Get the Most From Your 401(k) at Any Age

- The Conventional Money Wisdom That Millennials Should Ignore

- The Three Things Gen X'ers Should Be Doing In Their 401(k)s

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Millennials

Start small, then auto-escalate. Less than half of workers ages 22 to 32 are saving for retirement, despite how painless it can be. Socking away 3% of a $50,000 salary ($1,500 before taxes) costs you less than $22 a week in take-home pay. Then take baby steps by auto- escalating your savings by one percentage point a year. In plans with auto-enroll and a 1% auto-escalate feature, nine in 10 participants are able to safely generate 60% of their age-64 income, adjusted for inflation, according to EBRI.

Take the easy way out. More than two in five millennials in retirement plans aren’t familiar with their investment options. No problem: Just go with a target-date fund, which automatically adjusts your portfolio to be less risky as you age. The worst-performing target-date investors at Vanguard earned 11.8% annually over the past five years, far outpacing the worst DIYers, who gained just 2.1%.

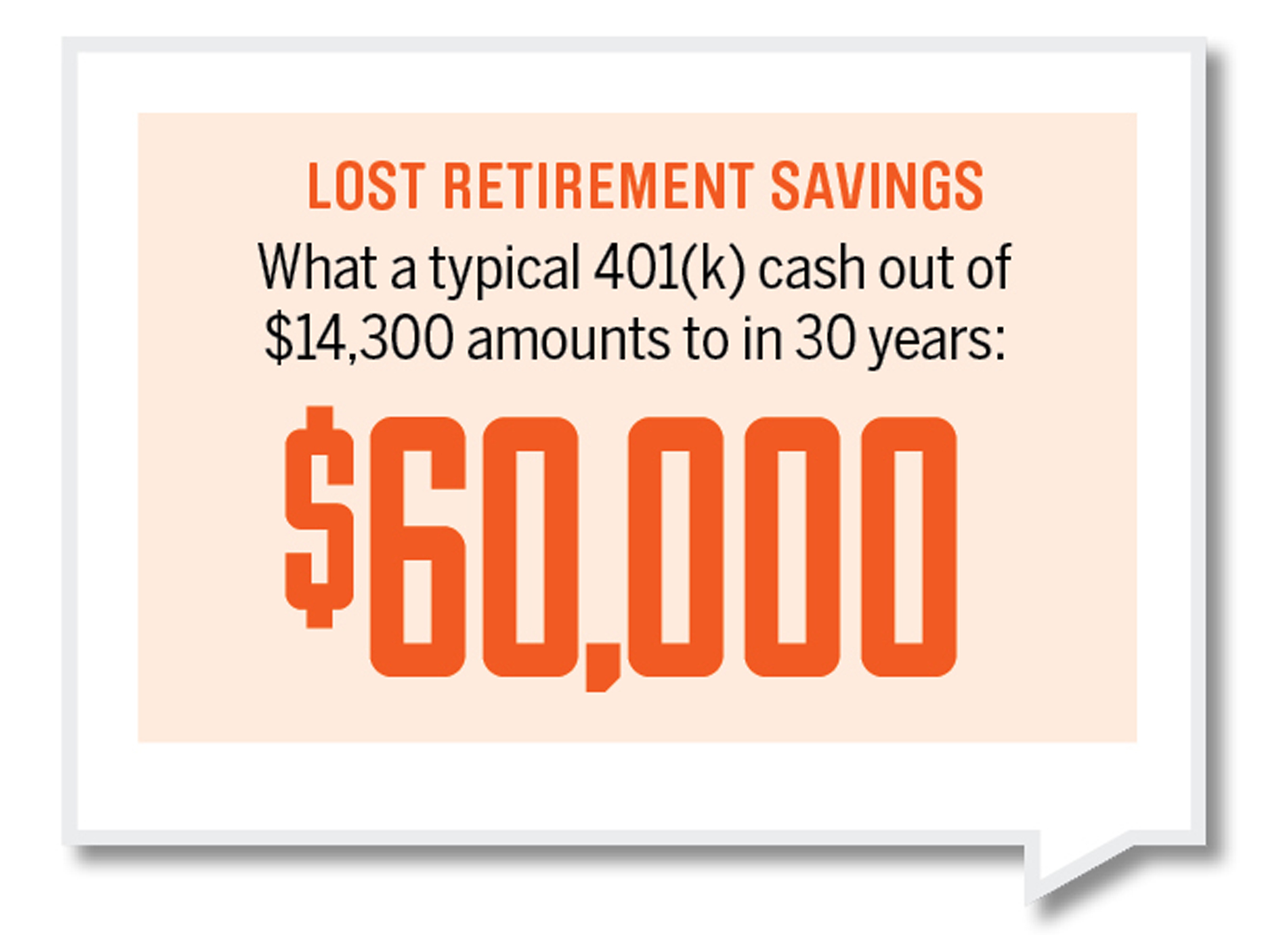

Roll over as you go. Twentysomethings typically spend 1.3 years at each job. And Fidelity says nearly half cash out 401(k)s when leaving. That triggers income taxes and a 10% penalty, depleting the amount that can compound. The box shows what that really costs you.

Gen Xers

Keep the bottom line top of mind. A funny thing about investing: The more you save and the bigger your balance, the more fees you have to pay in dollar terms. So now that your account has some serious money, shifting to lower-cost options such as an index fund is an easy way to save big (see chart). If you have $100,000 saved by 40 and underlying returns average 7%, the savings by 65 of switching from a 1.2%-fee fund to 0.3% is $102,000—nearly a whole second nest egg.

Shoot for 17%. How much you need to save depends on how much you already have. But 17% is a good mental anchor. That’s the number Wade Pfau of the American College of Financial Services came up with for folks starting from scratch at 35, with a 60% stock/40% bond portfolio, to safely fund a typical retirement goal. You might be okay saving less if the markets go your way, but Pfau’s number is what it takes to get there even with poor returns. That’s far more than the average 401(k) contribution of around 6% to 7%. But take a deep breath. That number includes the contributions from your employer.

Resist the urge to borrow. About 22% of participants between 35 and 54 in plans run by Vanguard have borrowed from their retirement accounts. Compared with other forms of debt, a 401(k) loan isn’t the worst. But the amount that you borrow is money that’s not compounding tax-deferred.

Baby Boomers

Save in bursts. Neither saving nor spending runs along a smooth path. For example, you may have to pare back savings while paying the kids’ college bills. The good news is that “after 50 is when people should be able to save the most, as their kids are moving out, they’ve paid off the mortgage, and they should be in the highest earnings years of their lives,” says economist Wade Pfau. Starting at 50, you can also make extra 401(k) contributions of up to $5,500, on top of the normal $17,500.

Prep for the spend-down phase. Once you retire, you’ll have to spend out of your nest egg regardless of market conditions. Even if stocks do well on average, a bad run early on can deplete your portfolio. So “start taking a couple percent of equities off the table every year in the five or 10 years leading up to retirement,” says financial adviser Michael Kitces.

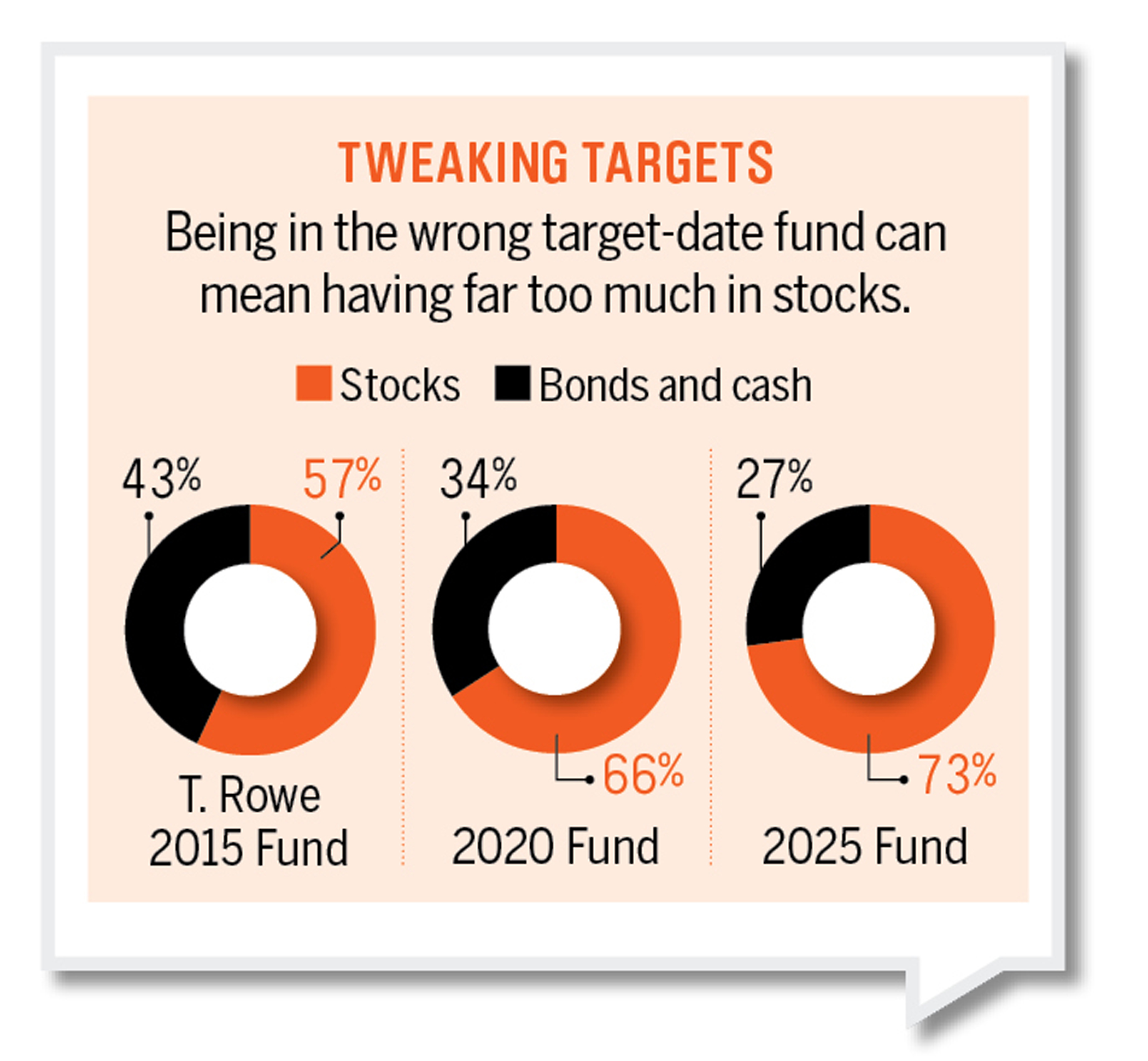

Readjust your target. According to polls, Americans expect to retire around 66. But the actual age of retirement is 62. Things happen: You may run into health issues or be forced into early retirement. Now many 401(k) savers use target-date funds. As you gain more visibility on your own retirement date, adjust the target-date fund you use. As the chart shows, it can make a big difference. Notes: Cash-out growth assumes a 5% annual return. Fee calculations are based on total costs, including forgone gains. sources: Morningstar, T. Rowe Price, SEC, Money research