3 Ways College Financial Aid Letters Can Confuse Families — and What to Do About It

Good news: your teen got into college! Bad news: now comes the heavy lifting of analyzing financial aid offers.

Every year, colleges send out financial aid offers after letters of admission. For many families, it’s the first time they’ll get a true, individualized price for attendance. But while these offers contain important numbers, they’re full of jargon-y terms that sound like they belong in a back office.

You’re not alone in feeling confused and possibly misled. Colleges don’t present financial information in a uniform way, which makes comparing costs across multiple schools a challenge. Some colleges don’t even include important information like tuition, housing and meals, says Rachel Fishman, deputy director for research with the education policy program at New America. That leaves families to figure out on their own the details of what could be one of the biggest purchases they’ll ever make.

Here’s why financial aid letters are so frustrating — and what to do to make them clearer.

Many financial aid offers combine all aid and use confusing terms

One of the first challenges families face when reviewing financial aid offers is trying to parse through unfamiliar vocabulary. In a 2018 report by New America and nonprofit organization uAspire, researchers found that 70% of the offers they analyzed grouped all the types of financial aid together and didn’t explain the differences.

The problem is, not all aid is created equal. Scholarships and grants (aka gift aid) don’t have to be repaid, while loans must be paid back. Work-study, the federal program that funds on-campus jobs, isn’t guaranteed and doesn’t help you pay the fall bill. Parent PLUS loans are more expensive, and riskier, than student loans. Combining them all into a single number creates a misleading impression, Fishman says. The final cost of the college appears more affordable than it is.

Confusing financial aid terms also trip up families every year because they’re inconsistent across offers. A good letter, therefore, will define the terminology so families can understand the pros and cons of different types of aid and can compare aid offers from different colleges.

“A good letter clearly separates out the aid by type and uses terminology that students can understand,” says Brendan Williams, senior director of consulting at uAspire.

The offers may leave out cost of attendance

Even if a scholarship or grant looks generous, you can’t tell how it affects your bottom line unless you know cost of attendance first. A full cost of attendance includes tuition, housing and meals, mandatory fees, books, personal expenses, and transportation.

“A $10,000 scholarship or grant has a much different impact on a college that costs $20,000 than one that costs $60,000,” Williams says. “It’s really important to know those starting costs.”

Adding to the confusion, colleges often combine costs in different ways. Some list direct costs (tuition, fees, housing and meals) and indirect costs (personal expenses, books, and transportation) together. Others separate them out.

“How price is displayed is confusing,” Fishman says. It’s helpful to know all the costs, but it’s more helpful to see these costs broken out. Families need to know the firm tuition and room and board costs separate from the “squishier” indirect costs of transportation and personal costs, Fishman says. That’s because those variable costs may not be the same for every family.

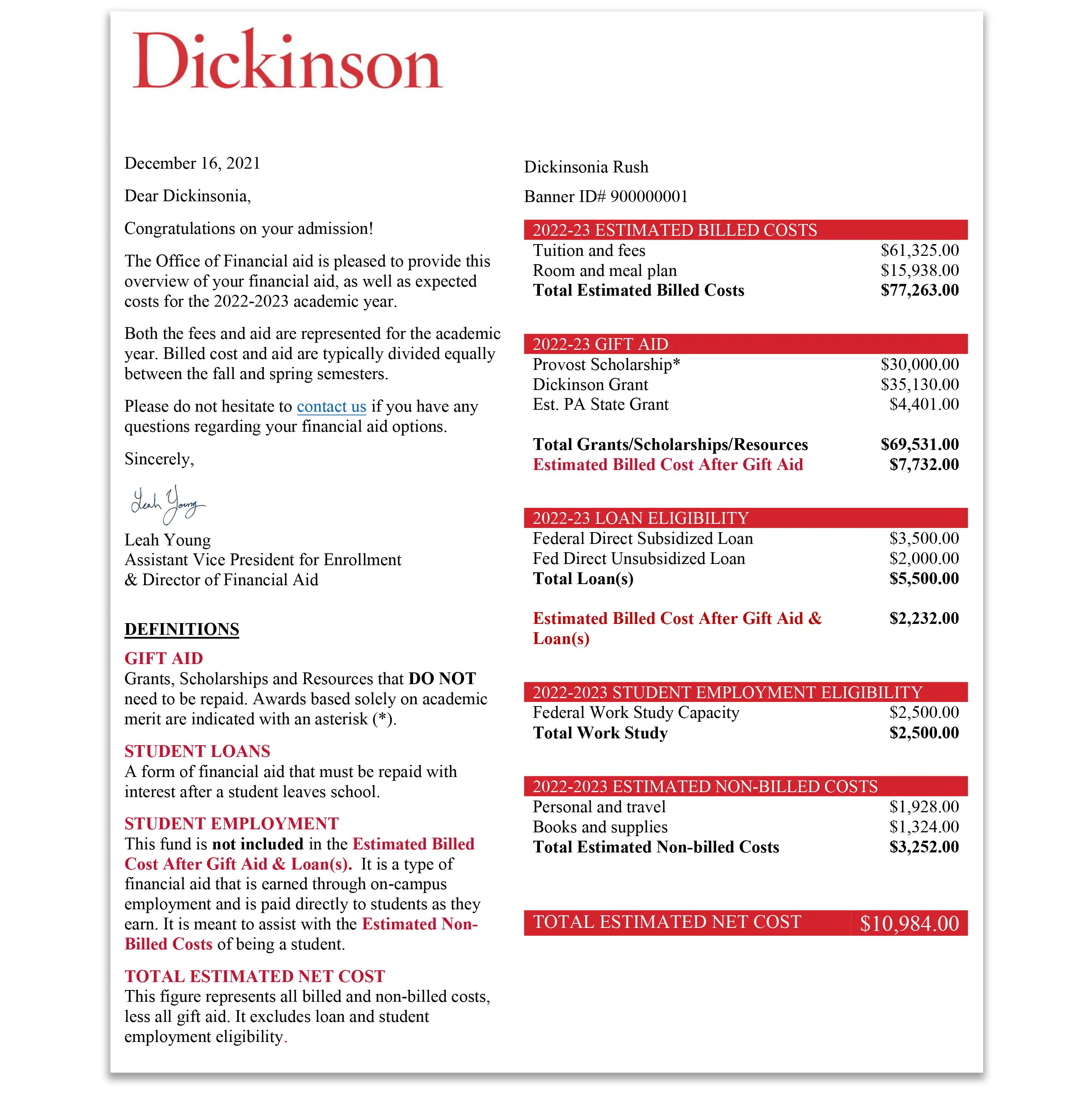

Some colleges are moving to make their offers and bottom line costs for families more transparent. At Dickinson College, a new format released this spring includes definitions alongside an outline of the billed, or direct, costs after gift, plus an estimate of the indirect costs, says Leah Young, assistant vice president for enrollment and director of financial aid. At the bottom, it lists a “net cost” for the family that combines all the expenses minus the gift aid, with loans and work-study listed separately.

“When we went to our college financial advisory board, the feedback we got was families wanted to see net cost listed,” Young says.

Financial aid offers might not list your estimated family contribution

In fact, financial aid offers probably won’t include your estimated family contribution, but knowing it is useful. Your estimate family contribution, or EFC, is the number on your FAFSA student aid report posted as a string of numbers (for example: 010000 = $10,000). The EFC isn’t the amount you’ll pay. It’s a measure of the aid you may qualify for — federal and non-federal — including Pell grant, state need-based grant, institutional grant, subsidized loan and work-study.

If your EFC is $15,000, then a $30,000 scholarship at a $78,000 college doesn’t come close to meeting your need. Most colleges don’t meet full financial need, however, leaving many families with funding gaps.

“If the college expects you to pay a lot more than your EFC, then you know it’s a raw deal,” Williams says.

Determine a college’s net cost: Understanding the overall cost of a particular college is important, but first, determine if you can handle the direct costs. If you can’t afford tuition, housing and meals after scholarships, grants, and student loans have been applied, the variable costs will be out of reach, too, Williams says.

If they’re not included in the letter, add up current costs for tuition, housing, meal plan and fees listed on the college website. If they are included, compare housing and meal costs (aka “room and board”) to other options on the website. Some residence halls may be more expensive to live in than others and many colleges offer different tiers of meal plans, so that’s one area you may be able to cut costs. “I’ve seen rooms on a campus that can be $5k difference in cost,” Williams says.

Next, you essentially want to follow Dickinson College’s new format: Once you have a fixed number for direct costs, subtract the grants and scholarships from that figure. That’s your net cost without loans.

Then, subtract federal student loans for a second total. That’s the cost to you after student borrowing. In other words, that’s the price you’ll have to pay out of pocket, either through savings, current income or additional borrowing, like private student loans or parent loans.

Analyze indirect costs separately: Since these costs are fluid for each family, they are worth considering as a separate category, experts say. For example, if you live a short drive from a particular campus, then you can subtract that $2,000 estimate for travel. Your student may be able to cover personal costs and books with summer savings, a part-time job or work-study. Leftover grants and scholarships can be used, but often that money doesn’t even cover all the direct costs.

Consult a dictionary: Don’t know the difference between a “subsidized” and “unsubsidized” loan? Never heard of work-study? You don’t want to be guessing when it comes to figuring out how much you’ll owe. If you have an offer in hand that doesn’t explain terms, use uAspire’s dictionary of terms or StudentAid.gov’s searchable glossary to understand it.

Compare colleges’ costs, apples to apples: Create a spreadsheet to compare the net cost of different colleges side by side. Some financial aid letters will make this information easier to find than others. You may have to dig around on the college website.

To compare costs, Young recommends using a worksheet created by the National Association of Student Financial Aid Administrators. Williams recommends creating a free account with uAspire to use its cost calculator. With either, you can list colleges’ costs side by side and generate estimates before and after loans.

Understand multi-year costs and borrowing: Once you’ve sorted out your costs for the first year, then you need to think about the other three (or more) years before committing to a college.

“Even if you can figure out how to pay, say, $10k this year, can you pay it next year, the year after, and the year after?” Williams says. Confirm that scholarships and grants are renewable. To understand what student borrowing means after graduation, tally up four years of borrowing and then map out the monthly bills, including interest, over a standard 10-year repayment plan. (You can use a loan calculator like this one to help.)

Explore parent PLUS loans separately: Some financial aid letters include parent PLUS loans as aid and may even list the final cost to you as $0 by applying parent loans, but these loans shouldn’t be part of the math. Eligibility to borrow is based on your credit history, so they aren’t a guaranteed source of funding as student loans are. Figure out the cost without parent borrowing first. Then think about whether you can afford monthly payments if you were to borrow the rest (or part of it) in parent loans.

Contact the financial aid office: If you need help understanding an offer, the college’s financial aid office can guide you, Young says. Also, if your financial situation has changed since you filed the FAFSA, be sure to submit a financial appeal. “Don’t wait until you get an offer — do it now,” Williams says.

This story has been updated to correct the spelling of Brendan Williams' name.

More from Money:

More Colleges Are Promising to Help Pay the Student Loans of Low-Earning Graduates

Parents Can Qualify for Student Loan Forgiveness, Too. Here's How