Why a Little Inflation Might Not Be Such a Bad Thing

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

- What Happens If the Social Security Trust Fund Runs Out in 2034?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Most people don't like inflation. If the prices of your groceries go up, you have good cause to complain about the rising cost of living. If you are saving for the long-term, you have to build an investment portfolio that defends against the gradual reduction in your earnings power. At a personal level, inflation is always a threat. Or, at best, a nuisance.

But many economists and monetary policymakers say that, in the big picture view, too low inflation can be just as worrying as high inflation. Slowly rising (or even falling) prices is a sign of an economy with too much slack. Prices rise slowly because consumers aren't spending, and consumers aren't spending because they aren't getting raises or replacing lost jobs.

That's why the Federal Reserve has been signaling since early 2012 that it wants to keep its foot on the economy's gas until inflation is running at least 2% per year. (The Fed tries to regulate the speed of growth by setting interest rates.)

As Money's Paul Lim notes, in the financial markets, there's a pretty strong consensus that inflation will remain quite low for some time. Paul's view is that investors might be in for a surprise.

If he's right, that might be bad news for your bond fund. But one Fed official, Minneapolis Federal Reserve president Narayana Kocherlakota, will take it as good sign. Once known as one of the Fed's inflation "hawks" (as opposed to the "doves" who usually favor a looser stance), Kocherlakota has raised the idea of a more aggressive inflation target. Here is his case:

- Low inflation is bad for borrowers. Inflation hurts a saver because it lowers their real returns. If you buy a bond that pays 2% and inflation hits 3%, you've lost money. The flip side is what happens if you take out a mortgage at 4% and expect 3% inflation. Assume that over the long run incomes rise along with inflation. If inflation turns out to be 2% instead of 3%, that 4% loan turns out to be much more costly in real terms than the borrower expected. (Another way to think about this is that if you borrow money and then inflation hits, you get to pay back the loan with less valuable money.)

- The economy is still much more slack than it looks. In Kocherlakota's view, the current 6.7% unemployment rate, though much better than it's been in the recent past, is not a sign of true economic health. Much of the drop in unemployment is due to a decline in the number of people actually looking for work. Fewer than 77% of Americans aged 25 to 54 have jobs right now, compared with more than 80% before the Great Recession. Almost 5% of workers are part-time but would prefer to be full-time, vs. fewer than 3% in 2007.

So although most people don't like inflation, Kocherlakota is saying that for most people a low-inflation world ain't so hot either. Inflation is often said to punish savers—that is, people who have already saved. For younger people who'd like to build up saving in the future, however, a stronger job market might be worth some inflation. In reasonable doses.

Figuring out the dosing really is the tricky part, though. Instead of keeping up stimulus efforts until inflation hits 2%, Kocherlakota suggests, why not aim instead for a certain level of prices? This sounds like a wonky distinction, but since inflation has been running below the Fed's target for some time, the price-targeting approach would leave the Fed room to maintain low rates (and delay unwinding "quantitative easing") even if inflation rose above 2% for a while.

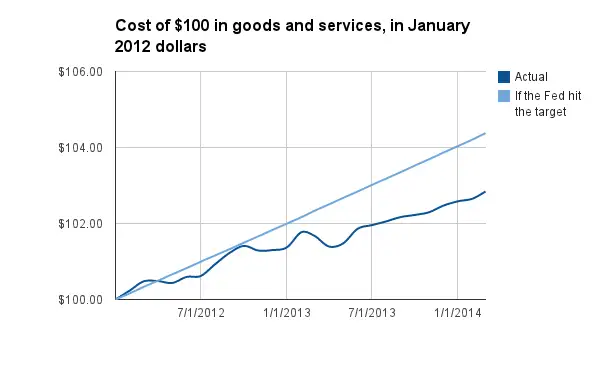

Because prices have a lot of catching up to do. Below is how prices have risen since the Fed announced it's target. If they had actually hit the mark, they'd be 1.4% higher today.

Does the fact that someone inside the Fed system is making such an argument signal a push for higher prices ahead? As a regional bank president, Kocherlakota is one of just twelve votes on the Fed's rate-setting body this year, and next year he won't have a vote, because the regional seats rotate. And Fed chair Janet Yellen hasn't been willing to call for inflation higher than the 2% target. Kocherlakota is staking out one end of the Fed's consensus here.

But whatever your view on the dangers of higher prices, or your guess about whether higher inflation is really on the way, it certainly makes sense for a long-term saver to hedge against inflation risk.

Stocks over the long-run should provide some protection. As prices rise, so should the nominal earnings of companies. For investors looking to keep money safe, though, a better bet is Treasury Inflation Protected Securities, or TIPS, the government bonds that come with built-in inflation protection. Their principal value rises along with the consumer price index.

Right now, a 10-year TIPS bond has a yield of just over 0.4%. That's terribly low. But it also represents a real, after-inflation yield that you'll get no matter what happens to the CPI. By comparison, you can buy a regular Treasury that yields 2.6%. That means if inflation comes in at an average of about 2.2%—a little higher than it is now—you get the same real yield as you would in the TIPS bond. (2.6% - 0.4% = 2.2%.)

That means inflation hedging is a reasonable bet even if you don't see dramatically higher prices ahead. If inflation comes in below 2.2%, you'll be glad you owned regular Treasuries. If it comes in anywhere above that, you'll have done better in TIPS. So hold some of both flavors. Inflation hedged bonds are especially attractive for money you've set aside to meet specific spending needs, since they preserve your real purchasing power. You can buy TIPS individually at TreasuryDirect.gov or hold them via a specialized mutual fund. Vanguard Inflation Protected and Vanguard Short-Term Inflation Protected are two low cost choices on the Money 50 list of recommended funds.

Be aware that TIPS, like any Treasury, stand to lose market value if interest rates rise. That's less of an issue if you plan to hold the bond to maturity, but the value of a TIPS mutual fund will fluctuate. A fund focused on short-term TIPS will give you less interest rate risk, at the expense of yield.