Don't Let Divorce Derail Your Retirement

At any age, a divorce can set you back financially, but ending a marriage later in life poses an extra threat: derailing a previously on-track retirement. As is true with younger couples, a divorce is likely to leave you with higher living expenses, lower in-come, and less wealth. But if you're fiftysomething or older, you'll have a lot less time to amass more earnings to make up for what you've lost.

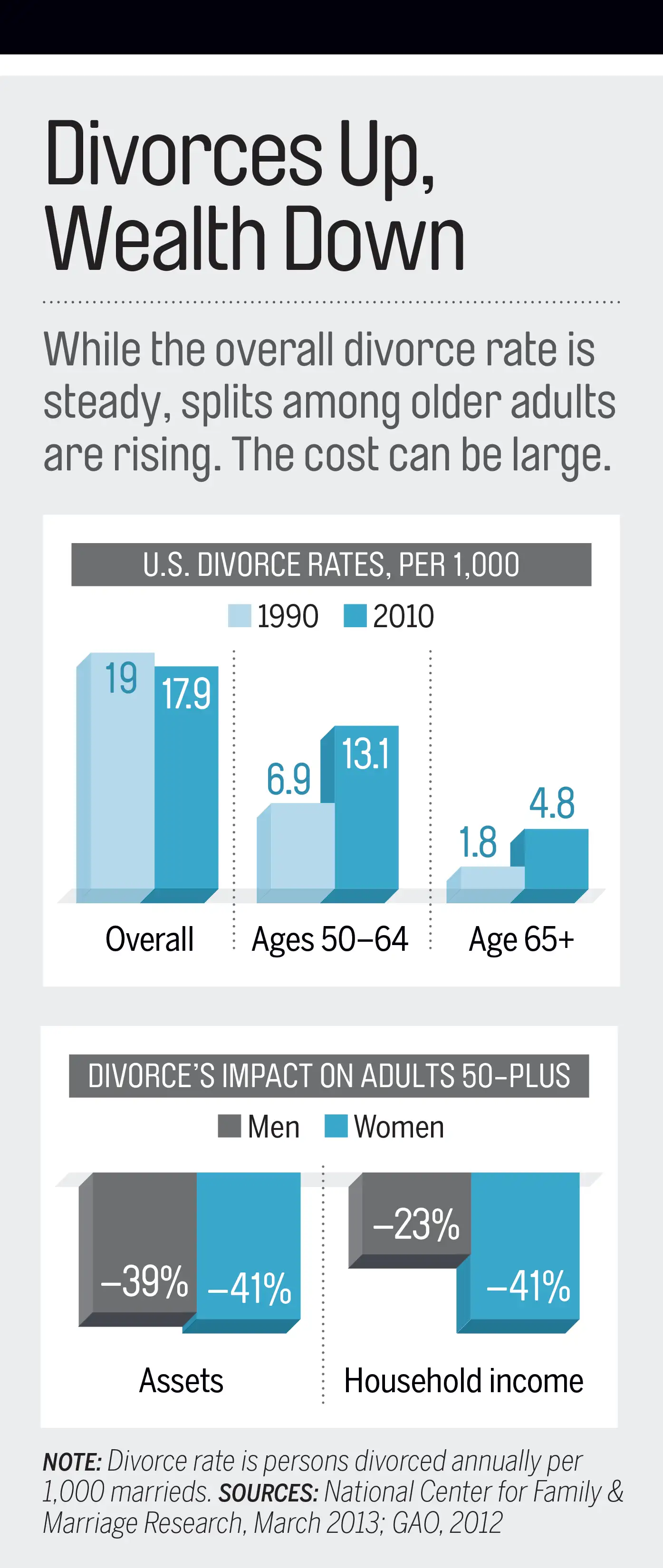

That challenge is on the rise. The divorce rate among couples 50 and older doubled from 1990 to 2010, while the overall rate stayed flat, according to a Bowling Green State University study.

Splitting up? Take these steps to protect your retirement finances.

Sell the house. After a post-50 divorce, household income, on average, drops 23% for men and nearly double that for women (see the chart). You'll need to recalibrate your spending to match that.

A painful but powerful tactic is to move to less costly quarters. Staying in the family homestead may furnish stability during a split's upheaval, but you'll lose a chance to boost your retirement income, says Jacqueline Roessler, a financial planner at Divorce Solutions in Southfield, Mich. If you cut your housing costs by $500 a month, for example, and get a 5% return on those savings over the next decade, you'll have $77,000 more for retirement. You can also use the money from a sale to build a larger, income-generating diversified portfolio. (You're at an age when, even if you were to stay married, you might downsize; sell now and you can split the sales costs with your ex.)

Use your extra cash to take advantage of catch-up contributions open to people 50 and older. You can put $24,000 a year in a 401(k) and $6,500 in an IRA.

Focus on income. You and your spouse are free to negotiate your own divorce terms. The goal: an equitable distribution of assets based on factors such as work records, earnings power, and the length of your marriage. (If you can't agree, a judge will decide. In 41 states, that equitable framework rules, while the rest tend to a 50-50 split.) With retirement so close, be single-minded about valuing financial assets in terms of the sustainable income they are likely to generate. Taxes count. A $500,000 401(k), where 100% of withdrawals are taxed at ordinary income rates, is probably worth much less than $500,000 in a taxable investment account, where only the gains are taxed (at advantageous rates), notes Tracy B. Stewart, a CPA in College Station, Texas, who specializes in divorce cases.

Factor in Social Security too. Once you're at least 62, you can opt for a benefit that's 50% of what your ex is due, if it's greater than your full benefit. (Your marriage must have lasted at least a decade, among other conditions.) "If one spouse is going to have a Social Security benefit that is double the other spouse's, that's an argument for using another asset to offset the lower payment," says Roessler.

Setting values on pensions, IRAs, insurance policies, and other assets—and figuring out your long-term financial needs—would be a mind-numbing challenge even if it weren't arising at a time of heated emotions. So hire a financial planner along with a lawyer, advises Janice Green, a family law attorney and the author of Divorce After 50. "Retirement planning and divorce negotiations go hand in hand when you are older," says Green. Financial professionals specially trained to work with divorcing spouses can be found on the website of the Institute for Divorce Financial Analysts.

Do the division. Your divorce decree merely states who gets what. You still have to make sure you receive the assets you're due. Dawdling is dangerous. If you are owed part of your spouse's 401(k), you can't control how it is invested—or whether your ex borrows from it—until the money is moved.

Read next: Keep a Divorce From Killing Your Finances

For each 401(k) or private-sector pension of your ex's that you have a claim on, you have to file a qualified domestic relations order (QDRO), a legal document that authorizes the transfer, which can run you $300 to $500 apiece. IRAs, public pensions, and military benefits each have specific paperwork.

Also, revisit estate documents and beneficiary designations. Even if an investment account's beneficiary does not change, says Green, you must "re-execute" those documents to reflect your divorce. Once that is done, you can focus on your new life knowing you've taken all the key steps to protect your retirement.