The Ages When Most People Retire (Hint: Probably Too Young)

You've heard the horror stories about many Americans retiring with puny nest eggs and little income to live on. Still, data show that more than two-thirds of Americans are out of the full-time workforce by age 66.

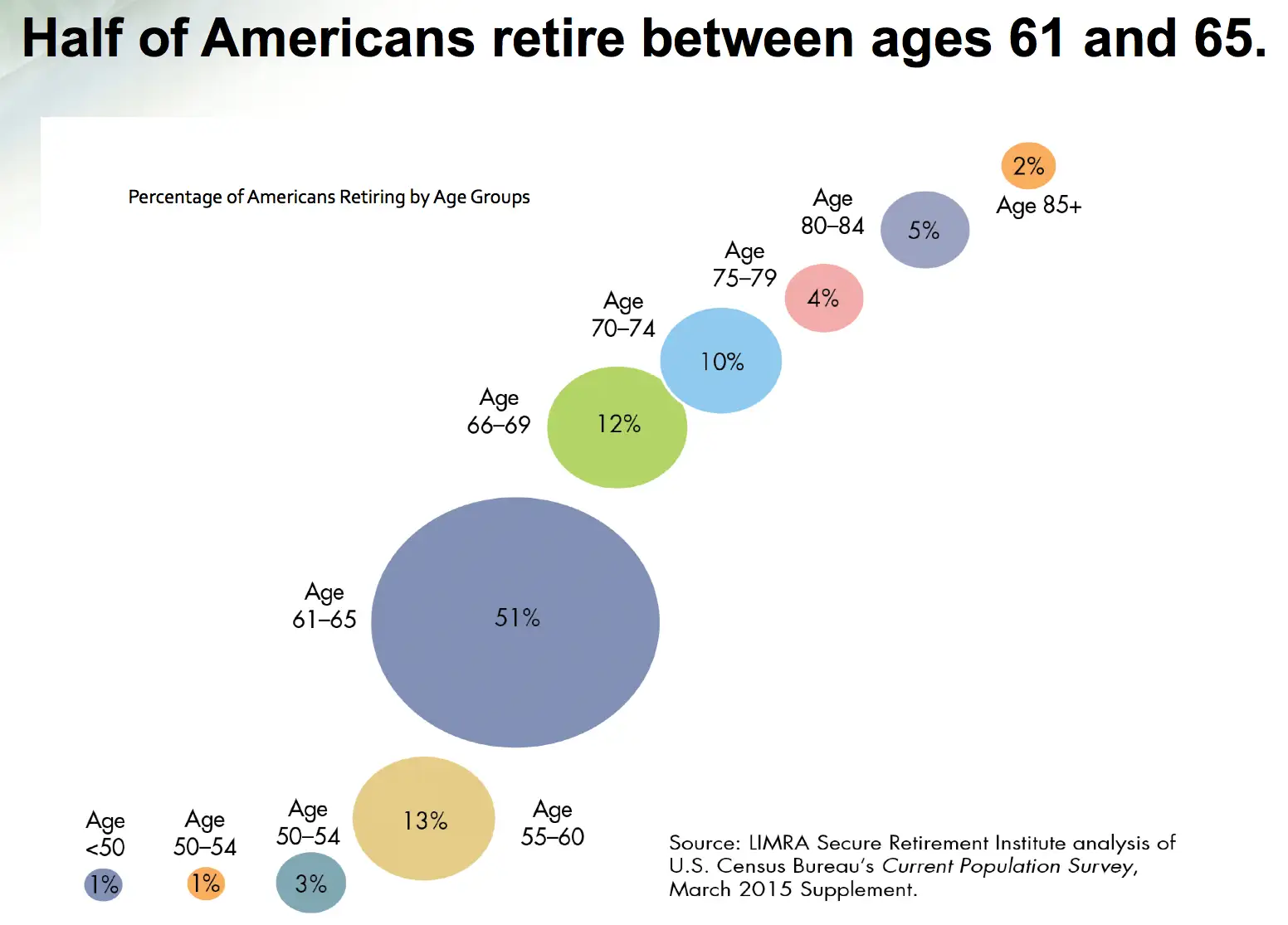

About half of Americans call it quits between ages 61 and 65 while 18% retire even earlier, according to the data shown here from LIMRA Secure Retirement Institute. By age 75, 89% of Americans have left the labor force, LIMRA says.

The retirement statistics no doubt include some people who can't find work or who can't work because of health problems. Still, early retirement can mean an income squeeze.

Along with stopping work early, most Americans begin collecting Social Security before their full retirement age, which is 66 for many and rises to 67 for those born after 1960, LIMRA says in a recent report.

The percentage of those claiming Social Security early is declining. That’s generally good news because monthly benefits rise by roughly 6.5% to 8% a year between ages 62 and 70. Still, in 2014, 57% of men and 64% of women took the benefit early, LIMRA says.

Half of leading-edge baby boomers, those ages 61 to 69, have fully retired and about 15% of the U.S. population is now finished with work. Among this group, the presence of a traditional pension or retirement plan is often what separates those considered income-rich from those who are not, LIMRA found.

Retired Americans receive $1.3 trillion in income. The vast majority of this income comes from two sources: Social Security (42%) and traditional pension and retirement plans (30%). Traditional pensions remain fairly common for those over 75 but are virtually nonexistent for those under 34, LIMRA found.

Some 41% of retirees have annual income less than $25,000, and of those, only 21% receive income from a pension or retirement plan. Meanwhile, of retirees with income over $50,000 a year, about 80% draw from a pension or retirement plan.

To get a picture of how severe the retirement income crisis is—and why more Americans should consider working longer and delaying Social Security—LIMRA looked at total savings. U.S. households own $31 trillion of investable assets. That’s an average of $253,200 per household. But most of that is owned by the wealthy. The median holding is just $17,500 and three in four American households have saved less than $100,000.