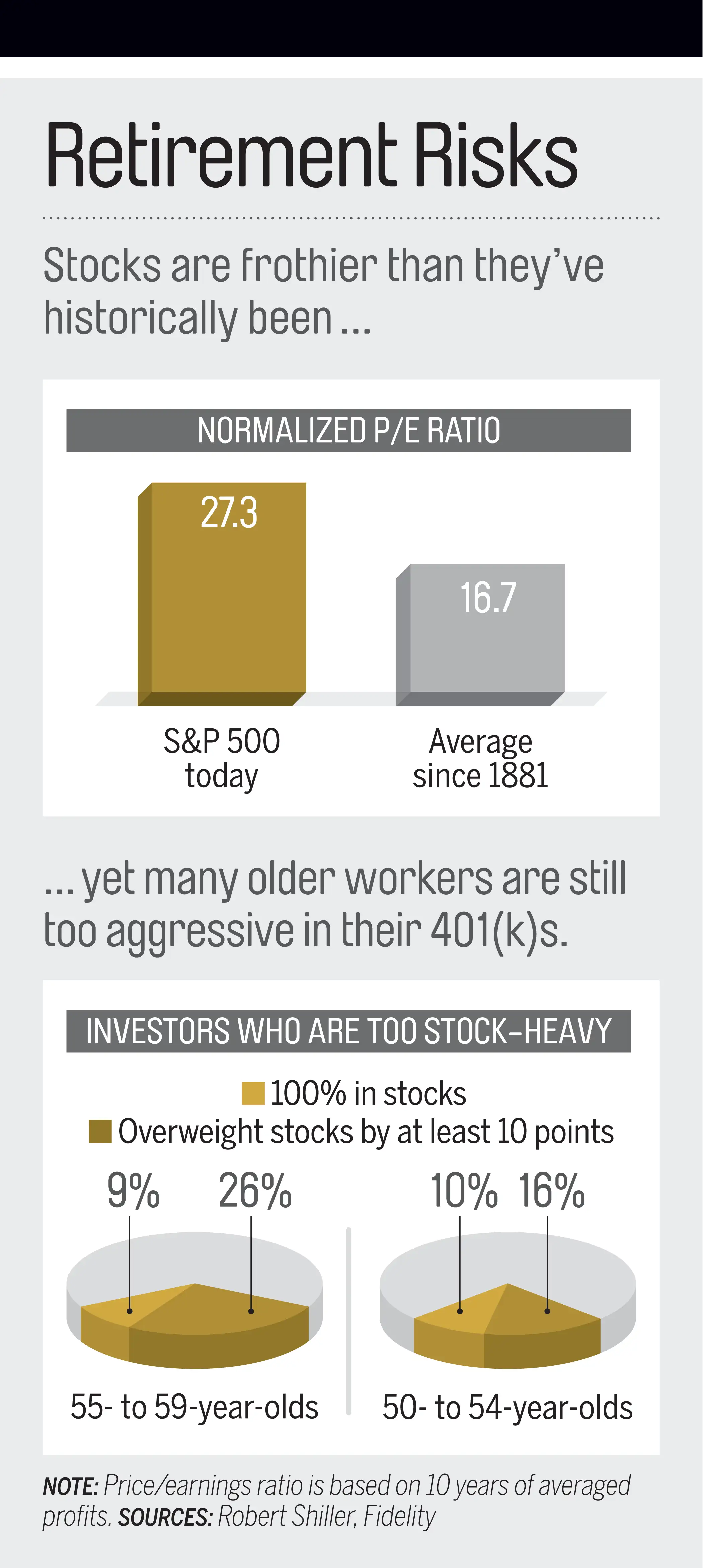

But inertia works only as long as the winds are blowing in the right direction. Today there are signs that momentum could be shifting. U.S. equities, for one, are as frothy now as they were leading up to the 2007–09 bear market and the Great Depression in 1929. The S&P 500 trades at a price/earnings ratio of 27.3 based on 10 years of averaged profits, a 63% premium to historical averages.

Meanwhile, corporate profits have been declining for five consecutive quarters, the worst such streak since the financial panic. And worried fund managers have amassed large piles of cash, according to a recent Bank of America Merrill Lynch survey.

None of this means your 401(k) needs a major overhaul. This is, after all, your long-term portfolio, meant to endure choppy air from time to time. But a few tweaks now can help ensure that inertia doesn't work against you—and that you're still on track no matter what happens in the market.

Get over your fear of bonds

If you haven't rebalanced your 401(k) in a while, it probably looks different from what you remember. Without rebalancing, a moderate 60% U.S. stock/40% U.S. bond portfolio at the end of the last recession is now closer to an aggressive 80% equities/20% bond mix, according to Morningstar.

The rule of thumb: If your weightings are off-kilter by five percentage points or more from your desired mix, it's time to take action.

Read next: Rebalance Your Portfolio or Not?

Some investors, though, may be wary of rebalancing into bonds now, notes Maria Bruno, a senior investment analyst in Vanguard's investment strategy group. That's in part because fixed-income prices fall when interest rates rise, and the Federal Reserve could lift rates before the year is out.

But "rebalancing helps protect you from short-term volatility," Bruno notes. Even if fixed-income prices fall, bonds can still serve as a cushion. The worst calendar-year loss for intermediate-term government bonds was 5.1%, in 1994. By contrast, the worst loss for blue-chip U.S. stocks was 43.3%, in 1931.

You can further reduce risk by choosing bond funds with an average "duration" of about five years or less, which are less sensitive to interest-rate moves, says Peter Mallouk, president of Creative Planning in Leawood, Kans. (A duration of five implies that if rates rise one percentage point, the fund could lose 5% in value.) You can look up this figure for your plan's fixed-income offerings at Morningstar.com. If your 401(k) doesn't offer a good low-duration option, go with a core fund such as Dodge & Cox Income , with a duration of just four years, in your IRA. The fund, which has beaten more than 80% of its peers over the past five, 10, and 15 years, is in our Money 50 recommended list.

Act your age

This means you, boomers. If you're closing in on retirement, taking stock profits off the table is even more vital. Recall that at the end of 2007, nearly a quarter of 401(k) participants 56 to 65 had more than 90% of their assets in equities, according to the Employee Benefit Research Institute. That was at the start of a bear market that cut stock values by more than half.

The situation isn't as dire now—thanks in part to the growing use of target-date funds that rebalance for you. But more than a third of 401(k) investors ages 55 to 59 still have significantly higher-than-recommended stock weightings, according to Fidelity (see chart, above).

Read next: The Right--and Wrong--Investing Risks in Retirement

Retiring into a bear can seriously imperil your security, as you would be tapping funds just as your portfolio is shrinking. Conventional wisdom says a 60-year-old should be about 50% to 60% in equities.

To minimize risk further, Mallouk suggests keeping five years' worth of expenses in short-term bonds. This will ensure that "you're not selling stocks while they're down," he says. Depending on the size of your nest egg, you may be able to accomplish this simply by shifting money from other parts of your bond portfolio.

Rotate into cheaper stocks

Don't forget to rebalance within the stock portion of your portfolio too. According to a joint study by BrightScope and the Investment Company Institute, which looked at 401(k) trends as of 2013, only 8% of these retirement accounts were invested in foreign equities—a figure that's likely lower today, given the selloff in developed and emerging-market stocks overseas.

History shows that low-priced stocks hold up better to bad news than frothy shares, according to research by investment manager David Dreman. As a result, stocks with P/E ratios in the lowest quintile posted annual total returns of 15.3% from 1970 through 2010. Stocks in the highest quintile gained barely more than half as much.

Today the lowest P/Es are found abroad. The MSCI EAFE index, a benchmark of foreign developed-market shares, for example, trades at a 16% discount to the S&P 500 based on projected profits over the next 12 months. Emerging-market stocks trade at a 28% discount.

Read next: The Case for Going Global With Your Money

So shift some of your U.S. stock allocation abroad. Research by Vanguard found that putting 40% of your equity allocation in foreign funds maximizes the diversification benefits of global investing. In a 60% stock/40% bond strategy, that means keeping 36% in U.S. shares and 24% in international equities.

T. Rowe Price says that of the 401(k) plans it administers, most offer a global stock fund; nearly a third have an emerging-markets stock fund. If your plan doesn't have a good foreign option, add one through an IRA or taxable account.

Money 50 member Vanguard Total International Stock Index , which has beaten two-thirds of its peers over the past decade, gives you exposure to developed and emerging-markets stocks for a mere 0.19% in annual expenses.

Make up ground on your own

"We can talk all we want about the market and how to invest," says Stuart Ritter, a senior resident for wealth strategy at PNC's asset management group. "But how much you save has the biggest influence on your retirement readiness." And you can save more: Last year the cap on 401(k) contributions rose from $17,500 to $18,000 annually. For workers 50 and up, catch-up contributions went from $5,500 to $6,000.

Boosting your 401(k) contributions even in the final decade of your working career can help keep your portfolio on track in the event of a lousy market. For instance, if you planned to save $17,500 a year in your 401(k) for the last 10 years of your career and earned 7% returns annually, you would add another $242,000 to your nest egg. However, if you took full advantage of the higher caps and socked away $24,000 annually, you could earn just 0.2% a year in the market and still wind up with the same amount.

If you're young, double-check how much you're saving per year. Most plans set a default contribution rate of 3% or less for workers who are automatically enrolled in a 401(k), according to Vanguard. Seven in 10 employers will automatically boost those contributions annually, but typically by just one percentage point. Yet if you boost investments now and the market soon drops, you will be picking up more shares at bargain prices. Over the long run, this can be hugely beneficial to younger investors.

Hedge your tax bets

Another way to shore up your nest egg in a shaky market is to protect yourself from future taxes. To do that, use an increasingly common feature in company retirement plans: a Roth 401(k). With a Roth, you don't get an upfront tax break on contributions, but earnings and qualified withdrawals are tax-free. Last year 58% of employers offered a Roth 401(k), up from just 11% in 2007, according to Aon Hewitt.

For young investors, Roths make sense since you'll be paying taxes now, when your salary is modest. For older workers the decision is more complicated. But Ritter argues it's still worth redirecting at least some of your savings to a Roth. It gives you flexibility in case one year in retirement you need to make a larger-than-normal withdrawal. "If that money came from a Roth, it would be tax-free," he says. You can direct a portion of your 401(k) election into a Roth; the tax code allows you to split contributions.

In the event of another major downturn, these moves won't prevent your portfolio from suffering losses. But they will lessen your fall—and allow you to recover faster in the rebound