Your Portfolio Is a Mess. Here's How to Tidy It Up

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

As you wade through your tax statements this spring and cast about for something to hurl out the window, here's a suggestion: How about getting rid of some funds you bought years ago and lost track of?

Think of it as a complement to rebalancing. In addition to routinely checking to see if your mix of mutual funds is right, regularly "ask yourself why you hold each fund," says Myhanh Hoskin, senior financial consultant at Charles Schwab. "Is the reason still there?"

You may own funds that seemed like a good idea years ago, but you might also have a hard time remembering what that idea was. Plus, odds are good that your goals—and some of your funds' managers—have changed since you bought them way back when.

- Read more: The 50 Best Mutual Funds and ETFs, Period

Cleaning house could do your portfolio worlds of good. Here are a couple of tips.

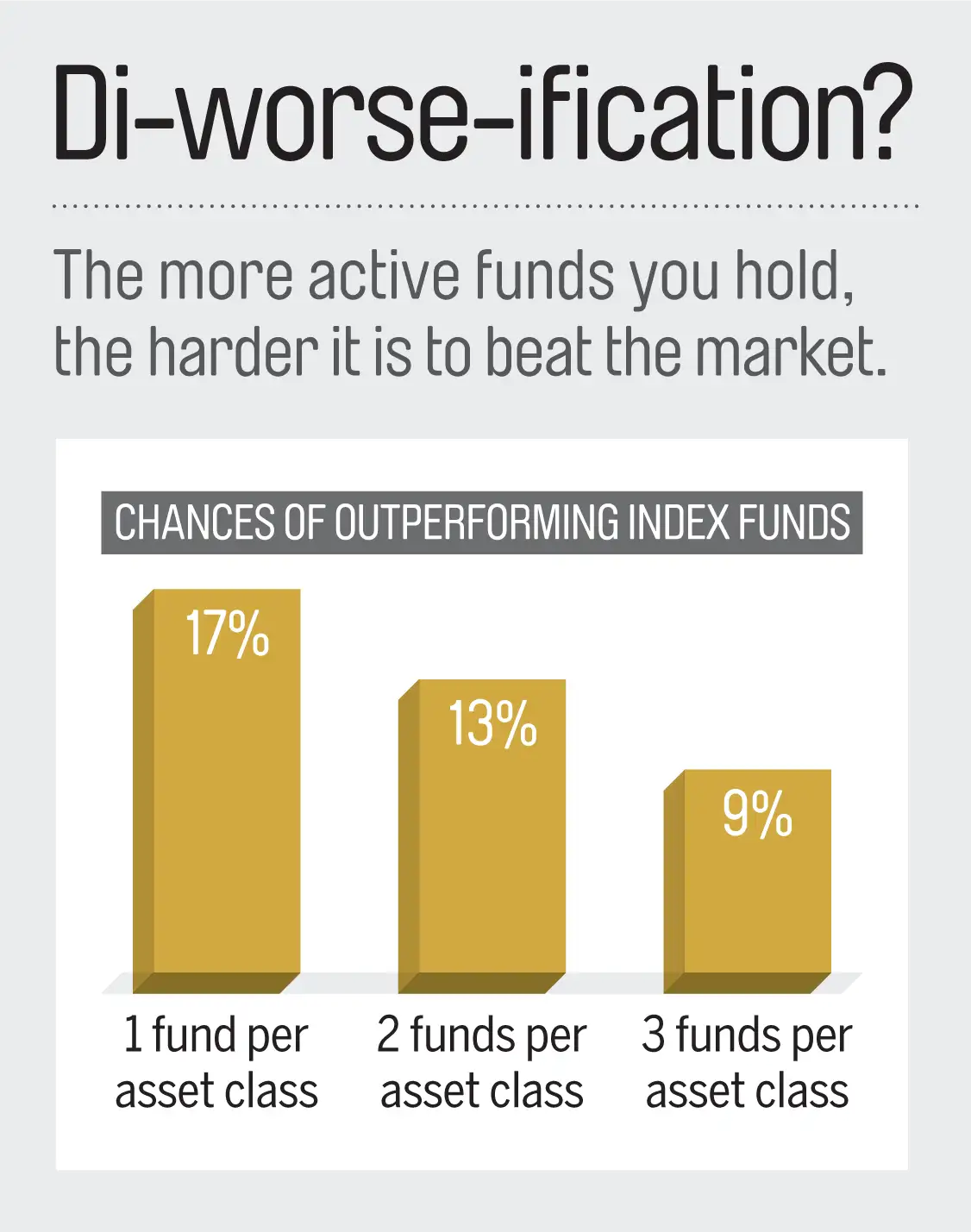

Less Is Often More

Owning a multitude of funds may seem like another form of diversification—but accretion is a problem. Among your various retirement plans and taxable accounts, you probably have several that own the same type of investments. (To find out if there's overlap, you can use Morningstar's X-Ray tool.)

What's the harm? You don't really need three large value funds. And hold too many funds and you'll collectively own so many stocks that eventually your returns will look remarkably similar to a broad-based index, such as the S&P 500.

If indexing is what you want, you can buy a fund that mirrors the S&P 500 for as little as 0.04% a year. Creating an index strategy by holding too many funds may end up costing you nearly 1%. Plus, it defeats the purpose of buying actively managed funds—to try to beat the market. (See chart at left.)

How to Prune

Start with the basics: Ask yourself if the funds you own still match your goals and time horizon. Those volatile growth funds may have been just what you needed in your youth but may no longer be suitable if you're about to take minimum distributions from an IRA.

Spring tax-prep season can also be a good time to do some pruning, says Maria Bruno, senior investment analyst for Vanguard. "Assess not only if there's overlap, but also tax inefficiencies to minimize," she says. Are any of your duplicative funds generating greater-than-average capital gains distributions? Conversely, are any sitting on capital losses? That may be the perfect trigger to sell, as you can reset your strategy while lowering your taxes.

Worried you may be tossing out too many funds? Don't be. You can form a solid portfolio with just four, says Hoskin: a large-company U.S. stock fund, a small-company stock fund, an international equity fund, and a bond fund. And if managing even that seems like too much work, there's no shame in using a single target-date fund, says Bruno.

"The beauty of an all-in-one fund is that you get a high level of diversification across all asset classes," she says—without ever having to worry about pruning.