How to Make Your Savings Last for Decades, According to a 96-Year-Old Retirement Expert

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Lots of retirement experts theorize about how best to plan for the thirty-plus years you hope to enjoy after hitting 65. When Jack Guttentag — who turned 96 last December — gives advice, he’s speaking from experience.

Guttentag, an economist who retired from the University of Pennsylvania’s Wharton School in the late 1990s, founded the website the Mortgage Professor in 2011, which he still runs. In addition to helping homeowners, the site promotes reverse mortgages, which Guttentag argues is an under-used way for older Americans to tap housing wealth to cover retirement costs.

Most of us can’t hope to share the nonagenarian's killer work ethic. But Guttentag says planning for a long, financially secure retirement isn’t as hard as you think. He recommends diversifying your career, and, of course to saving as much as you can. But adds that obsessing over hard-and-fast rules the financial services industry sometimes promotes isn’t necessary.

“It’s about having money in ways that benefit you,” he says.

A 70-year career

Guttentag graduated with an engineering degree from Purdue University in 1948. After earning a masters and Ph.D. in finance from Columbia, he began a banking career at the Federal Reserve Bank of New York, but eventually left to pursue teaching at Wharton.

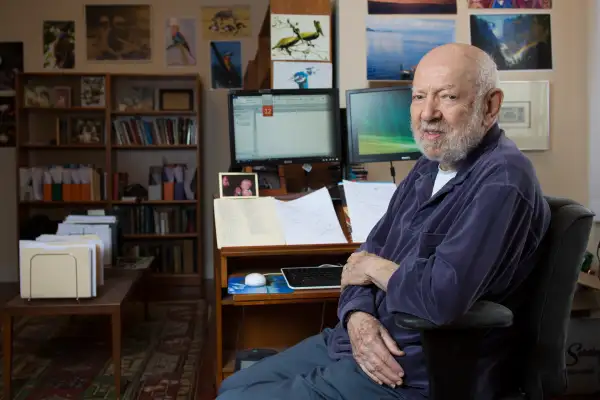

Today, he runs the Mortgage Professor website from the retirement community where he lives in Gladwin, Pa. Guttentag starts his workday around noon and spends his days building tables, writing and sifting through financial data. In addition to his business, Guttentag regularly writes on retirement topics for financial publication Forbes. Food is delivered to his door each morning and most of his interactions are done virtually. “I sometimes go until 2 o’clock in the morning because I can,” he says.

Looking back, Guttentag says he tried to shift his interests throughout his career. “I didn’t want to retire from [the bank] along with a gold watch,” he says.

It’s advice he repeats to others: “It’s very useful as you go through your working life to diversify your interests and capacities — so you don’t get stuck in one vineyard and find it boring,” he says.

That means there were times when he listened to his heart over his wallet.

In one instance, a semester-long opportunity to teach abroad in Iran in 1970 turned into a jet-setting trip with stops in Egypt and Ethiopia for a year. “It was the highlight of my life,” says Guttentag who purchased four round-the-world airline tickets and traveled with his wife and his two school-aged children. “There were heavy expenses incurred.”

Another time, he pursued academia after eight years in finance — just two years shy of having a pension. “It was a hard choice to make because I was losing so much, but I wanted the freedom to do my own research and to explore other possibilities,” he says.

Rethinking retirement strategies

These days, Guttentag is focused on retirement savings.

He’s quick to correct a common misnomer: Rigid rules about how much you’ll need to save for retirement don’t exist.

“What’s the point when you’re 40 years old of trying to guess how much you’re going to need 25 years later?” says Guttentag, who was married for six decades before his wife passed away in 2017. “My objective was to generate as much wealth as possible and I knew that the more that I could accumulate, the better my position would be.”

On the other hand, he does recommend maxing out retirement savings vehicles. “You put in as much into those accounts as you can and certainly as much as you can to avoid paying taxes,” he says. “Not taking advantage of that great benefit is a violation of your self interest.”

That kind of mindset also helps prevent a last-minute retirement savings crunch or the need to make risky investments in your later years, he adds. “When you’re on the cusp of retirement, it’s too late to exercise a lot of discretion,” he says.

From home ownership to cash flow

Guttentag says his new career goal is to help retired homeowners to understand the financial options available to them – even if those tools are not being widely used. Specifically, Guttentag is passionate about reverse mortgages for the millions of retirement-age homeowners who need additional cash to live off of. Reverse mortgages allow homeowners “in the cash-poor-house-rich category” to convert part of the equity of their home into cash and pay back the money after selling the home, he says.

While critics say reverse mortgages can be a risky form of debt or result in foreclosure, proponents including Guttentag embrace them because they help address a cash crunch when few other options are available. “The existing retirement facilities are not well designed for the person who doesn’t have a pension to rely on,” he says.

As the economy falls into a longer recession, these retirement savings vehicles will only become more relevant, he adds. Currently, Guttentag is working to build broader interest in reverse mortgages by helping retirees integrate them into their retirement plan along with annuities and financial asset management.

“There is a group of retirees whose sole wealth is in their home and it’s getting larger, so the need for the kind of integration will be greater,” says Guttentag who is funding his venture by tapping into savings from a software business he built in the 90s and sold in 2005.

Staying active

Publishing research on retirement finance issues allows him to keep his mind sharp while staying busy. Four independent contractors are helping him build his website's tools; his grandson is now his attorney. The ability to put out meaningful work is especially important during a time when most of his in-person interaction has been replaced with Sunday morning family Zoom calls, he adds.

With no plans to stop, he’s determined to find new ways of working that still feel doable at his age. Running a business “is probably why I’m still functioning,” says Guttentag. “It engages my interest, and it’s what gets me out of bed in the morning.”

More from Money:

Before You Take an Early Retirement Buyout, Complete This 6-Step Checklist

How to Get Back on Track After Tapping Into Your 401(k) in a Financial Emergency

Everything You Need to Know About Reverse Mortgages

An earlier version of this story stated Guttentag's nephew, not his grandson, was his attorney.