Why I Won't Own Bond Funds in My Retirement Portfolio

When stocks took a tumble last week, financial pundits were quick to call it a “potent reminder” to investors of the importance of having some bonds in your portfolio for their perceived safety and yield. The classic mix is supposed to contain 60% stocks and 40% bonds, with bonds supposedly cushioning the risk of equities. In the eyes of most investment experts, I would be considered foolish to be 100% in stocks, as I have been ever since I started investing.

But I’m not sure what bonds they’re talking about. Yes, last week the yield on a 10-year U.S. Treasury note surprised everyone by falling sharply to 1.85%, as bond prices soared—when bond prices rise, bond yields fall, and vice versa. Treasury yields edged back up to 2% the next day, as stocks rebounded. Wall Street experts are still trying to determine the reasons behind the 10-year Treasury note's plunge, which stunned investors and traders.

But that was a one-day event. When you look at the decline in bond yields over the last three decades, I don’t understand how it is mathematically possible for Treasuries—known as the safest bond possible—to protect a stock portfolio against major shocks over the next 20 years.

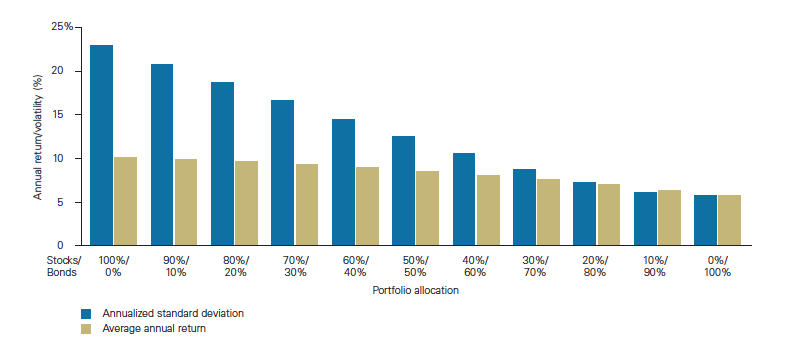

No question, falling interest rates have been a boon to fixed-income investors over the last three decades. The yield on a 10-year bond has fallen from 14% in 1984 to 8% in 1994 to 4% in 2004 to about 2% today. The decline hasn’t been non-stop—bonds have rallied along the way—but the overall downward trend has most certainly pushed up fixed-income returns. As a result, bond funds have both made money and helped lower risk in a portfolio. This chart created by Vanguard, based on market data between 1926 and 2011, shows the impact of adding bonds to dampen volatility (as measured by standard deviation), while not drastically reducing returns.

But those conditions, and that steady decline in rates, no longer exist. Today we have an environment where rates have very little room to fall and at some point will go up (we just don't know when). Once rates finally rise, bond prices will fall, which means investors will lose money. So when someone recommends diversifying one’s portfolio with bonds these days, I wonder: is there some kind of bond that’s immune to interest rate rises that I don’t know about?

Junk, or high-yield, bonds certainly don't fit the bill as they are also vulnerable to rate hikes. Moreover, there have been warnings that the accumulation of high-risk corporate and emerging markets bonds by mutual fund companies such as Pimco and Franklin Templeton could create a liquidity crisis in the future. Investors have been pouring money into these funds, but shocks could turn into even larger debacles when investors look to liquidate and the large amounts held by fund companies become hard to sell.

Short-duration bond mutual funds might be less affected by rising interest rates. Fidelity has a whole suite of such funds, which the fund group says “can help investors in a low and/or rising rate period.”

There are also mutual funds that “ladder” bonds with staggered durations so that a portion of the portfolio will mature every year. The goal of these laddered bond funds is also to achieve a return with less risk over all interest rate cycles.

The problem for investors saving for retirement is that the returns on such funds are so low that it’s hard to justify allocating anything to them other than savings you will need in three to five years.

I won’t be retiring for another several decades, so at this point, a market crash isn’t really my greatest risk. My greatest risk is not growing my retirement account as much as humanly possible over the next ten to 15 years. To meet that goal, I think I should stick with equities and use any future crashes as buying opportunities. I’m not 100% comfortable with that decision, but I don’t feel I have much choice. I would love to find a bond fund that could be both a safe haven and could provide steady returns, but I just don’t think that exists anymore.

Konigsberg is the author of The Truth About Grief, a contributor to the anthology Money Changes Everything, and a director at Arden Asset Management. The views expressed are solely her own.

More on investing:

Should I invest in bonds or bond mutual funds?

What is the right mix of stocks and bonds for me?

How often should I check my retirement investments?

Read next: Why Americans Can’t Answer the Most Basic Retirement Question