These 7 Real People Tell Us How They Got to $1 Million

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The balance of our coverage provides a snapshot of who America's millionaires are, where they live, and how they built their wealth.

Nearly two decades ago, these five families were featured in Money as "millionaires in the making"—households that were well on their way to a seven-figure net worth excluding the value of their primary residences.

That was starting in 2000, around the time the dotcom stock bubble began to burst. Yet despite running into one of the worst bear markets in history—which was followed soon after by the global financial panic, the worst economic crisis since the Great Depression—these families still managed to achieve their goals.

How did they accomplish this? Some did it by living frugally and saving aggressively so that when the bad times hit, they had enough of a cushion. Others proved to be resilient in the face of setbacks, staying the course with their 401(k)s and IRAs in the face of a lousy economy.

Cary and Sheryl Chaitoff

Location: Solon, Ohio

Occupations: Marketing; insurance

The Strategy: Set it and forget it.

Cary and Sheryl Chaitoff hit the $1 million mark unceremoniously—there was no big party after a recent meeting with their financial planner showed that all of their assets, including their home equity, exceeded $1 million. (They're nearly there even without counting the house).

Then again, they joined the seven-figure club in about as routine a fashion as is possible. The Chaitoffs—the prototypical American family with two kids, a new house, and a new dog—are living proof that you don't need a windfall, a flashy salary, or an overly complicated investment strategy to become millionaires.

Since the start of their marriage, Cary, 50, and Sheryl, 48, have used automatic savings to build their wealth. This includes socking away at least enough in their 401(k)s to qualify for company matches— and then making additional monthly investments into the market.

After their first child was born in 2000, they tackled college savings the same way. Today, 8% of their pretax income is put into 401(k)s and another 8% (which used to be earmarked for taxable investing) goes toward 529 college savings accounts. "We have seen the benefits of continuous savings by starting young," Cary says. "We've never tried to time the market. Dollar-cost averaging and automatic savings have gotten us to where we are."

Though their strategy hasn't changed all that much, "life is a little more complicated than it was 20 years ago," Sheryl admits. The couple has bolstered their emergency savings and life insurance coverage. Cary lost his father to a form of dementia, and he and Sheryl are determined to protect their kids in the case of a similar life-changing event. "I've personally seen the financial impact a health crisis can have on a family," he says. "So we strive to prepare as much as we can."

Yet they still maintain a comfortable lifestyle. When they splurge, they do so on family experiences—vacations, summer camps—and pass on the latest gadgets. "I'd rather have the memories," Sheryl says.

Suzanne Wyatt

Residence: Las Vegas

Occupation: Actuary

Strategy: Invest in yourself.

There are two sides to Suzanne Wyatt. An actuary by profession, the 44-year-old has always been prudent. Yet there's another part of her that takes things to extremes. For instance, Wyatt is a sucker for adrenaline sports. Her indulgence of choice: flying private planes. Last year, she got her commercial pilot's license.

These two facets of Wyatt are on full display when it comes to her savings strategy. When Money interviewed her 17 years ago, she was living in a couchless studio apartment because she didn't want to invest in a stick of furniture that she wasn't absolutely sure she'd keep.

That frugality, coupled with extreme savings goals—Wyatt has continuously socked away 20% or more of her pay every year—helps explain how she nearly hit the $1 million mark in her mid-thirties by the time she married Glen Johnstone in 2006.

Wyatt has also avoided the common mistakes of most young workers. For one thing, she started saving for retirement immediately with her first job after college in 1994. Her starting salary was low, about $30,000, but she deferred as much as she could to her 401(k). When she left that job after four years, her account balance was around $30,000. But unlike most young workers who cash out their 401(k)s when they quit (which triggers a tax bill and a penalty), Wyatt stuck with it. Today, that account alone has grown to over $100,000—10% of her retirement savings.

Along the way, Wyatt's salary has also grown, as she has worked to improve her skill set with new accreditations and continuing education. Today, both Wyatt and Johnstone have rewarding careers— she's a senior consultant at a global professional services company; he's a medical-device sales rep. "We've built our careers to a point where, we're not rolling in it, but we don't have to skimp," she says. "It's a nice place to be."

Wyatt is still a careful spender, but she gets to have a little more fun than in her studio apartment days. "There's a balance," she says. "It's a matter of setting aside a little cushion each year and enjoying life to the extent that you can."

Eric Rhone

Residence: St. Louis

Occupation: Agent and entrepreneur in the entertainment industry

Strategy: Hang on to what you've earned.

When Eric Rhone's story first appeared in Money, he was still pretty green. But his photo—sly smile, nonchalant stance— said otherwise. "I'm not sure if I knew I'd make it to a million," he says. "But I was totally confident that I was going to work very hard to get there."

And he did. A celebrity manager, Rhone's career took off with that of his biggest client, Cedric the Entertainer. Rhone has well surpassed his goal; he hit the $1 million mark in 2004, he says. Now, the 52-year-old is finding that it's just as important to protect the wealth he's built as it is to focus on creating more.

Taxes are his first item of business. Fluctuating income and multiple revenue streams can make squaring up with Uncle Sam complicated for those in the entertainment industry (Wesley Snipes isn't the only horror story). But Rhone is adamant about understanding what's in each of his accounts. And he refuses to carry a tax bill into the next year.

"My golden rule is "Taxes first, then savings, then expenses," he says. "That particular formula has helped me reach my financial goals."

Luckily, he's got some help sorting it all out. Rhone employs a team of financial experts—an adviser, accountant, insurance broker, and estate planner—that he brings together quarterly. Rhone's wife, Angela, who runs the business and family books, sits at the head of the table.

After decades in the entertainment industry, Rhone has some money to play with. But he maintains his core priorities. He and his family live on about 40% of Rhone's income; put 20% toward straight savings; and invest the remaining 40%.

His portfolio is also on the conservative side: While he once used to take more risks in the stock market with individual stocks and aggressive mutual funds, Rhone's current portfolio plays it safe. Only about 20% of his portfolio is now in aggressive stocks, and the rest is in a balanced mix of bonds, staid stocks, and other conservative investments.

"As I got older, I became more conservative," he says. "I'm not 30 anymore. In 10 years I'll be needing that money."

Today, Rhone's largest expense is education; he and Angela have one child in college and two in private middle school. Travel is next on their list. The family has a second home in Los Angeles, and take frequent vacations together.

As for retirement? Well, the past 17 years have been good to Rhone, but he's not ready to call it quits just yet. Still, it's good to know that he can.

Scott and Charlene Kozloff

Residence: Charlotte

Occupations: Schoolteacher; IT administration

Strategy: Brace for life's curveballs.

When they were featured in Money 17 years ago, Scott Kozloff was an affable shoe salesman who picked stocks for fun, while Charlene was a savvy stay-at-home mom.

But along the way, things changed—as happens in life. Scott, who was growing tired of sales, enrolled in an elementary education program at the University of North Carolina at Charlotte—and for the past five years, he's worked as a public school teacher. At the same time, Charlene, who put her career on hold to raise the couple's three kids (now 22, 19, and 12), went back to work. Today, she manages administrative functions at an IT company she's worked at for 10 years. "We did a full 180—a complete role reversal," Scott says.

Career changes weren't the only surprises. In the 2008 financial crisis, their retirement savings—largely invested in the stock market—took a beating. Three years after that, they were dealt an even heavier blow: Charlene had breast cancer.

Yet the couple coped—and today, they are quick to rattle off their blessings. After months of chemotherapy and four surgeries, Charlene, now 57, has made a full recovery. Because she was diagnosed with cancer during an enrollment period, they were able to quickly change insurance coverage to better pay for her treatment. And since they had saved diligently for decades—driving cars until they broke down, treating every raise as a savings opportunity—the remaining medical bills weren't that much of a burden.

Eventually, their investments healed too. It was a rough patch, to be sure, but they weathered the storm because they didn't cash out their 401(k) at the market's bottom. They were able to do that by saving more aggressively with the extra income from Charlene's salary.

Scott, 54, still takes an active role in managing their portfolios, but even that has changed. Today he "plays" with only about half of their investments and leaves the other half to investment advisors. After the downturn, he stopped looking for "longshot" growth stocks with big potential upside. He now veers to blue chips that were depressed by the market. He still likes to invest in companies with products the couple uses, like Cisco and Microsoft. His best investment? He snagged Facebook stock in 2012 for $24 a share and sold it in 2016 at a more than 400% increase.

They have about $930,000 in their portfolio, mostly in a diverse mix of funds. But about $350,000 is held in individual stocks, with the highest percentage in shares such as Nike, Boeing, and Google.

As they near retirement, the couple are looking forward to living closer to the beach, and doing some traveling (Charlene is a scuba diver, so a diving trip to Australia is high on their bucket list).

Yet they are also committed to padding their emergency fund as much as possible. "We know how quickly things can turn around," Charlene says. "Thank goodness we thought about that 10 years ago."

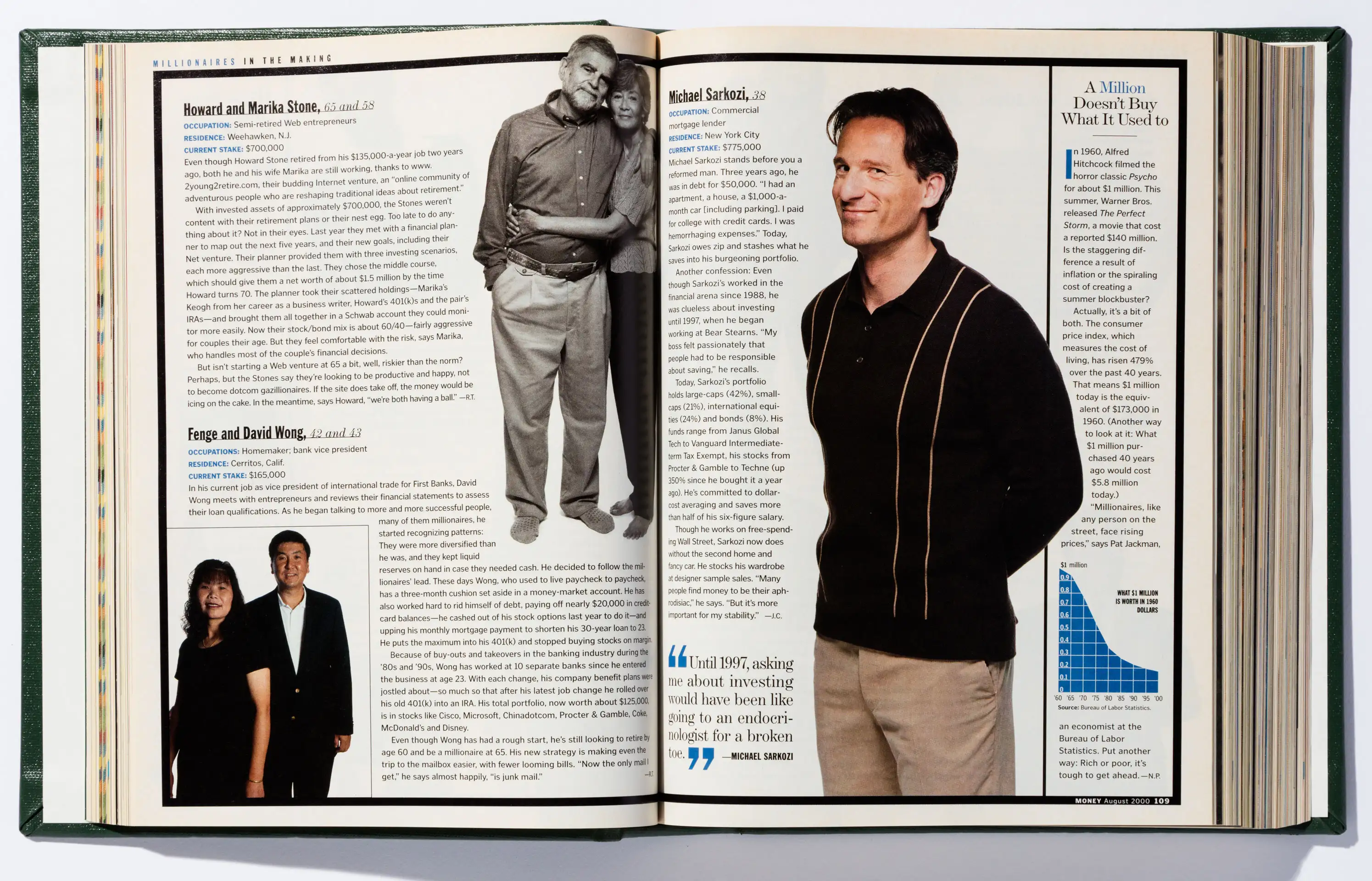

Michael Sarkozi

Residence: New York

Occupation: Commercial mortgage lender

Strategy: Stay the course.

Michael Sarkozi's financial history is a crash course in resiliency—as is the case for many members of the millionaires club. When Money first interviewed Sarkozi, he had worked in financial services for 12 years, and as a commercial mortgage lender at Bear Stearns for about three. You probably know where this is headed.

At the height of the subprime mortgage crisis, Bear Stearns collapsed, and its employees faced massive layoffs. Sarkozi, fortunately, hung on to his job. But as business dried up, he spent entire days watching the sun rise, and then set, in his Madison Avenue office. By the time the smoke cleared, his net worth, largely vested in the stock market, was nearly depleted. "Life was completely derailed," he says. "It was a terrible time for the whole country."

But Sarkozi kept a level head. When the market came back, so did his book of business. When JPMorgan Chase bought Bear in 2008, he was one of the lucky few who got an offer to stay on. He's now a managing director in Wells Fargo's banking group.

Sarkozi built back his net worth gradually—also by keeping a level head. Like many investors, "I shifted my portfolio a bit—from one industry or asset class to another," he says. "But just cashing out wouldn't be good long term. I would have lost the opportunity of a rising market."

Today, Sarkozi is less exposed to stocks than he was when Money first interviewed him. He keeps roughly 48% of his portfolio in stocks, about 40% in bonds and cash, and 12% in alternative investments (like private equity) and real assets.

But that's to be expected, as he's older now, at 55. Sarkozi also married his longtime partner, Ron Shuma. The couple make sure they have enough wiggle room in their budget for charitable donations—such as to the LGBTQ nonprofit Live Out Loud.

When Money first spoke with him, Sarkozi made a case for using money as a means of stability, rather than as an "aphrodisiac." After navigating a volatile career and market, and one of the worst downturns in history, he's proved his point.