The Three 401(k) Moves Millennials Should Make Now

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

For the so-called Millennial generation, born after 1981 (yes, that includes you, 30-year-olds!), retirement might seem far off.

But if you're lucky enough to have a job with an employer-sponsored 401(k), you ought to take advantage right now. Assuming you—like many of your peers—feel too perplexed by your options (or too busy multi-tasking) to put in much effort, here are the best bare-minimum moves:

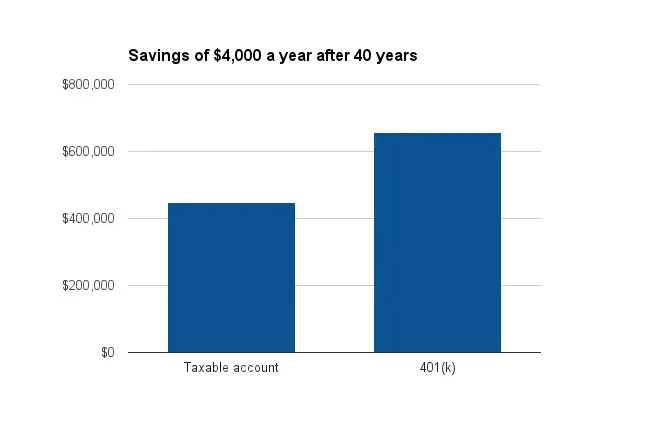

1. Contribute even if you don't get a match. Although the vast majority of large employers offer some matching 401(k) contributions, smaller companies don't always do the same. But your account is still worthwhile. A 401(k) lets you set aside a chunk of your paycheck before it gets taxed and shields that cash from Uncle Sam as it grows. Yes, you'll pay income tax on the money you take out when you retire. But because you got to stash more to begin with—and that money will have had many years to build—you'll do better than you would have in a taxable (e.g., savings or brokerage) account.

For example, imagine you put away $4,000 annually starting at age 25. Here's how much more you'd have saved by 65 if you kept that money in a 401(k) instead of an unsheltered account:

In addition to being hit with income taxes, money in a non-retirement account is subject to taxes on earnings—whether from dividends, capital gains, or just simple interest. Not so with a 401(k). And therein lies another big advantage. "The less money coming out because of taxes, the more available for compounding, which is the real wind at your back," says Brooks Herman, head of data and research at BrightScope, which rates 401(k) plans.

If you're fortunate enough to get a match, maximize it. Say your employer matches up to 6% of contributions (the most common match), but you save only 3% of your salary each year? You're leaving free money on the table.

2. Take the cheap and lazy option. If you feel clueless about the funds offered in your 401(k) plan, you're not alone: A TIAA-CREF survey recently found that more than 40% of millennials who participate in retirement plans are not familiar with their investment options.

Assuming you'd like to do as little work as possible, go with a target-date fund. These funds—which automatically adjust your relative holdings in bonds and stocks (your "asset allocation") to be less risky as you get older—are particularly attractive if they charge less than 0.5% in annual fees, or $5 for every $1,000 invested.

3. Don't touch that money, unless you need it for a medical emergency. Millennials have it tough, financially, with higher debt and unemployment (and lower income) than Gen Xers and Boomers had when they were young, according to a recent Pew study. So it might be tempting to view your retirement account as a good rainy-day fund. But money in a 401(k) is meant for retirement, and if you try to pull it out early (before you are 59 ½) you will have to pay an extra 10% tax on top of standard income tax. That penalty could wipe out all the benefits of the account, and then some. The only real exception to the penalty is if you are using the money because you've been disabled, or for certain qualified medical expenses. Likewise, borrowing against your 401(k) should be only a last resort.

If there's a serious chance you'll need to use your savings for future educational expenses or for buying your first home, an individual retirement account (IRA) not sponsored by your employer might be a better vehicle for your cash, because those come with slightly more flexible rules for early withdrawals. But in general, retirement accounts—whether 401(k)s or IRAs—should be left untouched until you actually retire.