Why This "Tech Bubble" Isn't Like the Last One

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

- What Happens If the Social Security Trust Fund Runs Out in 2034?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

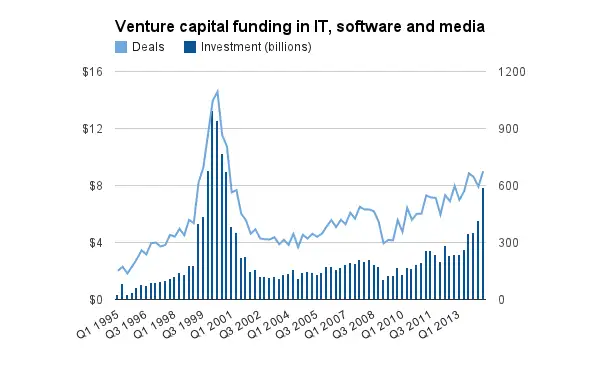

Venture capital investment—that is, money flowing into companies before they go public—is on a tear in the technology sector. At least in nominal terms, investments are at levels not seen since 1999. The comparison to the turn-of-the-millennium is a bit less impressive adjusted for inflation, but the recent trend remains boomy. (Hat-tip to Business Insider for pointing us to this data.)

So how is this boom different from last one? To borrow from blogger Joshua Brown, if it's a bubble, it's "a rich man's bubble."

Not only are you and your friends (mostly) not getting into the excitement by chasing hot IPOs — such as this week's public offering from the Chinese e-commerce giant Alibaba — you also aren't sharing in the boom in a much more tangible way. The late-1990s boom was a pretty great time for job seekers.

Remember the last boom: The build-out of the Internet was part of a high-pressure economy with plentiful jobs. New web retailers were opening warehouses and distribution centers, and fiber optic cable was going in the ground (much too fast, it turned out). In my own little corner of the world, newspapers and magazines were setting up big digital newsrooms that ran alongside still staffed-up print teams. Information technology was raising productivity in surprising places—big-box retailers reaped many of the gains—and for a time business was so competitive that employers had to share more wealth with workers. Unemployment dipped below 4%.

The latest influx of cash, and the speed with which companies are burning through it, in Silicon Valley has a lot of people worried we're in a new bubble, perhaps fueled by the Federal's low interest rates. A few months back, BI's Joe Weisenthal made the contrary case: Venture money isn't flowing as strongly into other industries, so this isn't only about cheap money burning holes in investors pockets. Rather, something's going on specifically in tech: With a fairly small investment in resources and people, a tech company with a great idea can quickly scale up to be a huge business. Think Whatsapp, or for that matter Facebook, which become a giant media company by leveraging free content provided by its users. Investing in these ideas is a high risk lottery, but great for the investors who win it.

The flip side is that it doesn't seem to be much of a jobs engine outside of the expensive parts of northern California, or unless you count odd jobs from Task Rabbit. Do we have a bubble? Maybe. Maybe not. Do we have a well-balanced economy? No.