Everything Investors Got Wrong About the Trump Presidency, Explained

- Here's Why 2015 Will Be a Good Year for Stocks

- For the Fed, There's Only One Excuse Left to Keep Rates Low

- What Airline Stocks Tell Us About the Rest of the Market

- It's a Huge Day for the Stock Market. What You Need to Know About History's Longest Bull Market

- The Best Performing Stock of This Bull Market Is Up Almost 39,000% — and You've Probably Never Heard of It

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Ever since President Trump came into office, investors thought they had the script figured out. The promise of deregulation, tax cuts, and fiscal stimulus would push the economy's pedal to the metal, while Trump's tough populist talk—and threats of new tariffs—would steer focus back onto U.S. stocks.

The bottom line: Wall Street would shift into a higher gear. And to some extent it has. But the "Trump Bump" hasn't played out anywhere near the way investors envisioned.

Sure, anticipation of a reinflating economy "rekindled the animal spirits," says Christopher Marangi of the Gabelli Funds. But that enthusiasm has morphed into anxiety lately, turning the Trump Bump into a bumpy ride.

And sure, the economy looks as if it's heating up. But one key indicator of future growth—the spread in bond yields—is throwing some cold water on this assumption. Even the Point Bridge GOP Stock Tracker ETF (ticker: MAGA)—known as the "Make America Great Again" fund because it invests in firms whose political action committees and employees support the GOP and Trump—is lagging the market this year.

It just goes to show that Wall Street "probably attributes too much to this one person and administration," says Jason Brady, CEO of Thornburg Investment Management. And it illustrates that many assumptions investors made about Trump's impact on the stock market were wrong.

Here are five of the biggest investor misconceptions about the Trump Bump—and how you can tack your portfolio back to reflect what's really going on:

America First?

❌ Misconception No. 1

Trump's "America first" policies were supposed to turbocharge the domestic economy, making U.S. stocks great again.

✅ What really happened

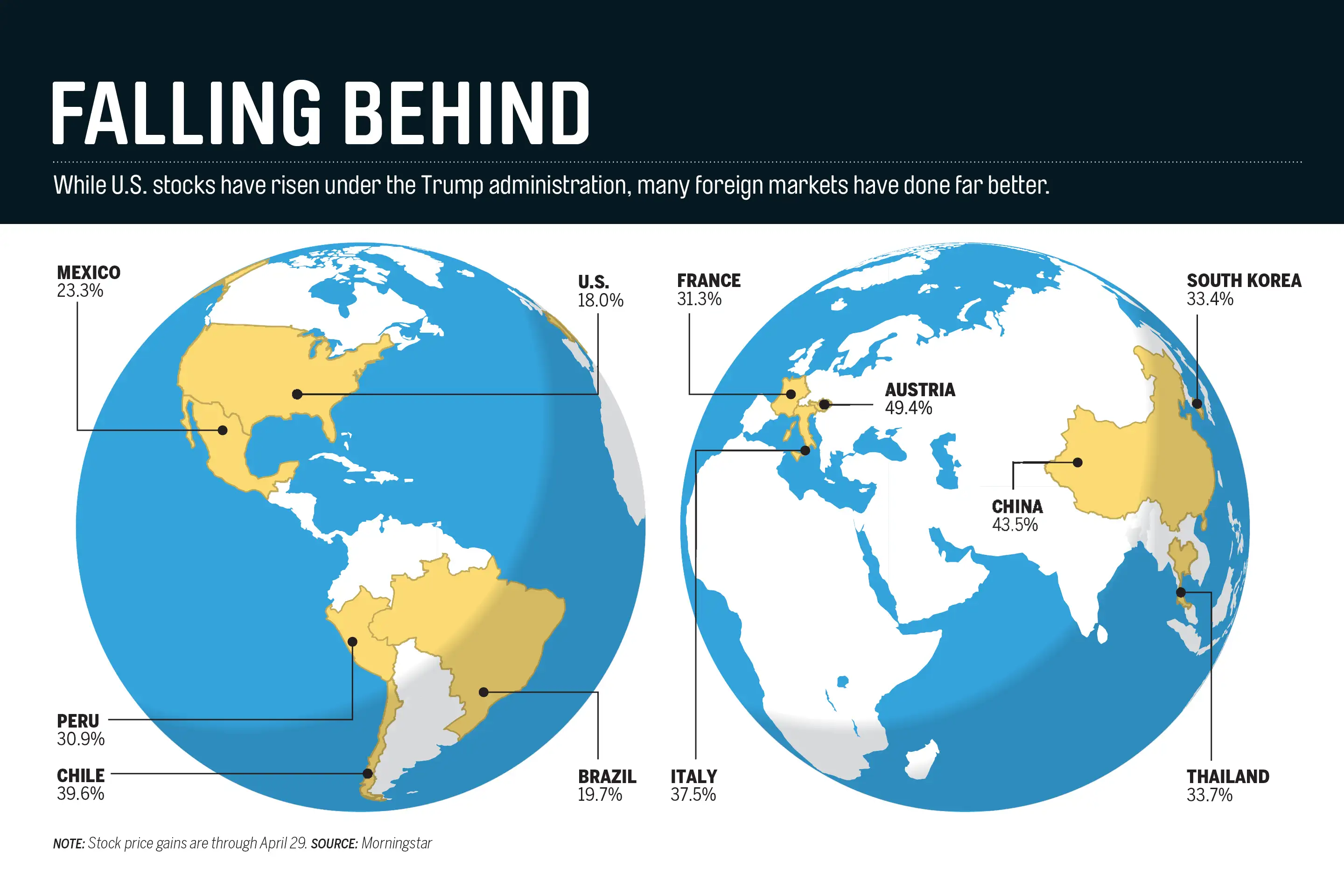

Shares of U.S. companies are up, but they are actually laggards when compared with foreign equities.

Since Trump took office in January 2017, the S&P 500 index of U.S. stocks has raced ahead 18%. But if you look around the world, you'll find plenty of foreign markets that have lapped American equities during Trump's tenure in office.

Austrian stocks, for instance, are up 49% in the Trump era. Chinese equities have advanced 44%. And Italian shares are up 38% under Trump and 12% this year. (By comparison, U.S. stocks have been flat so far in 2018.)

The reason? While the U.S. economy has grown an average of 2.5% in the first five quarters of the Trump administration—which is faster than the pace of growth in 2016—gross domestic product is still expanding at a slower rate than it did for much of 2015.

What's more, even if you're convinced that Trump's policies will eventually turbocharge the U.S. economy going forward, there's no evidence that faster GDP growth produces better stock results.

Nearly a decade ago, finance professor Elroy Dimson and colleagues at the London Business School discovered something counterintuitive: Stocks in the slowest-growing economies of the world have historically outpaced the gains of companies in the fastest-growing regions—based on more than a century of economic and market data.

More recently, a study by Vanguard found that trends in GDP growth have about as much predictive power over the future performance of equities as does the level of rainfall—which is to say, there is no correlation whatsoever.

Instead, the best determinant of future stock performance over the coming decade is how frothy stocks are, Vanguard researchers found.

And U.S. equities are historically expensive at the same time that many foreign markets are not—and there's nothing that a President can do to change that.

The price/earnings ratio for U.S. equities (based on 10 years of averaged earnings) is more than 31, which is about twice the historical average. By comparison, foreign shares are trading at a P/E ratio of 17, while foreign stocks based in emerging economies like China are trading at a P/E of just 15.

👍🏽 What you can do

Success in investing requires counterintuitive thinking. And as strange as it sounds, you have to be willing to think more globally than ever in the era of Trump.

That's what financial planner Lewis Altfest is doing. "We have more money abroad than we normally would. Where we would normally have 25% abroad, we now have 40% of our money outside the U.S.," says Altfest, president of Altfest Personal Wealth Management.

Forty percent is a key weighting. Research by Vanguard found that the full diversification benefit of owning foreign shares kicks in only when investors hold 30% to 40% of their equity portfolio overseas.

Another reason to look overseas: Based on the historical relationship between valuations and future stock gains, foreign equities in the developed economies of Europe and Japan are expected to return nearly 7% annually over the next decade, while emerging-market shares are likely to return 8% annually, according to Research Affiliates. By contrast, U.S. stocks may gain only 2.4% annually for the next decade.

The Strong Dollar?

❌ Misconception No. 2

The reinflating economy would push interest rates higher, boosting optimism and investments in the U.S.—and strengthening the dollar.

✅ What really happened

The U.S. dollar has been sinking for much of the Trump presidency, making it harder for some U.S. companies to compete abroad.

Now, in the days immediately following the November 2016 election, the buck did begin to creep higher—a development that President Trump told the Wall Street Journal was partially "my fault because people have confidence in me."

There is some truth to what he was saying. Sometimes trading in a country's currency reflects the global market's confidence in the health of that economy.

Yet since President Trump actually took office in January 2017, the dollar has lost more than 10% of its value against a trade-weighted basket of foreign currencies.

Curiously, this took place at a time when interest rates have been rising in America. Normally, rising rates in the U.S. entice global investors to park more of their cash in dollars, which boosts the currency's value.

Does this mean the world has lost confidence in the dealmaker-in-chief? Nope.

There's a perfectly good explanation for why the buck has weakened. The Federal Reserve Board has been raising rates gradually to combat inflation, notes James Paulsen, chief investment strategist for the Leuthold Group. And "inflation is what destroys the value of the U.S. dollar," he says.

👍🏽 What you can do

Start by diversifying your portfolio using "real assets" like oil and other commodities to supplement your equity holdings. If the dollar is indeed falling because the U.S. economy is reinflating, then history says this is a good time to add some commodities to your portfolio, as they perform well in inflationary times, says Paulsen.

An easy way to gain exposure to real assets is through a fund like iShares North American Natural Resources ETF (IGE), which is on our Money 50 list of recommended exchange-traded funds. More than 90% of this fund is exposed to energy and basic materials.

Another way for Americans to take advantage of a weakening dollar is by investing in funds that hold international stocks. When you—or the funds you own—buy foreign shares, you aren't just buying overseas equities, you're also purchasing the foreign currency that the stock is denominated in to make that trade.

That means if the dollar were to weaken while you hold that investment, you could see gains simply because the foreign currency you used to buy those equities appreciated against the dollar.

There is a wrinkle, however, says Jack Ablin, chief investment officer for Cresset Wealth Advisors. When the dollar weakens, it also makes it harder for foreign companies to compete against U.S. firms in the global marketplace, since the falling dollar reduces the prices that American companies can charge.

Ablin says a simple way around this is to focus on shares of foreign businesses that derive most of their sales in their home regions. You can do that by concentrating on small- to medium-size foreign companies, which are more apt to be locally focused than giant multinational firms.

You can find those types of stocks in the Vanguard FTSE All-World ex-U.S. Small-Cap Index Fund (VFSVX), which is also on the Money 50 and focuses on small- and midsize stocks in the developed and emerging markets.

Multinationals Take a Back Seat?

❌ Misconception No. 3

Large multinational corporations were supposed to be big losers under Trump's populist trade policies, which were expected to make it harder for "elites" to move products and jobs across borders.

✅ What really happened

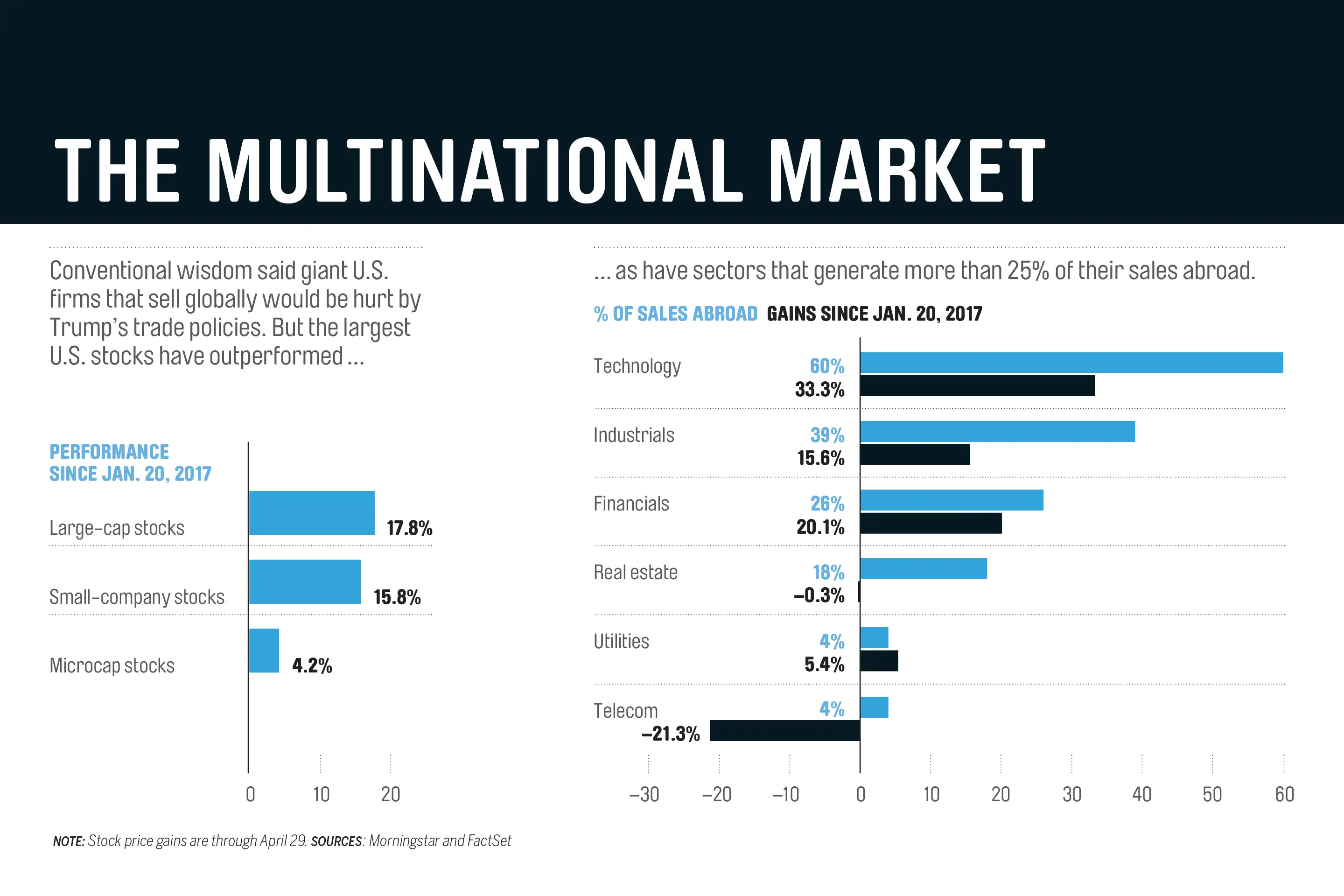

The multinationals are all right. In fact, giant companies that sell globally are likely to keep being big winners, regardless of Trump's threat of a trade war.

Throughout the 2016 campaign, candidate Trump used social and traditional media to take a verbal hammer to global titans like Ford, Boeing, and Goldman Sachs.

But in the era of Trump, large stocks have actually outpaced small-company shares, even though small stocks tend to outperform over time. Multinationals "seem rather happy right now," says Terri Spath, chief investment officer for Sierra Investment Management.

Why? There are a bunch of reasons. For starters, tariffs or no tariffs, the weak dollar under Trump has helped U.S. multinationals sell their products and services abroad, boosting revenues and earnings, Spath says.

Consider this fact: The three sectors that generate the biggest percentage of sales abroad are technology, energy, and basic materials. This year, all three sectors are on track for the fastest revenue growth in the S&P 500.

Okay, but isn't a trade war—not just with China, but also with our biggest trading partners in Europe and North America—a real threat?

Absolutely. But remember that multinationals are also better positioned than smaller businesses to deal with the fallout of a trade war. "They're the ones with a global supply chain. They're better able to adapt" to rising production costs since they can switch where they source their materials, says Adam Abelson, chief investment officer at Stralem & Company.

There's also the fact that tough talk on trade wasn't the only thing the Trump administration promised. "Probably the most significant and arguably least-covered substance of the Trump administration has been deregulation," says Chris Brightman, chief investment officer for Research Affiliates. "Trump and his appointees have been very busy deregulating, and that's been wonderful for large corporations." After all, unlike small businesses, the biggest companies in America have armies of lobbyists who can advocate for specific regulatory relief that benefits them, he says.

👍🏽 What you can do

At the start of the Trump administration, conventional wisdom said investors should think small, as shares of small- and midsize U.S. companies are likely to derive the bulk of their sales domestically— allowing them to avoid much of the fallout from a potential trade war with China and Europe.

But if large U.S. multinational corporations are disproportionately benefiting from other Trump policies, then you may want to think big. Really big.

For instance, the average stock in the Vanguard Mega Cap Value Index ETF (MGV) has a market value of more than $126 billion, 30% larger than the typical company in the S&P 500 blue-chip stock index. The fund's top holdings include big financial, tech, health, and energy names that are global in nature, led by Microsoft, JPMorgan Chase, Johnson & Johnson, and Exxon Mobil.

With this strategy, Vanguard Mega Cap Value has outperformed more than 85% of its peers over the past three and five years, according to Morningstar. Even better, the average holding in this fund sports a low P/E ratio of 14.5 (based on projected profits), roughly 15% cheaper than the stocks in the S&P 500 and the Russell 2000 small-stock index.

The Infrastructure President?

❌ Misconception No. 4

Trump was supposed to be the infrastructure President, proposing to boost spending on the nation's crumbling roads, bridges, and tunnels by $1.5 trillion. This was expected to hurt the fortunes of municipal bonds used to finance many of these projects, as an infrastructure boom could flood the bond market with new muni debt supply, driving down prices.

✅ What really happened

Despite the fact that infrastructure was one of the few Trump initiatives that had some real bipartisan support in Washington, this initiative has gone nowhere.

To date, Congress has allocated only around $21 billion for infrastructure spending, a tiny fraction of what the administration has called for. Meanwhile, the White House has been busy pushing its other policy priorities, including tax cuts, deregulation, and trade deals.

Some of this is to be expected, says the Gabelli Funds' Marangi. "Infrastructure is a particularly difficult issue. There isn't a national funding mechanism for the type of infrastructure spending that needs to be made," he says. Instead, any effort to rebuild crumbling roads and bridges must be taken up on a state-by-state and, in many cases, city-by-city basis.

Meanwhile, there aren't that many shovel-ready projects. Sites still have to be debated with public comment; environmental issues have to be assessed; and traffic has to be studied—all before an official vote can be taken to move forward. In many cases, "this is a 10-year framework," Marangi says.

👍🏽 What you can do

Now that the difficulties of trying to boost infrastructure spending are understood, it's time for investors to give muni bonds another look.

Tax-advantaged municipal bonds issued by states and municipalities have had a rough year. Over the past 12 months, muni bonds have returned a little more than 1% after taking a couple of hits. First, fears of oversupply in an infrastructure boom scared off some investors.

Then Congress passed the Tax Cuts and Jobs Act of 2017, which lowered income tax brackets. "When you're talking about a tax-advantaged investment, any lowering of taxes is bound to make it less attractive than before. And it has to be repriced," says Mark Freeman, chief investment officer at Westwood Holdings Group.

But Freeman says that this repricing has already taken place and now "munis are more attractive relative to the rest of the market." At the same time, fears about a flood of new munis hitting the market have dissipated, giving investors reason for hope.

His advice: Focus on shorter-term muni bonds, which he says have repriced the most.

Financial planner Altfest agrees. With interest rates rising, Altfest says it's safer to buy short-term debt that will come due sooner, so you can reinvest it at higher rates quickly. On our Money 50 recommended list, you can turn to Vanguard Limited-Term Tax-Exempt Bond Fund (VMLTX), a short-term muni fund whose holdings have an average maturity of around three years.

The Real Estate President?

❌ Misconception No. 5

As a real estate mogul who, during the 2016 election, kept warning investors that the stock market was in a bubble that was about to burst, Trump was expected to be a champion of property ownership, and not Wall Street's cheerleader.

✅ What really happened

It turns out that Trump can't defy the laws of supply and demand—nor can he control interest rates. As a result, real estate is likely to continue to be a laggard under this administration.

Since President Trump took office, real estate has been the one sector of the economy that hasn't enjoyed a Trump Bump. Since Jan. 20, 2017, real estate investments have been largely flat while the S&P 500 has risen 18%. Why?

Part of it is tied to the reinflating economy. As the economy has picked up, investors have been selling slow-growing bonds to buy faster-growing stocks. And as bond prices have fallen, yields have risen. The result: The average 30-year fixed-rate mortgage has gone from 4.09% when Trump was sworn in to 4.58%, according to Freddie Mac.

Meanwhile, there are supply issues throughout real estate. With single-family homes, the dearth of supply amid decent demand has sent prices higher. "Some people are choosing not to sell," says Spath. "Interest rates are going up, so that's slowing the velocity in new demand." In commercial real estate, it's the opposite problem: "There's lots of concerns of oversupply" in properties ranging from storage facilities to multifamily buildings, says Freeman.

👍🏽 What you can do

Don't force the issue. If you own a home, you probably have plenty of exposure to real estate to begin with. There's no need to bolster that with your investable portfolio. What's more, if you own an S&P 500 index fund, about 3% of that is in real estate too. So relax.