Profit Growth Is Slipping and That's Not Good for Stocks

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The fact that companies have been consistently generating record profits in recent years has certainly been a boon to the S&P 500 .

Unfortunately, there will come a time when corporate earnings growth will inevitably slow — and that time may be now.

A government report released in late May found that overall corporate profits actually slumped in the sluggish first quarter, when a brutal winter weighed on business activity. The Bureau of Economic Analysis says that a key measure of corporate earnings fell 3% in the first quarter, compared to the fourth quarter of 2013. Versus the same period last year, profits slumped much more — 9.8%. This is true for both financial and non-financial companies.

Now, there are a variety of ways to measure the health of profits. In the private sector, economists often look at overall earnings growth for companies in the S&P 500.

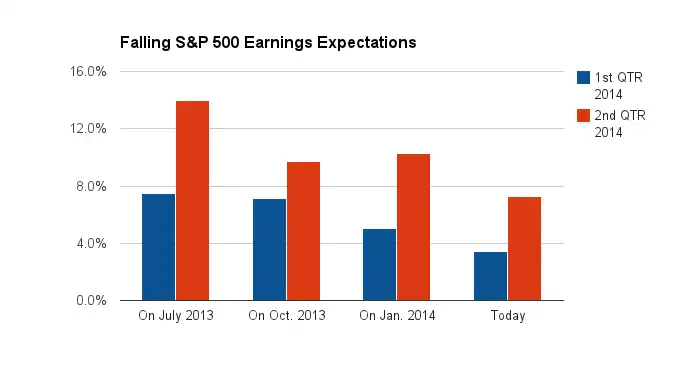

By this measure, profits are still climbing, but the rate of that growth is slowing noticeably. In fact, expectations for both first quarter and second quarter earnings have been cut in half in less than a year.

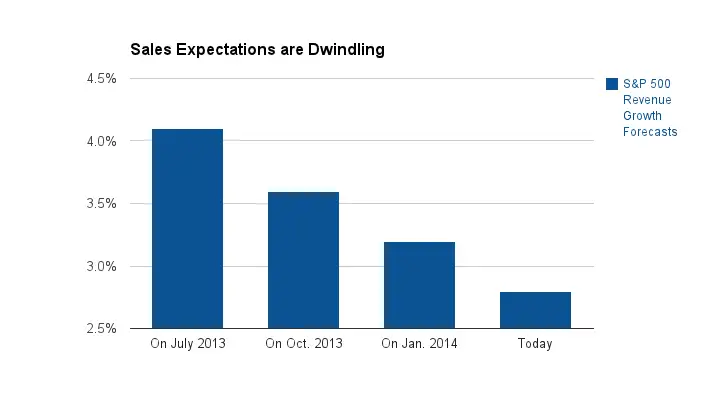

A big reason why is that the economy is not rebounding as strongly as was thought, and overall corporate revenues are growing only modestly.

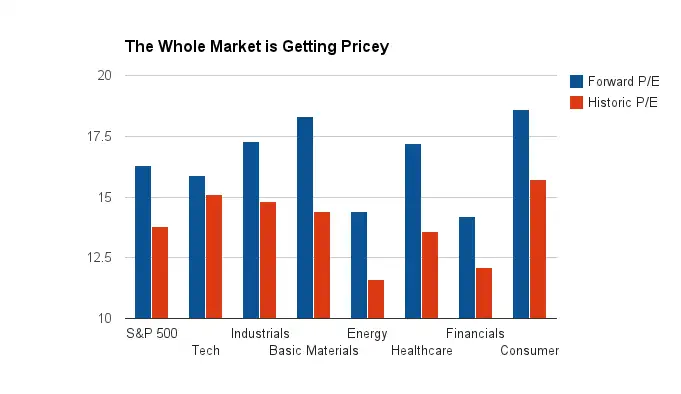

Yet stock prices have been surging faster lately than the rate of both earnings and revenue growth. "Over the past few years multiple expansion has been the key factor lifting equity market levels higher," notes Tom Stringfellow, chief investment officer for Frost Investment Advisors.

Indeed, virtually every part of the stock market is now trading at higher price/earnings ratios — based on forecast profits over the next 12 months — then they have historically. And that's never a good sign.