How to Choose the Best Student Loan Repayment Plan for You

- How to Pay Off Student Loans Fast

- Biden Reveals New Student Loan Forgiveness Plan — Here's What Borrowers Can Expect Next

- How Student Loan Borrowers Can Prepare for Big Changes Coming in 2023

- Here's Exactly What the Student Loan Forgiveness Application Will Look Like

- Student Loan Payment Pause Extended Through End of 2022

More than a million class of '16 grads who took out federal loans for college will make their first payments this month. They'll also face a decision with potentially costly consequences: which of the growing number of repayment plans to choose.

But they aren't the only ones who should take a close look at their options. Anyone who still has federal student loan debt might benefit from switching plans—even if your college days are well behind you. Some of the payment plans will sharply reduce your current bill but cost you more in the long run. Others have the opposite tradeoff: larger payments now but a lower outlay overall. To decide which type is right for you, ask yourself these questions.

1. Can you afford the standard monthly payment?

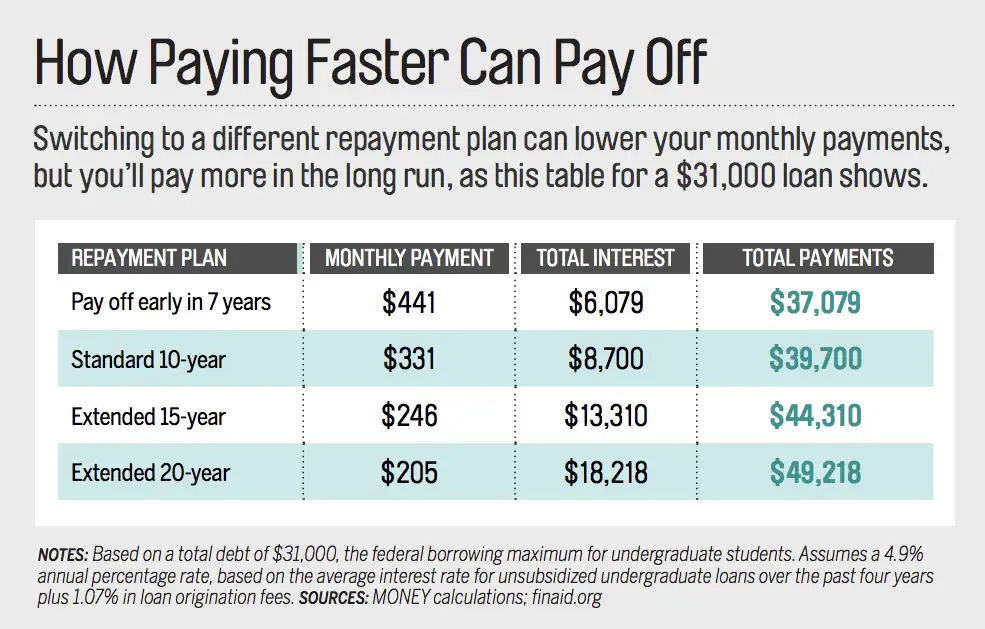

If you're starting repayment on federal student loans this year and don't do anything, you'll automatically be put into a standard 10-year plan with 120 equal monthly payments. You'll pay less in this program over the long run, so it's usually your best bet if you can afford it.

To determine that, add up all of your monthly debt obligations, such as credit cards and car payments. If you're a recent grad with an early-career salary, the total generally shouldn't exceed 10% of your pretax pay, says Mari Adam, a certified financial planner in Boca Raton, Fla. So, for example, if your salary is $40,000 a year, and your student loan would push your total debt bill to over $333 a month, you should look to a plan that will extend your payments or tie them to your income. You can use online tools, such as the new student loan calculator by 1st Financial Bank, to see what share of your income will go toward student loan payments.

Even if you can handle the standard payments, you should switch to an income-driven repayment plan if you work for a nonprofit or a government agency. That's because your remaining debt will be forgiven after 10 years of payments.

2. Do you need to reduce your monthly outlay?

Though it may be costlier in the long run, an extended or income-driven plan can ease your cash crunch now.

Extended plans stretch your payments over a period of up to 25 years. To qualify, you may have to consolidate all of your government loans into a new one. Your new interest rate will be based on the weighted average of your existing loans' rates—likely to be about 5% for the class of 2016. As with a standard 10-year plan, your payments will be fixed for the life of the loan.

Income-driven plans also stretch out your payments, but because they're set at 10% or 15% of take-home pay, the amount can change each year. Your payments may be lower at the outset, but they'll rise if your salary does.

Income-driven plans have the added benefit of loan forgiveness. Though your debt can be erased after 10 years if you work for the government or a nonprofit, the period is at least 20 years for everybody else. As a result, many borrowers will have paid off their debt before forgiveness starts, notes Mark Kantrowitz, a financial aid expert. What's more, the forgiven amount is taxable, which is not the case for government or nonprofit workers.

There are five types of income-driven plans, each with its own terms and eligibility requirements. For example, the newest one, Repaye, is open to anyone, but if you're married, your payments will be based on your income plus your spouse's instead of yours alone, so you'll most likely pay more than you would in a different plan. You can learn more about the five plans and sign up for them at studentloans.gov.

3. Do you want to pay your debt off even faster?

You might be able to get a lower interest rate if you refinance with a private lender, freeing up cash to pay your loan off faster. But there's a catch or two. For one, you'll lose the option of ever switching to a more flexible federal plan. Plus, the best rates, sometimes as low as 3.5%, can require a credit score in the high 700s, above-average earnings, and sometimes a cosigner, says Adam Minsky, a lawyer in Boston who specializes in student debt.

A better approach for most grads is to stay in the federal program and simply kick in an extra, say, $100 each month.