What Is a Roth IRA Account

A Roth IRA is an individual retirement account where the money you deposit is taxed upfront. Since you're funding your account with after-tax money, your investments grow tax-free. You can also withdraw contributions from your Roth IRA at any point, but you may have to pay taxes and penalties for early withdrawal of your earnings.

What You Should Know:

- You can have a Roth IRA account regardless of your age.

- Roth IRAs are recommended for people who are in a lower federal tax bracket or below 25%.

- You can withdraw your contributions to a Roth IRA penalty-free at any time for any reason but may be penalized for withdrawing earnings before the age of 59 ½.

While Roth IRAs seem like a great investment for younger people, their tax benefits are a great choice for people of all ages. If you're in a lower tax bracket now and anticipate having higher taxes upon retirement, a Roth IRA could be worth considering.

Roth IRAs offer tax benefits that appeal to people of all ages. They may be an especially good fit for you if you think you're in a lower tax bracket now than you will be when you retire. Unlike Traditional IRAs, you pay taxes on Roth IRA contributions upfront, so you keep what you've made in the account when retirement arrives.

However, Traditional IRAs may be a better option for higher earners. Top earners are generally in a higher tax bracket before they retire, which means it makes more sense for you to pay taxes on contributions when retirement arrives. Additionally, depending on your filing status and income, some people may be restricted from contributing to a Roth IRA altogether.

According to Alicia Munnell, professor of Management Sciences at Boston College’s Carroll School of Management and Director of the Center for Retirement Research, deciding on a Roth IRA is just a question of people’s perception of relative tax rates in the future and their individual circumstances.

Experts predict Congress will have to increase tax rates in the future because of the country’s growing debt burden. This is better known as an overall tax rate. Your individual tax rate will depend on your filer status, income, and the combination of your effective tax rate (taxes due based on tax statements) and marginal tax rate (tax rate paid on net income). Munnell refers to this as relative tax rates because they vary from person to person.

“We're going to have higher tax rates in the future than what we have today, so you would be smarter to pay taxes now rather than having to pay higher taxes when you retire,” said Munnell.

How Roth IRA accounts work

Roth IRA accounts have unique features like tax-free growth and no mandatory withdrawals. This makes them an excellent fit for savers who want a flexible retirement account. Even so, the account isn't without its drawbacks. Before deciding whether a Roth IRA is the right fit for you, familiarize yourself with its pros and cons in the table below.

Pros and Cons of Roth IRA Accounts

- No restrictions to contribution age

- Qualified tax-free withdrawals

- No income taxes for inherited Roth IRAs

- Earnings grow tax-free

- No mandatory withdrawals (unlike a Traditional IRA)

- No upfront tax break

- Annual contribution limits are about a third of 401(k)s

- Reduced or limited contribution amounts

Roth IRA vs. Traditional IRA

Roth IRAs have one main advantage over traditional IRAs: since your investments are made with after-tax dollars, once you reach retirement you’ll get every penny of your savings tax-free.

“When you look at your pile, that whole pile is yours,” said Munnell, referring to Roth IRA funds. “When those of us who have traditionally been saving to traditional 401(k) plans look at our retirement savings, we can say, I know that maybe 80% of that pile is mine, but 20% belongs to the government.”

Here’s a breakdown of their differences:

| Traditional IRA vs. Roth IRA |

| Traditional IRA | Roth IRA |

| Contributions to Traditional IRAs are made with before-tax dollars, meaning that you delay paying taxes until retirement. | Contributions to Roth IRAs are made with after-tax dollars, meaning you’ll pay taxes now rather than when you retire. |

| Investments will grow tax-free. |

| No adjusted gross income limits to participate. | Must meet adjusted gross income limits to participate. |

| Contributions limited to $6,000, plus an additional $1,000 if you’re age 50 or over. |

| You can deduct contributions if you qualify. | Your contributions aren’t deductible. |

| Withdrawals of contributions and earnings are subject to federal and most state income taxes. If you’re under age 59 ½ you may have to pay an extra 10% tax for early withdrawals, unless you qualify for an exception. | Withdrawals are a bit more flexible. You can withdraw contributions penalty and tax-free at any point. However, if you withdraw investment earnings before the age of 59 ½, you may be subject to tax and penalty charges — unless it’s for a qualifying reason. |

| You are required to withdraw money by April 1 of the year after you reach age 72. | If you’re the owner of the Roth IRA, there’s no age limit to start withdrawing money. However, if you’re a beneficiary of the Roth IRA, you may have to take distributions. |

| You can contribute to your traditional IRA after age 70 ½ provided you have earned taxable compensation. | You can continue contributing funds to your Roth IRA at any age. |

| Source: Internal Revenue Service |

Who Can Open a Roth IRA?

To be eligible to open a Roth IRA, you must have earned income. The Internal Revenue Service defines taxable income and wages as money earned from a W-2 job or self-employment such as childcare providers or babysitting.

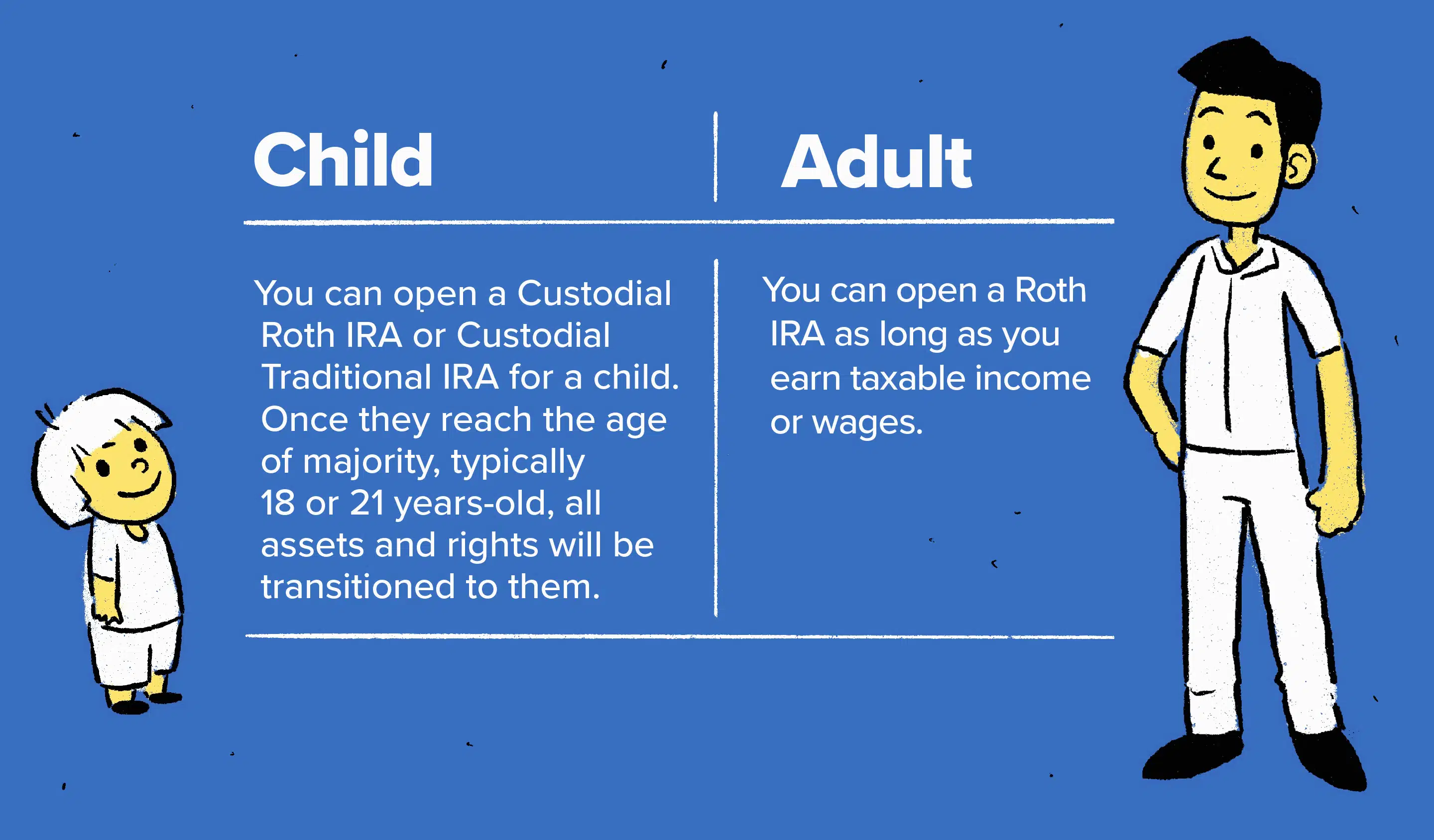

One of the great things about Roth IRAs is there’s no age limit on account owners. In other words, if your child did some babysitting throughout the year and earned $500, they can contribute that entire amount to a Roth IRA under their name. However, if the child is younger than 18 (or older, depending on the state) the parent/guardian has to open up the account as a custodian.

You can open a Custodial Roth IRA or Custodial Traditional IRA for a child, and once he or she reaches the age of majority, typically 18 or 21 years old, all assets and rights will be transitioned to them.

If you’re interested in opening a Roth IRA for yourself or a dependent, you can follow these step-by-step instructions to do so.

1. Determine if you meet the eligibility requirements

Roth IRAs offer unique tax advantages to account holders. However, the IRS will only let you take advantage of those benefits if your modified adjusted gross income (MAGI) is within certain thresholds.

The MAGI threshold varies by year. For the 2023 tax year, you can contribute the maximum possible amount to a Roth IRA if you make under $138,000 annually as a single person or under $218,000 as married taxpayers.

If you’re below these thresholds, you meet the income eligibility requirements. If you’re above them, you may still be able to contribute some amount to a Roth IRA, but your maximum contribution will scale down as your earnings go up.

2. Decide where to open your Roth IRA

Once you’ve determined that you meet the income requirements to use this investment strategy, your next step is figuring out where to open the investment account. Most financial institutions offer Roth IRAs for wealth management. The easiest option may simply be to open one of these types of accounts at your current bank to make it easy to transfer funds into the account.

One thing you should know about tax-deferred accounts like Roth IRAs is that they’re highly regulated by the federal government. This means there are rarely meaningful differences between Roth IRAs offered by different banks.

The most important step is ensuring your preferred bank is FDIC-compliant before setting up a Roth IRA conversion. Otherwise, your funds could be at risk if the bank fails. Similarly, check that your brokerage firm is insured by the Securities Investor Protection Corporation (SIPC).

3. Gather the necessary information

Now you’re ready to start gathering the information you need to set up your Roth IRA. Here’s some information your bank will likely ask for when you open an account:

- A driver’s license or an equivalent form of identification

- Social Security number

- Employment information

- Name, address and Social Security number of beneficiaries

- Your bank’s routing number and checking or savings accounts

4. Choose your investments

Your Roth IRA isn’t just for saving money. It also doubles as a brokerage account you can use to make investments that earn tax-deferred income for you. It’s also a smart idea to consult with a financial advisor while coming up with an investment strategy. But you will be free to invest in many different types of assets, including:

- Mutual funds

- ETFs

- Individual equities

- Bonds

- CDs

- Real estate

When coming up with an investment strategy, it's essential to consider your age and whether you have any big-ticket expenses coming up, such as a home purchase, that could impact your ideal investment options. Speaking with a financial and tax advisor will help you make the best decision for your scenario.

5. Make your contributions

Now you’re ready to begin making consistent contributions to your Roth IRA. You can do this in whatever ways you want as long as you stay within your maximum contribution limits.

For example, you could put your maximum yearly contribution in a Roth IRA immediately once you have the funds to do so. Alternatively, you might want to wait and spread out your contributions equally every month. The best method is the one that fits your financial situation.

6. Keep track of your contributions and earnings

All that’s left to do at this point is to keep an eye on your contributions and earnings over time to ensure you comply with all rules related to your Roth IRA. It will also be important to check in on any investments that you’ve made through the account periodically – especially as you grow older and your investment strategy may change.

How to choose the best investment options for your Roth IRA

Opening a Roth IRA account is a relatively straightforward process. But selecting how you want to invest those funds can be a challenge. Here are a few tips you may want to consider as you go about doing so.

Determine your investment goals

It’s best to start with an analysis of what you hope to get out of your investments. For example, do you want to start building an emergency fund? Or are you hoping to secure your retirement? The answer could impact your strategies and the types of assets you want to invest in.

You may also be interested in funding a particular life goal, such as a dream vacation or the purchase of a new car. Understanding what you hope to achieve through investment is the first step in determining the best assets to hold your money in.

Assess your risk tolerance

Another aspect of understanding your investment goals is knowing how much risk you’re willing to assume. The standard advice is that younger investors can afford to assume more risk because they have more time to re-earn any losses. Older investors may need to build a safer portfolio to avoid the potential for significant downside.

If you want your capital to grow at the fastest rates possible, you may want to look at assets with more upside, such as growth stocks. But the stocks with the highest upside often have higher risk as well, so you may need to take a more active role in managing these investments.

Or, maybe you're looking for stable, long-term growth out of your Roth IRA. In that case, you may want to consider holding stocks from more established companies, bonds, CDs and index funds that bundle multiple assets together.

Choose your asset allocation

It often makes sense to invest in multiple asset classes from a single retirement account. For example, in your Roth IRA, you may wish to hold ETFs for several industries, a few individual stocks and even some bonds or CDs. Holding multiple types of assets diversifies your portfolio to provide both low- and high-risk options while also mitigating any losses one sector may experience.

Once you know the types of assets you want to hold, you can start thinking about allocations. For example, the full value of your Roth IRA portfolio is 100%. You may want to put 20% in an ETF, 50% in a mutual fund and spread the rest out across a few stocks you like.

These percentages are not indicative of what an ideal asset allocation looks like. The exact combination is up to you, but diversifying in this way is an excellent way to reap the benefits of multiple options. It's a good idea to discuss your options with a financial advisor before proceeding.

Consider low-cost index funds

Index funds are a common investment choice for people with Roth IRAs. These are ETFs and mutual funds that hold multiple assets under a single ticker to give you exposure to multiple investment products through one type of asset.

Many financial institutions have built index funds specifically for people who are saving for retirement. Some of these are categorized by age. For example, one financial institution may offer an index fund for investors under 40 and a different index fund for investors who are near retirement.

These assets make it easy to diversify your retirement savings by allowing you to do so with a single asset purchase. However, index funds charge management fees that may eat into your annual returns. You'll need to take these fees into account when weighing how essential an index fund is. Conduct research to find the best low-cost options before making your final decision.

Review your investments regularly

Finally, all that’s left to do is to review your investments regularly. The investment strategy you choose today may not be the same one that’s right for you tomorrow. You don’t need to watch over your earnings and losses like a hawk, but you should check in every so often to ensure your account is still meeting your goals. If it isn't, discuss some alternatives with your financial advisor.

How to avoid common mistakes when investing in a Roth IRA

Setting up a Roth IRA can be an excellent way to save for retirement, but there are some common mistakes you should try to avoid.

For example, did you know that you can only roll over your Roth IRA once in a 365-day period? A rollover means withdrawing the funds from one tax-deferred retirement account and putting them into a new one. If you try to do that multiple times within 365 days, you could face hefty fines and penalties that may drain your account.

Another potential mistake is assuming a Roth IRA can’t work for you just because you exceed the income cap. It takes a few more steps, but you can contribute to a traditional IRA and then roll the money over into a Roth. Some 401k plans can also be converted into Roth IRAs.

A variety of little situations like this may or may not impact your Roth IRA goals. The easiest way to make sure you avoid all of those potential mistakes is to consult with a financial expert while setting up your account.

Roth IRA Contribution Limits

In 2023, the maximum amount you can contribute to your Roth IRA is $6,500, or $7,500 if you’re 50 or older. However, not everyone will be able to contribute the full amount. The IRS limits Roth IRA contributions for high-income earners. Consider the following chart and check your tax return to learn more.

| Filing Status | Modified Adjusted Gross Income (MAGI) | Contribution limitations |

| Married filing jointly or as a qualifying widow(er) | Under $218,000 | Up to the full IRA limit |

| Married filing jointly or as a qualifying widow(er) | More than $218,000 but less than $228,000 | A reduced amount that scales down as income rises |

| Married filing jointly or as a qualifying widow(er) | More than $228,000 | You cannot contribute to an IRA |

| Married filing separately and you lived with your spouse at any point during the year | Under $10,000 | A reduced amount that scales down as income rises |

| Married filing separately and you lived with your spouse at any point during the year | More than $10,000 | You cannot contribute to an IRA |

| A single, head of household, or married and filing separately and you didn't live with your spouse at any time during the year | Under $138,000 | Up to the full IRA limit |

| A single, head of household, or married and filing separately and you didn't live with your spouse at any time during the year | Over $138,000 but under $153,000 | A reduced amount that scales down as income rises |

| A single, head of household, or married and filing separately and you didn't live with your spouse at any time during the year | Over $153,000 | You cannot contribute to an IRA |

| Source: Internal Revenue Service |

Withdraw Early from your Roth IRA

You can withdraw contributions from your Roth IRA whenever you want, tax and penalty-free. However, taking out investment earnings too early may result in an early withdrawal penalty unless it’s for a qualifying distribution or if you meet certain Roth IRA withdrawal exceptions. Exceptions include purchasing your first home, qualified education expenses, disability or having a child, to name a few.

Additionally, distributions from Roth IRAs are more flexible for retirees than those of Traditional IRAs. Under Traditional IRAs, individuals must withdraw a required minimum distribution (RMD) by the age of 72 ½. Meanwhile, Roth IRAs have no such requirements — unless you have inherited a Roth IRA.

To make "qualified distributions" in retirement, you must be at least 59 ½ and at least five years must have passed since you first began contributing. Depending on your bank or the investment company of your choice, a Roth IRA application can be completed in just under 15 minutes.

Once you open an account, you’ll need to decide how you want to invest the money that goes into your Roth IRA portfolio. You can ask a financial advisor for help, but it’s easy to do it yourself.

Investments can be set up in your Roth IRA by either customizing your portfolio and picking investments, options, stocks, or exchange-traded funds (ETFs), or by purchasing a mix of individual stocks and bonds.

Keep in mind that there are some items that the IRS prohibits you from including in your Roth IRA. These include certain collectibles and life insurance.