How Soccer Bills Devoured This Family's Budget

LIKE MOST PARENTS, Steve and Siobhan Jones of Folsom, Calif., will do just about anything to support their children's passions. But the Joneses are the parents of four talented, soccer-crazed boys, which means that life can get a little bonkers.

Take a four-day weekend this summer. It starts at 5 a.m on Friday when Steve, a 47-year-old senior network engineer at Intel, and his 14-year-old son, Rhys, set out in their rental car on a 10-hour drive to San Diego for the latest big tournament. Before Rhys hits the field, Siobhan, 43, a part-time elementary school teacher, has piled her three younger boys—Kye, 13, Taine, 11, and Bryn, 9—into her 2009 Honda Pilot for their own tournament three hours away in Santa Cruz. They'll sleep in a rented Airstream trailer. (Left at home: the family's creaky minivan.)

On Saturday and Sunday, Siobhan scurries among the eight games played by Taine's and Bryn's individual teams. (Kye's team, mercifully, has the weekend off.) Meanwhile, Steve watches Rhys play three games, then drives the eight hours from San Diego to Santa Cruz, where all six jam into the Airstream's four sleeping berths. After a pit stop to ride the roller coasters on the Santa Cruz Beach Boardwalk, they get home Monday at midnight—exhausted, happy, and (after shelling out for lodging, car rental, gas, meals, and amusement park tickets) $2,000 poorer.

And that's just one weekend. Unlike playing on the local parks and rec team, the Jones boys compete in the elite world of American soccer clubs. For kids at this level, soccer isn't just a game. It's their lives. Top young athletes play year-round and practice as often as a dozen times a week. There are specialized, private coaches and $100 cleats. The playing, or club, fees alone run to $675 a month. Last year, Steve and Siobhan (pronounced "Shih-VAWN") paid $17,400 for soccer-related expenses, by far the biggest item in their budget after their mortgage. As much as they support their boys' dreams to play in college, the financial support required sometimes gives them nightmares. "We're living in the moment, going month to month to make this work," says Steve. "We have no money or time to spend on anything else."

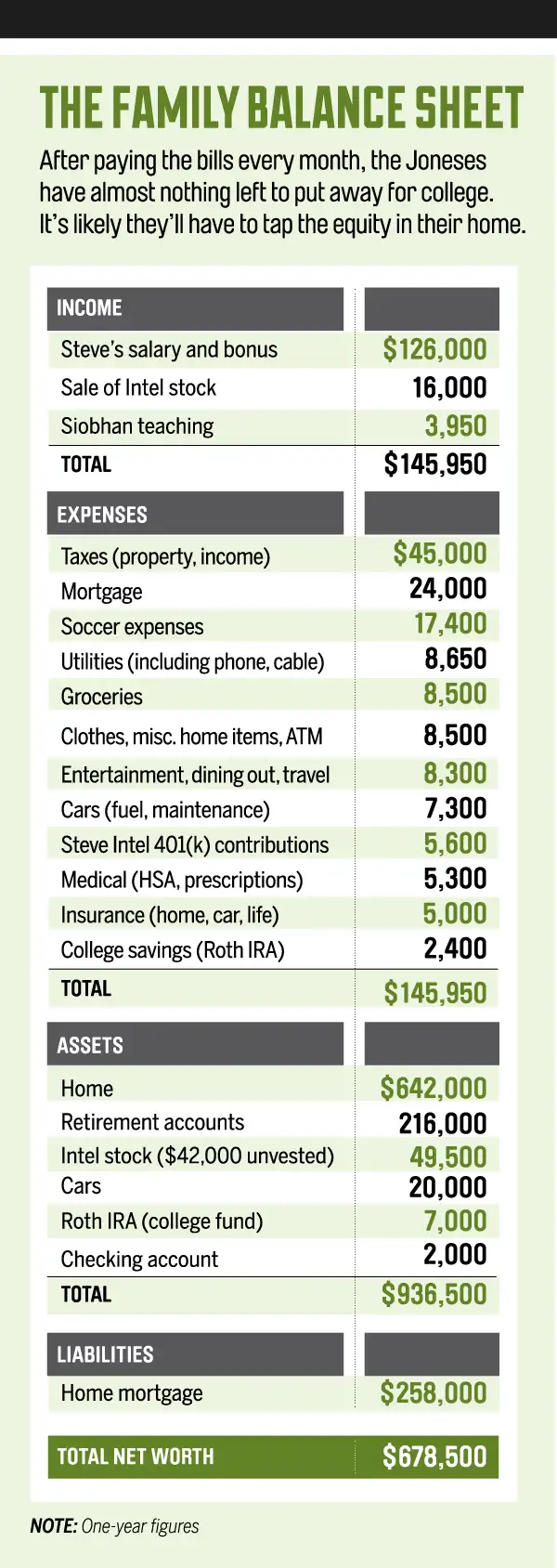

He is not exaggerating. Even with a healthy $146,000 in combined annual income—most from Steve's $126,000 Intel salary—the family barely makes ends meet. With all their expenses, they have managed to tuck away only $9,500 for emergencies. Perhaps more ominous for their long-term financial health: They have saved just $7,000 for college. That would be a major concern for many families; for the Joneses, who have four boys to educate, that is a ticking time bomb that's set to explode in 2022, when three of the kids are in college at the same time. "We do panic about that," says Siobhan.

The Joneses' situation may sound extreme, but the challenge of balancing the cost of athletics and academics is far from unusual. Some 21 million kids play under-17 competitive sports in the U.S., according to ESPN.com. All told, families spend about $5 billion a year on sports organizations, an analysis by the Columbus Dispatch shows, and another $7 billion on related travel, says a National Association of Sports Commissions study. Soccer in particular has boomed in popularity. The U.S. Youth Soccer Association is now the largest youth-sports organization in the country. In the Sacramento area alone, where the Joneses live, there are more than 42 competitive soccer clubs.

Clearly, Steve and Siobhan wouldn't have invested the considerable money and time if their boys didn't reap so much from their sport. "They get to mix with quality kids, they're doing something good for them, and they're learning life skills that will help them get on in the world," says Siobhan. Besides, their kids are talented and well-coached. "You don't quite realize how good they are until you see them play against kids at school—I'm like, "Holy smokes!" " she says.

Yet this is where soccer plays a tricky role in the Joneses' lives. They sacrifice because their boys love it, but in the back of their minds they hope their investment will pay real dividends—in the form of college scholarships. "If Rhys plays national tournaments," says Steve, "maybe he'll catch the eye of recruiters." Rhys's coaches think he might well have the right stuff. "He is still young," says his coach Marcos Mercado, "but he has potential because he's so tenacious and hardworking."

The problem is that whatever Rhys's (and his brothers') talent, the odds are against them. Only about 2% of high school athletes receive sports scholarships each year, with a fraction getting full rides, says the NCAA. "Sending your kid to college is such an emotional and expensive process that misinformation spreads quickly among parents," says Matt Wheeler of SportsRecruits.com, which helps high schoolers connect to college coaches. "That "scholarship" you heard about may be just fees and books."

With so much at stake, the Joneses know they have to get their house in order. They are about to begin. "With little safety net for emergencies and Rhys starting college in four years, they are in trouble," says Jeff Maas, a planner with Retirement Security Centers of Sacramento. "Something has to give."

THE JONES FAMILY'S devotion to sports started with Steve, who was born in Wales but grew up playing soccer and rugby in England. He met Siobhan at a pub in Bath in 1998, when she was an elementary school teacher, and they were married on a beach in Sri Lanka two years later. In 2008 he was working in IT at Intel's Swindon office when he learned that a downsizing could cost him his job unless he took a similar position in California. The boys, ages 2 to 7, were sad to leave England but acclimated quickly when their parents signed them up for recreational soccer.

When Rhys was 9, a coach asked him to try out for the local El Dorado United Soccer Academy. "All the boys are athletic, but Rhys has the advantage of also being very clever," says Steve. "He must take after his mother." Steve was thrilled that his son made the team, with its professional coaches and extended playing season. But he was stunned by the first bill: The $350 registration fee was more than an entire year of rec soccer, and the membership fee was another $115 per month. "That's when the costs really hit home," he says. Soon Kye wanted to join the club, followed by Taine (Bryn was too young). The price tag soared to $330 per month, plus $1,050 in annual registration fees.

But how does a parent say no when his kids are clearly thriving? In their spacious backyard that's home to two soccer nets, the Jones boys spend their rare free time drilling shots at one another, their booming kicks slicing through the air like drones on a mission. Most of the balls find the net, but a few bounce off the windows that, miraculously, have never been shattered.

The day after their four-day weekend, they're still reliving their soccer marathon. Bryn and Taine are psyched because their teams won in the finals—Bryn was the winning goalie and Taine scored a goal in his team's 6–0 victory on Sunday morning with a freakishly good move. "I couldn't hit the ball with my foot or my head, so I kind of hit it with my hip and it went in," he says with a smile as broad as, well, a soccer goal. On the other hand, Rhys is down because his team lost all three games. Kye is the most miserable of all because his team didn't even play. "I really wanted to run out there," Kye says.

Of the four, little Bryn is actually the biggest talker. He likes to be in charge. Taine has a wicked sense of humor and is popular enough to have been named team captain. Kye is easygoing, able to shop with Mom for hours without complaint. He's the only one who says he may not want to be a pro soccer player; he may want to play rugby (like his dad). Rhys believes he can do anything he puts his mind to.

If Steve ignited the boys' love for sports, Siobhan is the keeper of the flame. She picks up her kids at three different schools and shuttles them to practices, plus volunteers 10 hours per week as manager of their soccer club, scheduling their games, among other things. She spent her 43rd birthday watching Taine and Bryn play those four games at the Santa Cruz tournament. She didn't get a birthday dinner or even a cake, though Bryn's team gave her a cookie and sang "Happy Birthday." The best gift? "They both won!" she says.

STEVE AND SIOBHAN knew soccer was expensive, but they had never actually added up the numbers. At Money's request, they dug out their receipts and made some sobering discoveries. They were fully aware of only about half of their out-of-pocket costs—the San Juan Soccer Club's $8,100-per-year team-membership fees that show up on their bank statements ($675 a month) and the club's $100-per-child annual tournament fees.

The rest surprised them. In the past year they had paid $6,200 for travel to eight tournaments, including $2,400 for restaurants and the rest for hotels, car rentals, and gas. Cleats and other gear cost $1,200 a year, while the special ball-striking coach who gives all four boys private lessons runs $30 a week ($1,500 a year). "It's much more than I thought," says Steve. "It's the smaller stuff that goes out in dribs and drabs that really adds up." Adds up indeed. Once they've crunched the numbers, the Joneses realize that 17% of their after-tax income goes to soccer.

No wonder there has been so little left over for an emergency fund. When spending gets heavy, Steve often sells some of the $15,000 in restricted stock units he receives from Intel each year. They've still got $7,500 of this year's allotment, along with $2,000 in their checking account. He also has $42,000 in unvested stock and can sell off and net about $1,000 per year via a discounted employee stock plan.

Bringing in more income would certainly help, but Siobhan's earning potential is hampered. Because her British teaching degree isn't valid here, she'd need to take some classes in order to get certified. "The idea of going back to school is daunting, spending thousands of dollars to be taught what I already know how to do," she says. Instead, she works part-time teaching computer skills at elementary schools, averaging about 10 hours a week at $13 per hour. That brings in just $4,000 a year but leaves her free to shuttle the boys.

The family also tries to be frugal. Siobhan polishes her own nails and cuts the boys' hair in whatever crazy style they're looking for. (They are all currently sporting mohawks.) The Joneses know they can't afford to replace their aging carpets, and they've begun to wonder where to find the money to replace their two old cars: Siobhan's Honda and Steve's 2008 Town and Country minivan.

That said, they do have other resources, starting with the $384,000 equity in their five-bedroom, 2,700-square-foot house. They bought it in 2008, when housing prices in the U.S. had already started to slide but just before England's housing bust hit. They sold their home in Britain at the height of the U.K. bubble for $250,000 and bought their Folsom home during the U.S. slump for $550,000 with a down payment of $225,000. They opted for a 20-year mortgage with payments of $2,000 a month to reduce debt. The house is valued today at $642,000.

The Joneses also feel good about their retirement savings. They have $216,000 in several accounts that include a profit-share retirement plan from Intel. The company contributes 5% of Steve's salary ($6,500 a year). There's also a 401(k) plan in which Steve saves 4.5% of his salary ($467 a month). In addition, at age 65, they will qualify for about $14,500 a year from U.K. pensions.

It's what comes in the years before retirement that scares them. They are saving $200 per month for college, putting it into a Roth IRA because they want access to their contributions in case of an emergency. But they know that's not enough. With Rhys now a freshman in high school and only $7,000 set aside, Steve and Siobhan are worried about affording college, which will cost about $31,000 a year at a state school by 2019 and as much as $64,500 at private universities in the state. That translates to at least $500,000 for the four boys—assuming they all go to public, in-state schools.

Which is why the idea of a soccer scholarship is irresistible. Rhys took a step in that direction earlier this year when he was accepted by the elite U.S. Soccer Development Academy team. A partnership between the San Juan Soccer Club of Folsom and the Sacramento Republic FC, a minor-league professional team, the squad is one of the finest in the region, attracting players from as far away as Nevada. College coaches often scout teams at this level for prospects.

Rhys has more than soccer going for him. He was a straight-A student in middle school, and top grades can be a huge advantage for kids hoping to win an athletic scholarship. "Sports may also be an important piece of the puzzle that helps him get into a good school, where he might qualify for aid based on merit or financial need," says Jill Yoshikawa of Sacramento's Creative Marbles Consultancy, which helps families prepare for college admissions. But even for players on prestigious teams, substantial aid is a long shot. "College soccer teams can divide scholarship money among many players so you may get something, but it's usually minimal," Yoshikawa says.

The bottom line? The Joneses can't count on athletic scholarships to solve their problems. But they can find a way to pay for all their boys' educations. What they need, says planner Jeff Maas, a registered representative of Lincoln Financial Advisors, is a smart battle plan.

THE ADVICE

The Joneses occupy an all-too-familiar no-man's-land: They're not saving enough for their children's college careers yet they earn too much to qualify for need-based grants. But their situation may not be so dire, says Yoshikawa and our other advisers. Here are their recommendations.

Get serious about college saving. Steve and Siobhan first need a realistic idea of how much they'll have to come up with for the boys' education. The good news: Their potential out-of-pocket costs are not as onerous as they imagine, largely because financial aid formulas give a break to families when they have more than one child in college at the same time. The bad news: Even with that break, the Joneses are still woefully behind.

According to federal guidelines, their estimated family contribution (EFC)—the amount the Joneses are expected to pay—will be around $26,000 a year when Rhys goes to college, but that amount will drop to $13,000 per student when they have two children in college and $8,700 when they have three. The $7,000 they have socked away so far is just a drop in that educational bucket.

Saving in earnest to close the gap needs to begin now, Maas says. He recommends that Steve and Siobhan set up four separate 529 college savings plans, one for each boy. For starters, they should aim to contribute a total of $1,000 a month, with $300 going into Rhys's account because he's closest to enrollment, and roughly $200 set aside for each of their younger sons (advice about how to free up that cash follows). With an estimated 6% return, the plans would provide an average of about $11,000 per year of the $31,000 cost of a state college.

Hunt for academic grants (not just athletic ones). Though they can't count on athletic scholarships—no student athlete can—they may qualify for additional need-based California state grants once they have more than one kid in college at the same time (even more when they have three). Based on their grades, the boys may also qualify for nonsports merit aid, which can be preferable to athletic grants, says Paula Bishop, a college planning specialist in Bellevue, Wash. "Academic scholarships are given for four years while sports scholarships are often guaranteed only for the first year," she explains.

Though the sticker price on in-state public colleges is obviously less, Bishop says that Rhys and his brothers may have a better chance getting aid from private schools. That could result in a lower net price. These colleges often have more generous merit-aid budgets, especially for students who are in the top 25% of the applicant pool—so the Jones boys should keep up their grades and put those schools on their lists. (For help identifying colleges that provide the most merit aid and overall value, check out the Money College Planner.)

Meanwhile, once they're in high school, the boys should maximize their odds of finding athletic scholarships by getting on the radar screen of college coaches. (Here are some tips on how to do that.) Even a small stipend would be helpful, especially combined with other aid.

Free up cash. Tapping into their home equity will allow the Joneses to jump-start their college savings and also build up the emergency fund they so desperately need. Extending the terms of their mortgage from the 13 years they have left now to 20 years will reduce their monthly payment by $500 yet still allow them to pay off the balance by the time Steve is 67. "They will pay more in interest over the life of the loan, but rates are still low, and they need the money now," says Maas. They can get the rest of the way there with judicious belt-tightening. One target: the $2,400 a year that goes to eating out at Taco Bell.

Prepare for trouble. In addition to cash for college savings, the Joneses also need about $35,000 in a liquid emergency fund to cover expenses for six months if Steve loses his job. They can get nearly halfway there by considering the $7,000 Roth IRA, which they've earmarked for college, as part of their rainy-day fund, along with the $9,500 they already have in reserve. The Roth isn't the best college savings vehicle, says Maas, because of its low annual contribution limit ($5,500 per person), and because distributions count as income in federal aid formulas, reducing eligibility.

Jog toward retirement, then sprint. If Steve continues his current pace of saving for retirement until age 65—$5,600 per year to his 401(k), plus Intel's contribution of $6,500—he and Siobhan would run out of money by age 83 (assuming a 6% return before retirement and 5% after as they invest more conservatively). Fortunately, when Steve is 60 and Siobhan is 56, they should be done paying for college. At that time, Maas suggests boosting Steve's 401(k) savings to the max (currently $24,000 a year for investors age 50 and older), while Siobhan puts the same amount into a 403(b), assuming she gets her credentials to teach full-time by then. By the time Steve is 65, their nest egg should be $1.75 million, not including pensions. With the refinanced mortgage paid off two years later, retirement plans plus Social Security should last to age 95.

WHAT DO THE JONESES think about overhauling their financial life? Steve and Siobhan say they are all for starting 529 accounts. They are hesitant to extend their mortgage and pay interest for seven more years—but then again, they are open to any solution that will help pay for college and make sure their soccer bills are covered. "We'll do anything that will keep the kids playing competitive soccer," says Siobhan, "and anything to help us sleep at night."

Read next: How to Get Your Student-Athlete Noticed by Colleges