I'm $37,000 in Debt and Haven't Made a Payment on My Student Loans in 5 Years. How Can I Fix This?

This is the first installment of Money Makeovers, a series where we put together a financial plan for people in terrifying financial situations. Follow us on YouTube to receive a notification when new episodes are published.

At her desk job in the office of a marina, KC Susskind regularly watches customers spend thousands of dollars on boat maintenance. A part of her always wants to blurt out: How do you afford this?

KC, 29, can't remember a time when she didn't struggle with money. She's never learned how to save. She and her husband, Ryan, 28, have to scrimp to afford necessities. Now eight months into their marriage, the couple want to turn things around before financial strains burden their relationship. "It's terrifying. I'm so scared of living my life this way," KC says. "I have so many things I want to do, and I want to figure out how to do them."

To help the Susskinds get started, Money connected them with two experts: Ramit Sethi, author of the New York Times bestseller I Will Teach You to Be Rich, and Douglas Boneparth, a New York City–based certified financial planner who specializes in working with millennials. The help is coming not a moment too soon. KC thinks about money—and how they don't have enough of it—every morning when she wakes up, she says. It's suffocating. When she buys a coffee, she thinks what bill that $3 could go toward. When she needs new clothes, she feels guilty as she walks out of the store. "It's the worst of both worlds," Sethi tells KC. "You feel guilty, but you keep doing it."

After consulting with the pros, the Susskinds walked away with a three-point plan:

1. Master Cash Flow

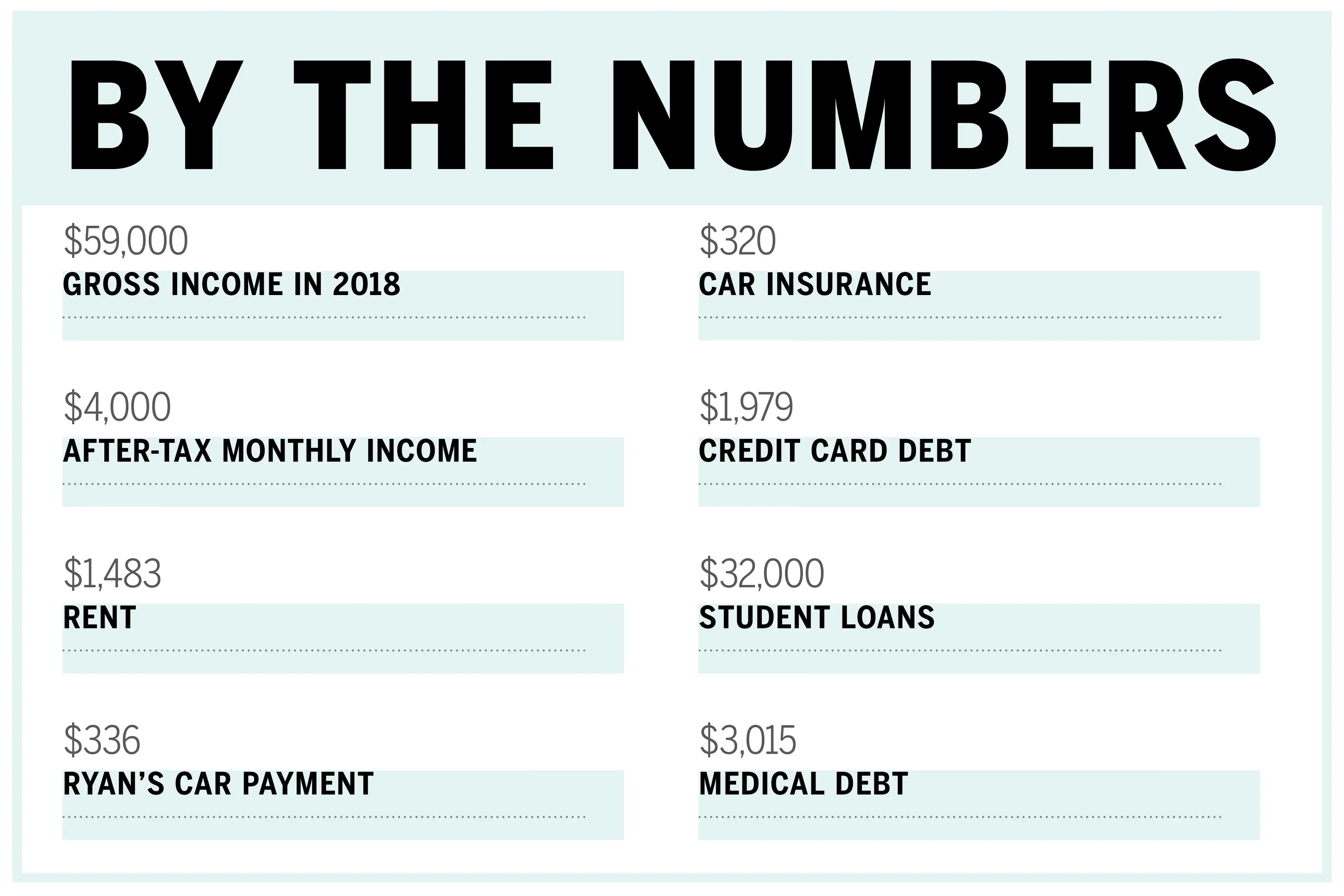

Nearly 40% of KC and Ryan's monthly take-home pay of $4,000 goes toward rent for a one-bedroom apartment in Freehold, N.J. Car payments and insurance eat up another chunk. So does gas—KC estimates she spends about $60 a week to fill up her tank.

As for the rest? KC isn't sure. "On paper, you're thinking, I made so much money. Where does it all go?" she says.

That's the exact question Boneparth wants her to answer. KC and Ryan need to analyze 12 months of spending and categorize their purchases. That will help them understand exactly where every dollar is going so they can identify areas to cut. Boneparth recommends using Tiller, a tool that for $5 a month automatically updates a spreadsheet as you spend.

2. Attack High-Interest Debt

The couple's credit card debt is Boneparth's primary concern. While the balances on the two cards KC has and a third they share total only $1,979, all three cards are maxed out. And the interest rates—each above 26%—are toxic.

KC recently paid off loans for her 10-year-old Jeep, which should free up roughly $300 a month to put toward those payments.

Next, Boneparth wants KC to call up the collection agency that's handling her medical debt and set up a structured payment plan or negotiate to pay a reduced amount. She has $2,015 in collections, plus $1,000 that is overdue.

KC's student loans from her communication degree at Monmouth University, which total $32,000, are the least worrisome of her debt. She hasn't made a payment in five years, however, so the balance continues to grow. KC wants to enroll in an income-driven plan that will reset her payments based on how much she earns. Boneparth agrees that's a good idea. But those plans can result in payments that are so low they don't cover interest each month. Aim to pay off at least the interest, he says.

3. Build Some Protection

Part of the reason KC and Ryan have struggled this year is that they have no savings to protect them when they're hit with an unexpected expense. In January, for example, KC was laid off for a six-week period when business was slow at the marina. During that span, Ryan, who works at a plumbing-supply warehouse, totaled his car.

That's why they need some cash set aside. As soon as they've eliminated their credit card debt, Boneparth wants the couple to build up three months of living expenses—an amount they should be able to figure out once they've mastered their cash flow. Then they can turn to longer-term financial goals.

Now the Susskinds have to decide how uncomfortable they want to get, Boneparth says. On the extreme end, if they could move in with a relative and redirect at least $1,400 a month to debt payments, Boneparth estimates they could wipe out what they owe in three years. On a smaller scale, KC says she can start saving at least $30 a week by bringing her lunch to work.

"It's easy to say, but it's hard to do," Boneparth says of changing financial habits. "We're asking people to change behaviors they've been adapted to for a long time."

To help with that goal, Sethi wants KC to picture her life four years from now. You've done everything on Boneparth's list, he says. Your debt is gone. Your emergency savings are healthy. Where are you?

Starting a family in an apartment or home, she says. And experiencing the world without the constant worry of debt.

What would that feel like?

"A victory," she says. "A really big victory."