How Not to Get Blindsided by Costs in Retirement

You don't have to be a psychic to forecast much of your spending in retirement. Your housing, your utilities, your dinners out—the monthly costs for these will rarely surprise you.

Not everything, though, can be budgeted so easily. You can safely assume, for example, that you'll have health care expenses—Fidelity estimates they will average $245,000 for a couple in retirement—but you can't know ahead of time when those bills will pop up or what each will amount to. You're planning to attend your grandchildren's weddings, but you don't know yet whether the nuptials will take place across town or in another hemisphere.

About 40% of retirees, in fact, say their retirement expenses are higher than they had expected, according to the Employee Benefit Research Institute. But with a little planning, you can minimize the financial shock of unpredictable expenses, either by setting aside money to address them or by taking other steps to keep them under control. To reduce your chances of getting blindsided, follow these tips.

Maximize your coverage

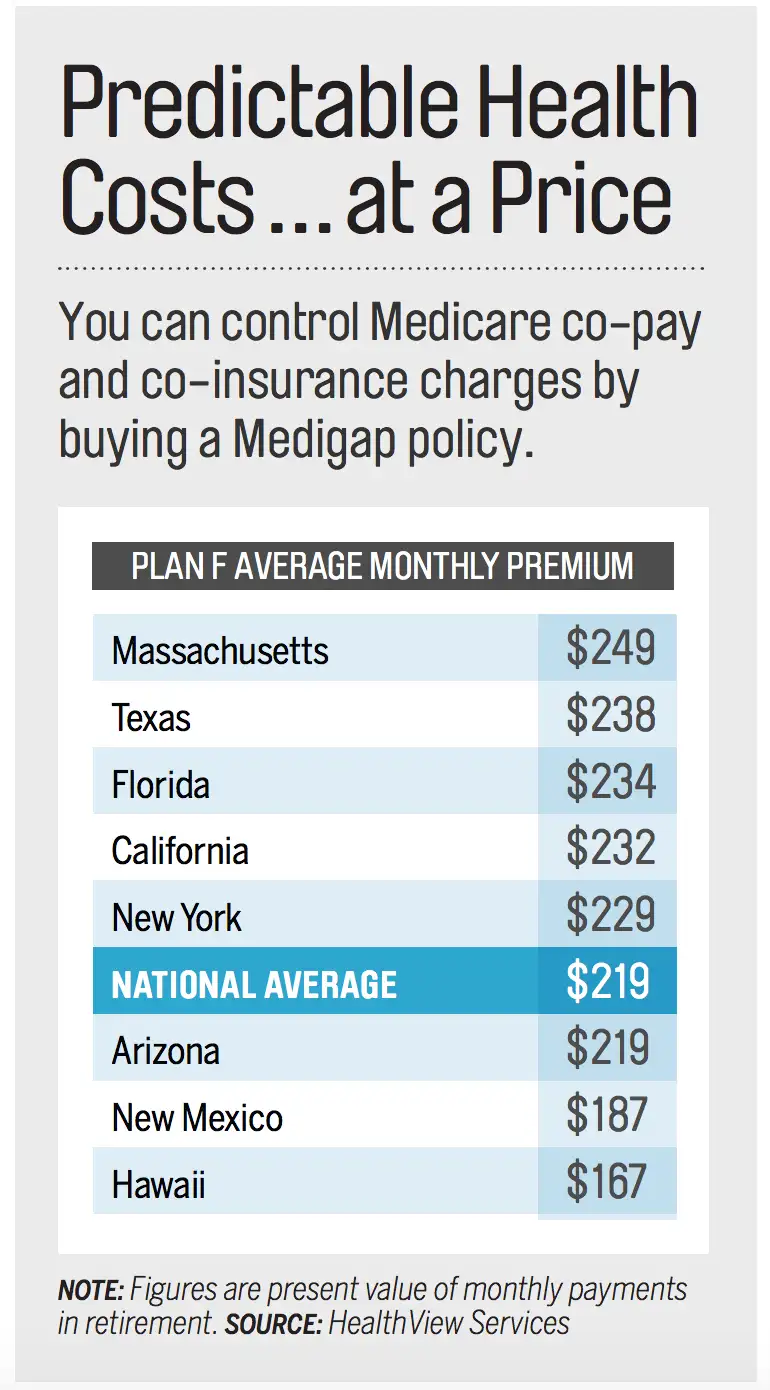

Health care expenses are one of the biggest wild cards in retirement. Original Medicare (Parts A and B) covers only about 20% of a beneficiary's total costs, according to HealthView Services, which provides retirement health care cost data and planning tools to the financial industry.

Supplemental insurance, including Medicare Part D drug coverage and Medigap—private plans covering costs not borne by Medicare—brings some certainty to your budget. While increasing fixed costs, these plans can minimize the financial injury of a heart attack or broken hip by covering all or part of your out-of-pocket costs.

Those costs can be considerable. After meeting the deductible, patients typically have to pay 20% of Medicare-approved fees for most medical services—an amount that isn't capped. Plan F, the most comprehensive Medigap plan, covers Part A and Part B co-insurance and deductibles, along with other services. The monthly premium varies by region (see the table).

Calculator: How will retirement impact my living expenses?

If you're under 65, you can limit surprises by buying a platinum health plan on the individual market, designed to cover 90% of medical costs, vs. 70% for a silver plan. Based on data from HealthPocket, an unsubsidized platinum plan would run the average 60-year-old $14,000 this year in premiums and a deductible, or $2,000 more than those costs in a silver plan.

Pad your savings

Even with insurance, you'll have to bridge other health care gaps in retirement. "The likelihood you'll need surgery or a drug not covered [by insurance] is considerable," says Richard W. Paul, a certified financial planner in Novi, Mich. Moreover, dental work, hearing aids, and vision care aren't usually covered. Paul advises having an emergency fund of 12 to 18 months of living expenses, up from the six months commonly suggested for people who are employed.

You can also ballpark those extra medical costs and save accordingly. Hearing aids average $4,000 to $5,000 a pair and need replacing every few years, says Jacksonville physician and financial planner Carolyn McClanahan. As for dentistry, full crowns can cost up to $1,500, and a single implant can run more than $4,000, according to the American Dental Association's Health Policy Institute. If you set aside money for expenses like those, you're less likely to have to tap your emergency fund or investments at short notice.

An ideal place to save, if you're still working and have a high-deductible health plan, is your health savings account. You can put pretax money into your HSA (up to $6,750 this year for families and $3,350 for individuals, with an extra $1,000 if you're 55 or older). Then you can let it grow to fund medical expenses tax-free in retirement.

Get serious about family fun

What if you have your bucket-list trips all mapped out, then your granddaughter invites you to her destination wedding in Belize?

Plan ahead by building a happy-family fund into your retirement savings. Count up the grandkids and start banking a few thousand apiece to cover graduations, weddings, and other festivities. And tap your hobbies for extra cash, says Rand Spero, a financial planner in Lexington, Mass. One of his clients, a former engineer, makes extra money training dogs.

You might even sell off a family heirloom. "What's a better legacy?" Spero asks. "Spending time with family or handing someone an old watch?"