The Right Way to Tap Income in Retirement

Over the past four decades, Ken Musolf, 63, has carefully plotted out an investment strategy for him and his wife, Jeanne, 59. His financial acumen has helped the couple accumulate $1.1 million in retirement funds.

Though Ken retired in 2012 after 35 years as a construction electrician, he and Jeanne have yet to tap that nest egg. He gets three pensions and Social Security, totaling $48,840 a year; and until December, she had been earning $100,000 as a department manager at a hospital. But they’ll need to start drawing down soon: Jeanne is scaling back her hours and job duties in January and plans to retire in three to six years.

Ken admits to being at a loss on this next phase: How do they transition from saving to taking income? With a portfolio across seven accounts that’s 66% stocks, 30% bonds, and 4% in cash, he says, “our quandary is that we have a basketful of investments and want to consolidate them in a sensible allocation that allows for growth and safety.”

Their only debt is a $43,000 home-equity loan and a $26,000 car loan. So the Musolfs have been living very comfortably on $8,500 a month, leaving them room to make extra debt payments, give $600 a month to charity, and splurge on their three grandkids. And Jeanne has been saving 20% of her pay in her 403(b). As she starts her new job, her salary will drop to $65,000.

The Musolfs can absorb that pay reduction and avoid dipping into their retirement funds by cutting back on overpayments on their mortgage and car loan, says Kay Allen of Aspen Wealth Management in Colleyville, Texas. The bigger challenge will be managing Jeanne’s retirement—when to quit and when to take Social Security—to minimize the impact on their portfolio. Depending on their choices, the couple could need to withdraw from $35,000 to $80,000 a year, Allen says. “The Musolfs are doing well,” she notes, “but it’s critical that they handle this transition carefully.”

The Advice

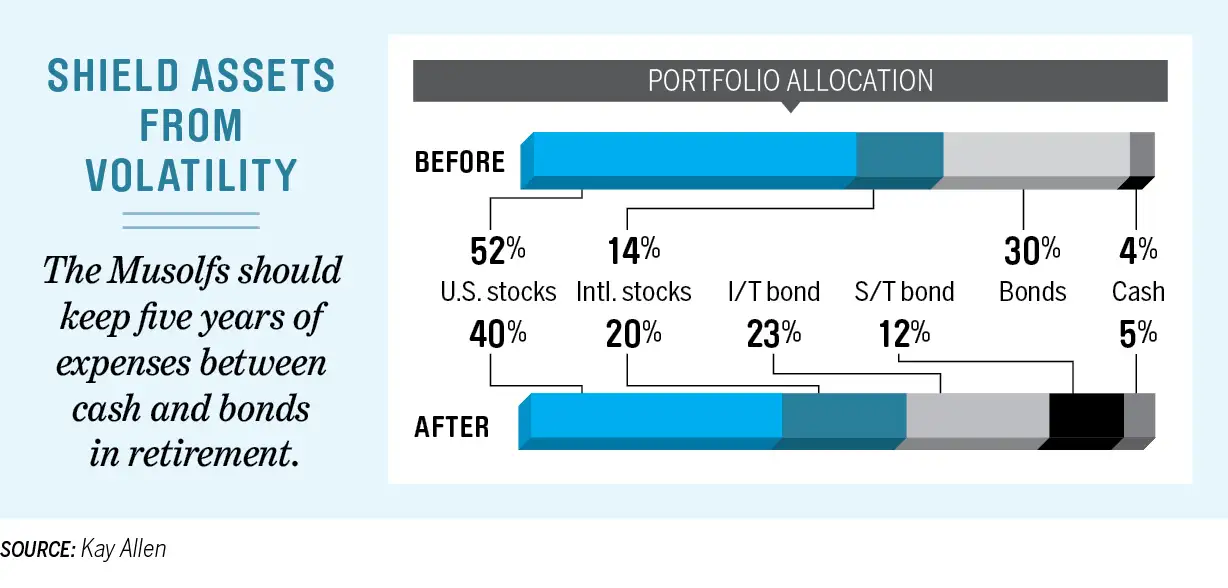

Reallocate to reduce risk: Ken can better manage their seven retirement accounts by consolidating them into four: one rollover IRA for each, Jeanne’s 403(b), and an IRA Jeanne inherited from her mother.

Next they should shift their allocation from a 66% stocks, 34% fixed-income mix to a 60%/40% mix. “This will enable them to better withstand market volatility,” says Allen. “At 60/40, they would have suffered a 22% loss during the Great Recession, requiring a 28% gain to catch up. With their current allocation, they’d have lost 30%, requiring a 43% gain. That is not something you want to experience in retirement!”

The mix she suggests (see illustration below) introduces shorter-term bonds for 12% of the portfolio via Vanguard Short Term Bond Index and 2% emerging-markets stock through Vanguard Emerging Market Index for diversification. Allen also suggests always keeping a year’s living expenses in cash and four years’ in bonds to cushion against market turmoil.

Tally up expenses: To determine an income strategy, the Musolfs needed to figure out their retirement budget. If she retires before Medicare kicks in at 65, Jeanne will have to pay for health insurance ($1,000 a month). Allen also wants the Musolfs to get long-term-care insurance ($500 a month), plus a Medigap policy for Ken once he turns 65 ($175 a month). Since the Musolfs want to travel more, Allen helped them come up with an annual vacation budget of $15,000. All told, the couple will have $146,000 in yearly inflation-adjusted expenses if Jeanne retires at 62, or $127,000 if she waits till 65.

Strategize withdrawals and Social Security together: Normally, retirees are advised to draw down at a rate of no more than 4% the first year, adjusting only for inflation annually, for the best chances of portfolio longevity. But if Jeanne retires at 62 and doesn’t take Social Security right away, the couple will need to replace $85,000 in income, for a whopping 7.6% withdrawal.

So if Jeanne does want to retire on the early end, Allen suggests she take a check from the government immediately. The couple would then initially have to draw 5.5% to get the $61,000 they’d need. But that’s okay, says Allen—three years later Jeanne qualifies for Medicare and won’t need health insurance, so their withdrawal rate will fall to 3.4%.

This way their money should last at least to their life expectancies, with some left for heirs. “Jeanne is concerned about retiring—she wants to know if she really can do it,” says Allen. “If they follow these steps, the answer will definitely be yes.”

Read more Retirement Money Makeovers:

Married 20-somethings With $135,000 in Debt

Freelancers With a Toddler, No Plan, and No Cash to Spare

30 Years Old, and Already Falling Behind

Read next: Why You Should Think Twice Before Choosing a Roth IRA or Roth 401(k)