Coping With the Costs of Dementia: The Early Stage

This is the first of a three-part series on coping with aging's costliest challenge. Read part two, on dealing with the middle stages, and part three, on preparing for the final stages.

Throughout their 39-year marriage, Dick and Helen Pell have shared a love of the theater. And it was in a theater that Dick first noticed something wrong.

Rehearsing a skit in an amateur production four years ago, Helen had trouble remembering her lines. Soon she was asking Dick the same questions repeatedly. He took her to a doctor, who diagnosed Helen with dementia.

Today Dick, 82, and Helen, 79, still go to the theater. But Helen doesn't act. In their one-story home she gets lost looking for the bathroom. She doesn't know how to use a toaster, or even a light switch. "I get very sad when I realize I am losing my gal," says Dick. "And it gets more apparent every day."

Also apparent are the mounting expenses they face. Right now Dick is spending $255 a week for 15 hours of help from a home care aide. A nursing home stay, which Helen is likely to need someday, will cost about $6,000 a month. Says Dick: "You don't have to be a genius to see that we'll run out of money, depending on how long Helen will need care."

If you are one of the estimated 15 million Americans caring for someone with dementia, you know that it's a uniquely devastating disease. Dementia—the most common form is Alzheimer's—robs you of the person you love. It attacks memory, personality, language, and physical abilities. It can last for years, even decades. And it has no cure.

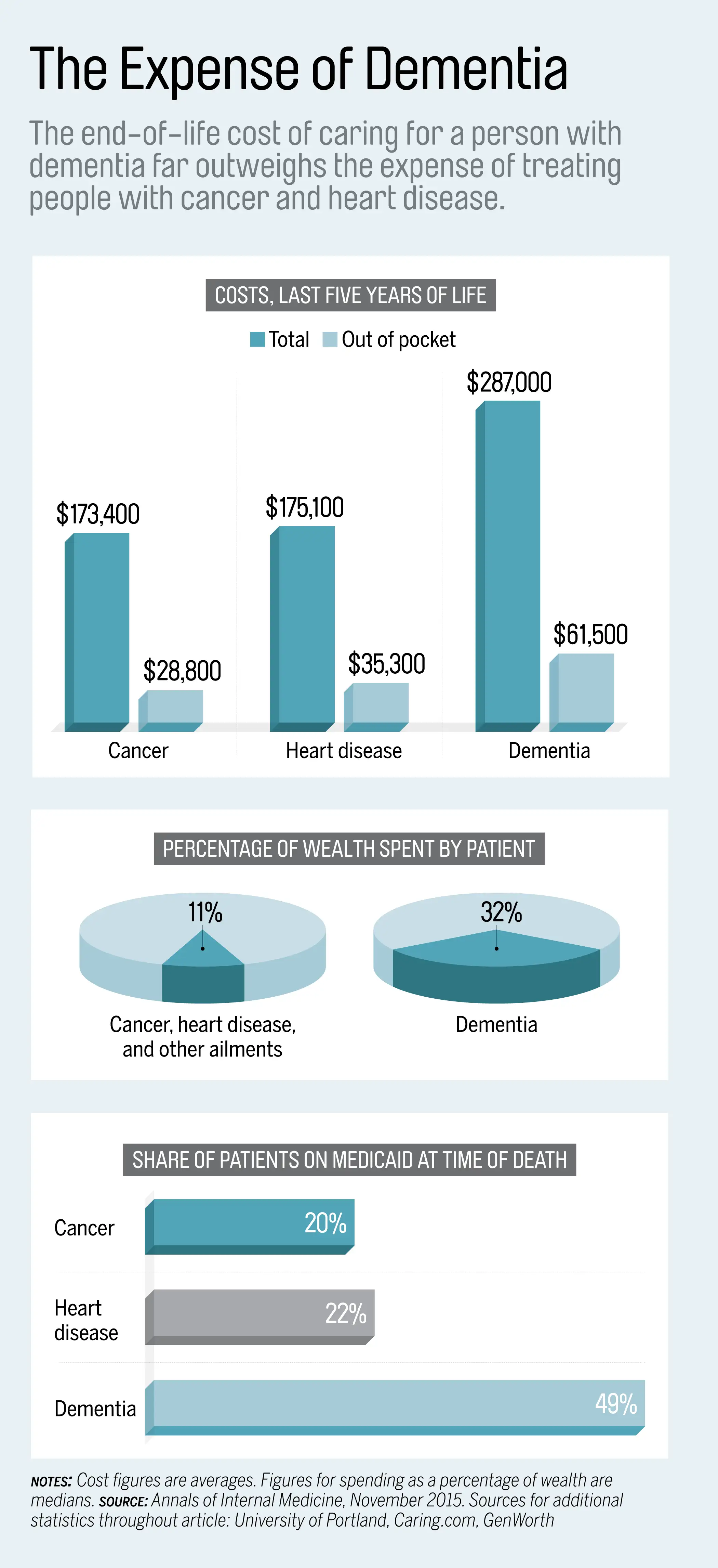

The financial toll can be nearly as large as the personal loss. Over the last five years of life, the average out-of-pocket cost of care for dementia patients totaled $61,500—81% more than for people without dementia—according to a new study in the Annals of Internal Medicine. Nearly half of the dementia patients ended up on Medicaid, the government health care program for impoverished Americans, compared to about 20% of patients suffering from heart disease or cancer.

Driving the cost aren't drugs or treatments, but the years of care necessary to get a person safely through life's everyday activities. Medicare, the primary health insurance for people 65 and older, doesn't cover that long-term nonmedical care. "The burden is on families to figure out how to pay for it," says Amy Kelley, lead author of the dementia study.

In this series of stories, you'll find detailed guidance on how to address the financial challenges of caring for a parent or spouse with dementia—the most important steps you can take in each of the three major phases of the disease. You'll also meet three families coping with the economics of dementia care and getting advice from financial professionals.

Dementia comes on gradually, so you can easily miss the first signs of it in someone you love, especially if you live with that person or see him or her on a regular basis.

That's partly because the early symptoms of dementia are often confused with the "senior moments" that naturally come with aging. It's also because the condition can be so frightening. "All too often, I've seen denial by the spouse, the family, or the person themselves," says Charles J. Fuschillo Jr., CEO of the Alzheimer's Foundation of America.

In this early stage of dementia, which lasts an average of two years, your out-of-pocket costs won't be burdensome. But you'll need to plan for more expensive care later on, and move quickly, since your husband, wife, or parent has a limited window to participate in financial decisions and sign any necessary legal documents before cognitive abilities fade. "When people don't recognize dementia earlier," says Fuschillo, "it costs you more in the end."

Christopher Churchill

Christopher Churchill

Know what is not normal aging

Be on the lookout for subtle but distinct differences from typical signs of aging, says Ruth Drew, director of family and information services for the Alzheimer's Association. Forgetting names or appointments isn't a big deal. More alarming is asking the same questions over and over or forgetting how to do familiar tasks like preparing a favorite recipe. You might also notice your parent or spouse misplacing things that turn up later in unusual places, like a phone in the refrigerator. (Visit alz.org for more tip-offs.) If the person you're concerned about doesn't live close by, enlist friends and neighbors to alert you to any troubling incidents, advises Kevin Jameson, president of the Dementia Society.

Add a doctor to the mix... gently

Bringing up the subject of dementia is an emotionally loaded conversation, and you don't want to put your loved one on the defensive. Pick a time when the person is relaxed. Start with a general question like, "How's your health? What has the doctor been saying?" Then raise your specific concerns. Andy Cohen, CEO of the caregiving information website Caring.com, suggests filtering your conversation through your own thoughts and feelings, along the lines of "I've noticed some behavior changes in you, I'm concerned, and it would make me feel better if you checked in with your doctor." A precipitating event—say, getting lost or bouncing checks—will make it hard to dismiss the problem, says Jameson, but if your loved one gets defensive, enlist a neutral third party, like a trusted friend, to bring up the issue. Offer to make the doctor's appointment and go along.

Appoint key decision-makers

Once you have a formal diagnosis in hand, ask for a family meeting to figure out who will be the point person, or persons, for managing your loved one's condition. As the dementia progresses, dozens of decisions will need to be made about care, housing, and finances—decisions that Dad, say, will be increasingly unable to make alone. Talk it through: Who lives the closest? Who has the most flexible schedule? Who is most comfortable with handling financial matters? Whoever ends up managing Dad's finances doesn't have to be the same person taking the lead on health care, but if it isn't, the two of them should be people who get along well enough to work together.

At the same time, sort out what will be needed in terms of relatives' money and time, and reach an agreement about who can contribute what. Even a long-distance relative can be of assistance by sending money or taking on tasks like paying bills online or handling taxes. "In the beginning the biggest cost is time and stress," says Jameson. "But those incremental costs can start to snowball quickly, so you need to always be thinking about the next steps."

Gather the paperwork

Along with a will, you'll need to have at least two key documents, says Shirley B. Whitenack, a lawyer and the president of the National Academy of Elder Law Attorneys (NAELA): a durable power of attorney, authorizing a person to make financial decisions for your family member, and a health care proxy, appointing someone to make medical decisions.

This, too, can be a tough subject to broach with a parent. Long-held roles are reversing: Now you're the one caring for Mom. Losing control can be scary and embarrassing for her, so make the conversation about you. You might say that you're getting your medical and financial paperwork together, so maybe she should too. Or you can say that you're worried and you'd feel a lot better if this paperwork were in place. You can draft these documents with the help of a local certified elder-care attorney who understands the relevant state laws and regulations. Start your search for a lawyer at the websites for NAELA and the National Elder Law Foundation.

Take a financial inventory

It's important to get a handle on all the assets your family member has available for funding care, starting with money in the bank, investments, pensions, and Social Security. You also want to know if he or she has a long-term-care insurance policy in force. (Only 7% of the population does, and after a diagnosis of dementia it's too late to apply for one.) You'll also want to know the equity in the home, in case you might want to tap it via a reverse mortgage or sale. Such an inventory may not be easy; when Theresa Von Vreckin took over her father's finances, his investments turned out to be in more than a dozen different accounts. And your parent may not want to share this information with you for privacy reasons. If so, offer to make an appointment with a financial planner who can help sort things out. But that planner should get Dad's okay that the adviser can get in touch with you if he is worried about Dad's cognitive abilities—an increasingly common practice among financial planners.

If it's your husband or wife who has been diagnosed with dementia, you might want to do what Dick Pell has done for Helen: set up a special-needs trust so that if you die first, your assets will be earmarked for your spouse's care. Again, consult an elder-care attorney.

Get ready for Medicaid

There's a substantial likelihood that your loved one may need to go on Medicaid for care: In the Annals of Internal Medicine study, for example, the share of dementia patients on Medicaid went from 21% to 49% during their last five years of life. You can start planning for that possibility now.

Medicaid, however, has strict rules limiting the assets a patient—and a patient's spouse—can own while qualifying for the program. One wealth-preserving tactic to keep in mind for now is for the patient to pay off any home mortgage. Because your primary residence is exempt for the purposes of determining Medicaid, that move will increase the amount of home equity you can tap later, if you end up needing those funds.

Another wealth-preservation tactic is to transfer assets of the person with dementia (again, plus the spouse's assets, if married) to someone else. There's a catch, though: Medicaid has what is known as a five-year look-back rule. If the dementia patient transfers the assets and then applies for Medicaid within five years, the patient will be expected to pay for caregiving equal in value to those assets. So if your mother impulsively gives all of her money to her grandchildren to spend down assets—but then needs that money for care within five years—you and other family members are going to have to figure out how to replace that money so she can qualify for Medicaid.

Read next: Coping With the Costs of Dementia: The Middle Stage