The Three Things Gen X'ers Should Be Doing In Their 401(k)s

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The big things you have to get right in your 401(k) don't vary by age: Pick a diversified mix of stock and bond funds. Keep costs as low as you can, using index funds if that's an option. Don't chase hot performance. But there is some advice that will matter more to you if you instantly know who's a brain, an athlete, a basketcase, a princess, or a criminal.

1. It's go time

Yes, you should ideally save a lot over your entire career. The truth is a lot people aren't great about this in their 20s and early 30s. Young people have school debts to pay off and households to set up. And, let's be honest, they have lots of free time to do fun stuff, but not such big paychecks to fund it. Maybe that sounds like you. (It certainly sounds like me.) The feeling that you are already behind can be paralyzing.

But here's the thing: You still have time to make up lost ground. And you've entered your peak earning years. If you save a given percentage of your income today, that may be a bigger chunk of money than it was when your career was just getting going.

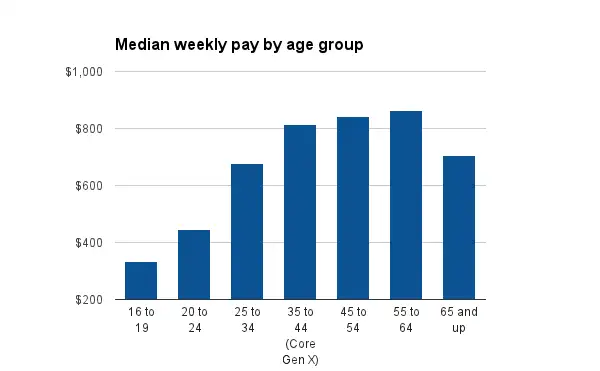

Let this be a spur to you as well. As you can see above, at your age, you likely don't have any lifestyle-changing raises in your future. (Sorry.) There's not going to be a better time than now to save money.

2. Think 17%

How much you really need to save for retirement at this point depends on how much you already have. But about 17% is a good mental anchor if you want to get your savings at least roughly right now and do the math later. The amount is far more than the average 401(k) contribution of around 6% or 7%. But take a deep breath. That number includes the contributions from your employer.

Where's the number come from? Wade Pfau of the American College of Financial Services calculated the savings rate required to safely fund a typical retirement goal. About 17% is the number he came up with for people who start from scratch with no savings at age 35, with a 60% stock/40% bond portfolio. You might do okay saving less than that if stock and bond markets go your way, but Pfau's number is what it takes to get there even with poor returns.

Don't delay. Wait until 45 to start, and the from-scratch required safe savings rate goes to 36%.

3. Review your risk

For young savers, market risk can be a bit of an abstraction. The amount you saved by your early 30s is probably on the low side, so even a steep market slide means losing fairly modest pile of actual dollars.

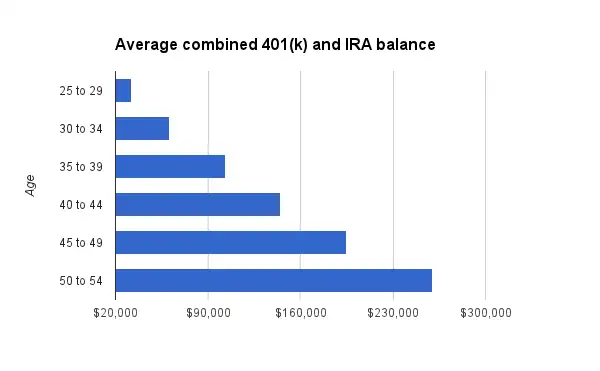

Around age 40, though, the numbers involved change. The average retirement account, according to a survey by Fidelity, crosses over the psychologically important six-figure line. Big losses feel real.

So if you haven't thought much about your portfolio lately, try this exercise. Figure out how much, in dollar terms, of your retirement accounts are in invested stocks. (If you have a fund, such as a target date fund, that combines stocks and bonds, be sure to include the stock portion of that fund in your total.) So imagine losing half those dollars. The S&P 500 fell by roughly 50% from top to bottom during the 2007-2009 crash, before rebounding. It could happen again. If you count up the possible losses and they feel like too much for you to stomach, meaning not just that you'd hate it but that you'd be tempted to sell, then trim back now.

That having been said, don't be too afraid of market volatility. You have a lot of good earnings years ahead of you, and can likely bear some risk to get a better return.