Money Makeover: 30 Years Old, and Already Falling Behind

Chianti Lomax grew up poor in Greenville, S.C., raised by a single mother who supported her four children by holding several jobs at once. Inspired by her mom, Lomax worked her way through high school and college; today, the Alexandria, Va., resident makes $83,000 plus bonuses as a management consultant.

But turning 30 last December, Lomax had an epiphany: Her career and her 401(k)—now worth $35,000 —weren’t enough to achieve her long-term goals: raising a family and buying a house in the rural South.

Her biggest problem, she realized, was her spending. So she downsized from the $1,200-a-month one-bedroom apartment she rented to a $950 studio, canceled her cable, got a free gym membership by teaching a Zumba class, and gave up the 2010 Honda she leased in favor of a 2004 Acura she paid for in cash. With those savings, she doubled her 401(k) contribution to 6% to get her full employer match.

And yet, nearly a year later, Lomax has only $400 in the bank, along with $12,000 in student loans. Having gone as far as she can by herself, Lomax wants advice. As she puts it, “How can I find more ways to save and make my money grow?”

Marcio Silveira of Pavlov Financial Planning in Arlington, Va., says Lomax is doing many things right, including avoiding credit card debt. Spending, however, remains her weakness. Lomax estimates that she spends $500 a month on extras like weekend meals with friends and $5 nonfat caramel macchiatos, but Silveira, studying her cash flow, says it’s probably more like $700. “That money could be put to far better use,” he says.

The Advice

Track the cash: Silveira says Lomax should log her spending with a free online service like Mint (also available as a smartphone app). That will make her more careful about flashing her debit card, he says, and give her the hard data she needs to create a budget. Lomax should cut her discretionary spending, he thinks, by $500 a month. Can a young, single person really socialize on $50 a week? Silveira says yes, given that Lomax cooks for herself most evenings and is busy with volunteer work. Lomax thinks $75 is more doable. “But I’d like to shoot for $50,” she says. “I like challenging myself.”

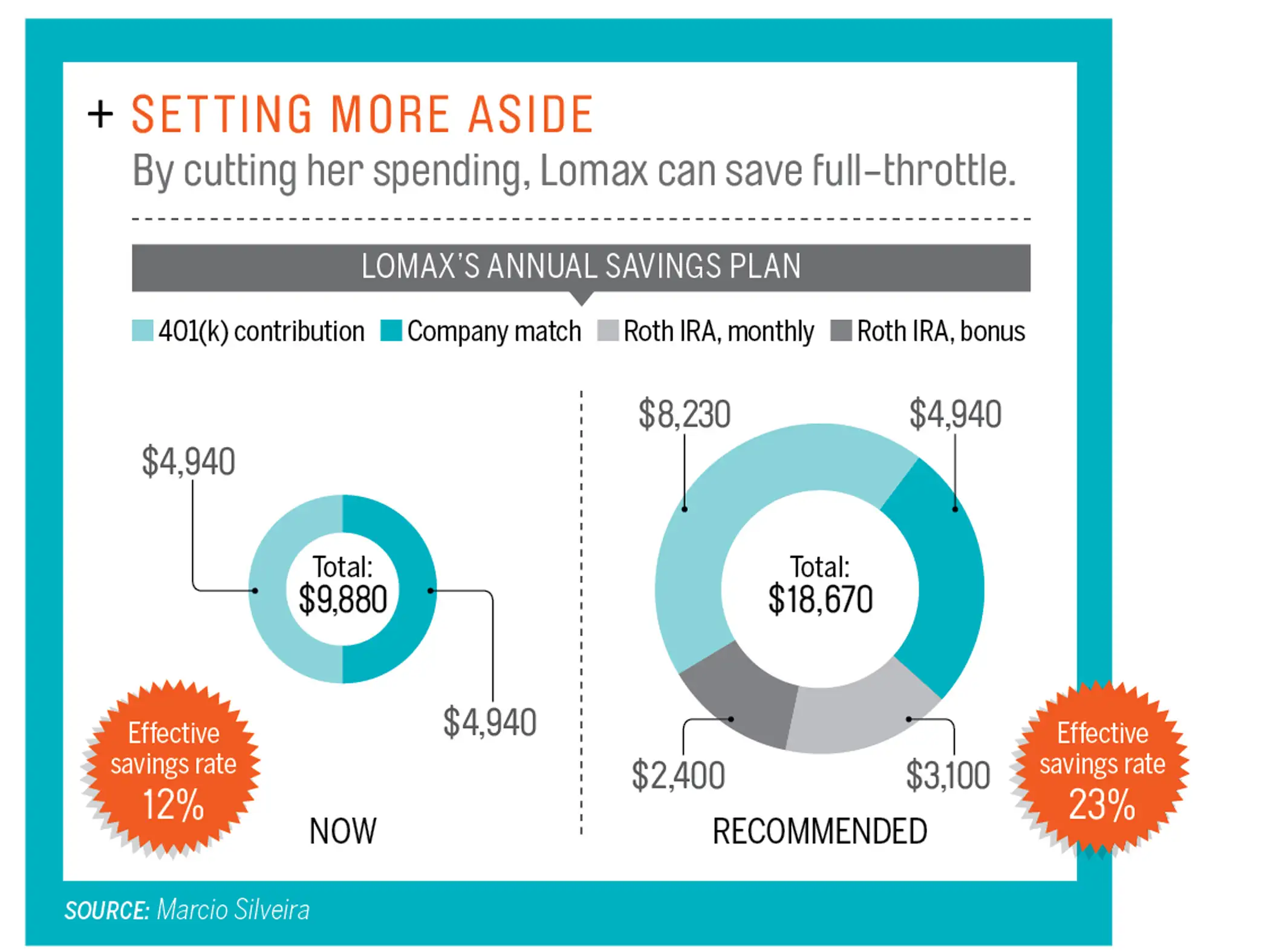

Automate savings: Saving money is easier when it’s not in front of you, says Silveira. He advises Lomax to open a Roth IRA and set up an automatic transfer of $200 a month from her checking account, adding in any year-end bonus to reach the current annual Roth contribution limit of $5,500, and putting all the cash into a low-risk short-term Treasury bond fund.

Initially, says Silveira, the Roth will be an emergency fund. Lomax can withdraw contributions tax-free, but will be less tempted to pull money out for everyday expenses than if the money were in a bank account. Once Lomax has $12,000 in the Roth, she should continue saving in a bank account and gradually reallocate the Roth to a stock- heavy retirement mix. Starting the emergency fund in a Roth, says Silveira, has the bonus of getting Lomax in the habit of saving for retirement outside of her 401(k).

Ramp it up: Lomax should increase her 401(k) contribution to 8% immediately and then again to 10% in January—a $140-a-month increase each time. Doing this in two steps, says Silveira, will make the transition easier. Under Silveira’s plan, Lomax will be setting aside 23% of her salary. She won’t be able to save that much upon starting a family or buying a house, he says, but setting aside so much right now will give her retirement savings many years to compound.

Read next:

12 Ways to Stop Wasting Money and Take Control of Your Stuff

Retirement Makeover: 4 Kids, 2 Jobs, No Time to Plan