3 Moves to Boost Income Even When Rates Are Low

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

It’s been nearly a year since the Federal Reserve hiked interest rates for the first time in a decade. Yet far from ringing in a new era of rising bond yields, the central bank has yet to make another move. Even if the Fed finally gets around to lifting rates in December—as some economists predict— policymakers are still likely to be cautious next year. In fact, Fed officials currently anticipate only two modest quarter-point rate increases in 2017.

Why so timid? The Fed finds itself walking a tightrope of wanting to return rates to something closer to normal without causing the weak economic recovery to stall. As the Fed takes things slowly, fixed-income investors who have been waiting for the market to do the heavy lifting when it comes to boosting yields now have to go back to the drawing board to find ways to generate sufficient income without taking on too much risk.

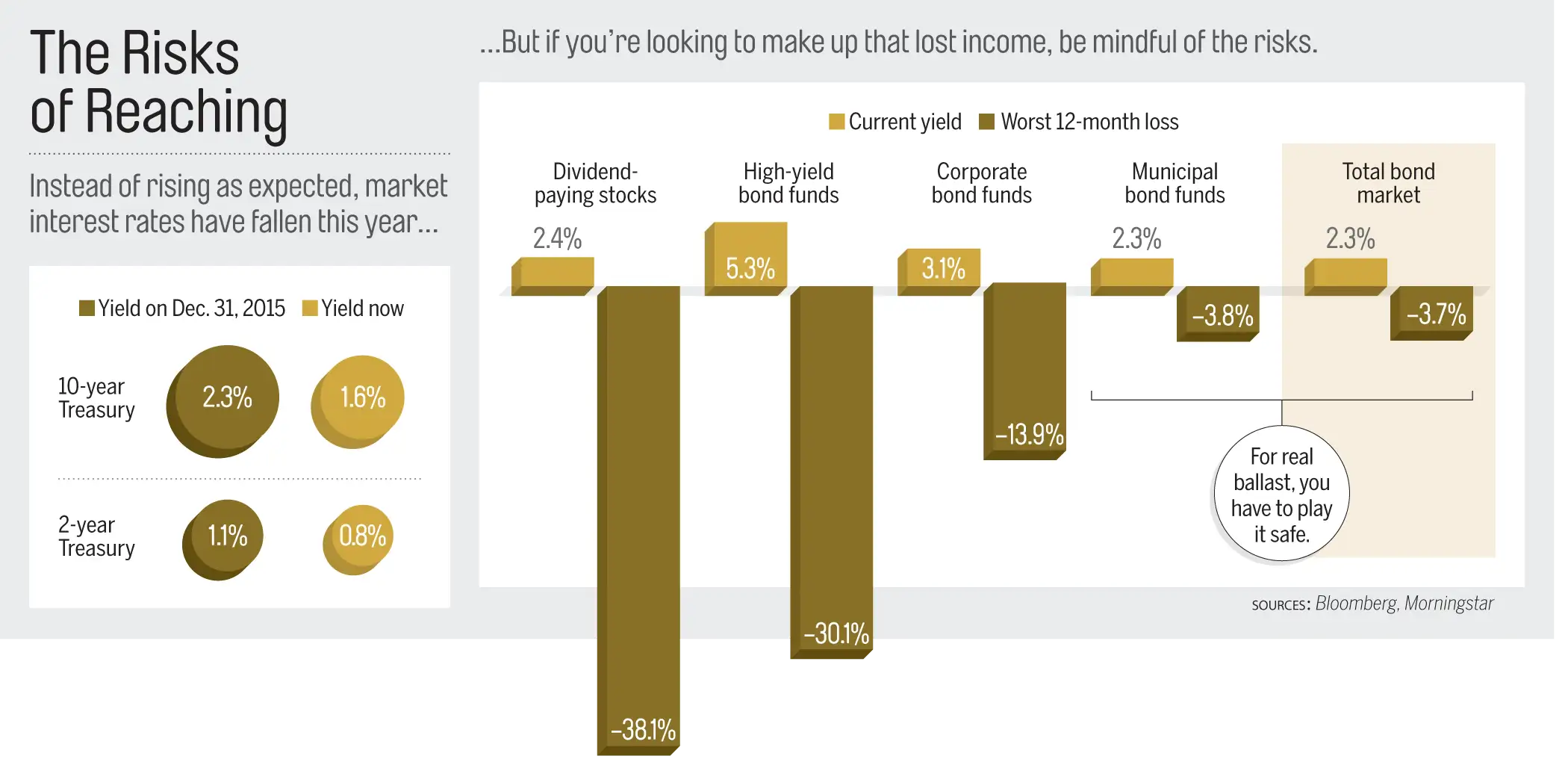

Not that the Fed is entirely to blame for low interest rates. As frustrating as the 1.6% yield on 10-year Treasuries is to Americans, it is manna from heaven for investors in Europe and Japan who are grappling with what was once unthinkable: negative interest rates.

As a result, overseas investors seeking relief have been pouring money into U.S. debt. That has lifted prices on longer-term bonds, causing market interest rates to fall and putting the Fed in a bind.

U.S. policymakers know that if they’re too aggressive with rate hikes, they run the risk of spurring more foreign demand for Treasuries. As that happens, the U.S. dollar will gain strength against global currencies, making American goods less affordable abroad and threatening growth. That’s something the Fed is not keen to do. “Pull it all together, and we have the pieces for bonds to remain in a low-volatility range,” says Jeffrey Moore, manager of Fidelity Investment Grade Bond .

This presents both a challenge and an opportunity for investors looking for higher income than Treasuries can offer, without taking on too much added risk. Here’s how to rethink your income game plan.

Bet on bond blue chips

Low unemployment, decent job growth, and a slight increase in wages are signs that the U.S. economy continues to heal and grow, with no imminent threat of a recession. Against this backdrop, corporate debt issued by companies with strong balance sheets offers a mix of stability with higher payouts over super safe Treasuries.

The 2.7% yield on Standard & Poor’s index of investment-grade bonds, for instance, is more than one percentage point higher than what you could earn on a comparable length Treasury bond. Moreover, high-quality corporate bonds are a tad less sensitive to interest rate changes than government bonds. So in the event there is a moderate uptick in rates later this year or next, corporate bond prices aren’t likely to fall as much as Treasuries.

Read: Why Interest Rates Won't Get Back to Normal Until at Least 2025

One way you can gauge the interest rate sensitivity of your bond fund is through a measure called duration, which you can look up for free at Morningstar.com. If a fund has a duration of five years, that means it is likely to rise or fall in price about 5% given a one percentage point change in market rates.

Moore says corporate issues with durations of four to eight years are the sweet spot for grabbing a bit more yield without taking on the volatility that comes with longer-term issues.

Since total market index funds are loaded with low-yielding government bonds, adding some active management will give your bond portfolio a bit more of a corporate tilt. Dodge & Cox Income , on our Money 50 recommended list, holds 48% of its assets in corporate debt, yields 3.2%, and has a duration of four years. If you prefer an index option, go with a fund that just focuses on high-quality corporates, such as Vanguard Intermediate-Term Corporate Bond ETF , yielding 3.2% with a duration of 6½ years.

Make room for munis

As the economy grows, so too do the tax revenues of cities and states. That’s a solid foundation for tax-advantaged municipal bonds. Anthony Valeri, strategist for LPL Financial, says that the low supply of new issues is another plus and that munis have historically been “more resilient” than Treasuries and corporates when rates rise.

Today’s 2.1% average yield on a high-quality A-rated 10-year muni is already a step ahead of the 1.6% yield on a 10-year Treasury. Add in the tax break and the payout looks even better. A 2.1% muni yield is equivalent to earning 2.8% if you fall in the 25% federal tax bracket and 3.1% if you land in the 33% bracket.

Marilyn Cohen, chief executive officer of bond investment firm Envision Capital Management, favors munis backed by revenues from a specific project like a toll bridge, rather than “general obligation” bonds relying on basic tax receipts: “We have learned from Puerto Rico, Detroit, and Stockton [Calif.] that general obligation is not rock solid.” Money 50 fund Vanguard Intermediate-Term Tax Exempt keeps nearly 70% of its portfolio in revenue bonds.

Dip a toe into the junk pool

Earlier this year, an index of high-yielding “junk” bonds paid nearly 8.5 percentage points more than Treasuries. After a ferocious rally, junk’s yield premium is down to a below-average five points. Still, earning a yield of 6% or more is plenty compelling in this market.

Given that the economic expansion and bull market are in the late stages, though, don’t get greedy by wading into the riskiest end of the junk market—bonds graded CCC or unrated. Valeri also recommends limiting your high-yield exposure to no more than 10% of your fixed-income portfolio—and favoring higher-quality junk over the lowest-rated stuff.

You don’t need to add a specific junk fund to your mix. Fidelity Investment Grade Bond, for instance, currently holds about 8% of the fund’s assets invested in high-yield debt, with most focused on “fallen angel” issues that have lost their investment-grade rating but that manager Moore believes will eventually return to that status. Currently, BB-rated bonds—which are one step below investment grade—yield more than 4.5%.

Calculator:

For a junk-only fund, check out Fidelity High Income , a Money 50 fund with more than 70% of its assets in BB- or B-rated bonds.

To further reduce risk, build your high-yield exposure not by shifting money out of your high quality bonds, but rather from your stock allocation, as this slice of the fixed-income market has equity-like risks.

Beware the dividend trap

With bond yields so low, stocks with decent dividend yields can look like alluring bond replacements. After all, the 2% yield on the S&P 500 index of blue-chip U.S. stocks is slightly more than what 10-year Treasuries are paying. And the average yield of dividend-paying shares is nearly one percentage point higher than government bonds.

Don’t fall for this. As the chart shows, swapping your bonds for equities means giving up one of the primary reasons you own bonds in the first place: to provide ballast for your portfolio. Indeed, in the financial panic of 2008, some dividend stock funds lost nearly as much as the broad market while total bond market index funds gained ground.

Read: Where to Find Dividend Payers Now

Also, many traditional dividend-paying stocks tend to be in sectors sensitive to interest rates, meaning that if rates rise, their share prices are likely to fall. When the yield on 10-year Treasuries shot up from January 2015 to June 2015, utility shares lost more than 11% of their value.

The bottom line, says Envision Capital’s Cohen, is that “income from a stock and income from a bond are not equatable.”