Making the Most of a Mighty Dollar

- Here's Why 2015 Will Be a Good Year for Stocks

- It's a Huge Day for the Stock Market. What You Need to Know About History's Longest Bull Market

- The Best Performing Stock of This Bull Market Is Up Almost 39,000% — and You've Probably Never Heard of It

- These Charts Show What's Wrong With the Stock Market This Year—and Where You Can Still Make Money

- Everything Investors Got Wrong About the Trump Presidency, Explained

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

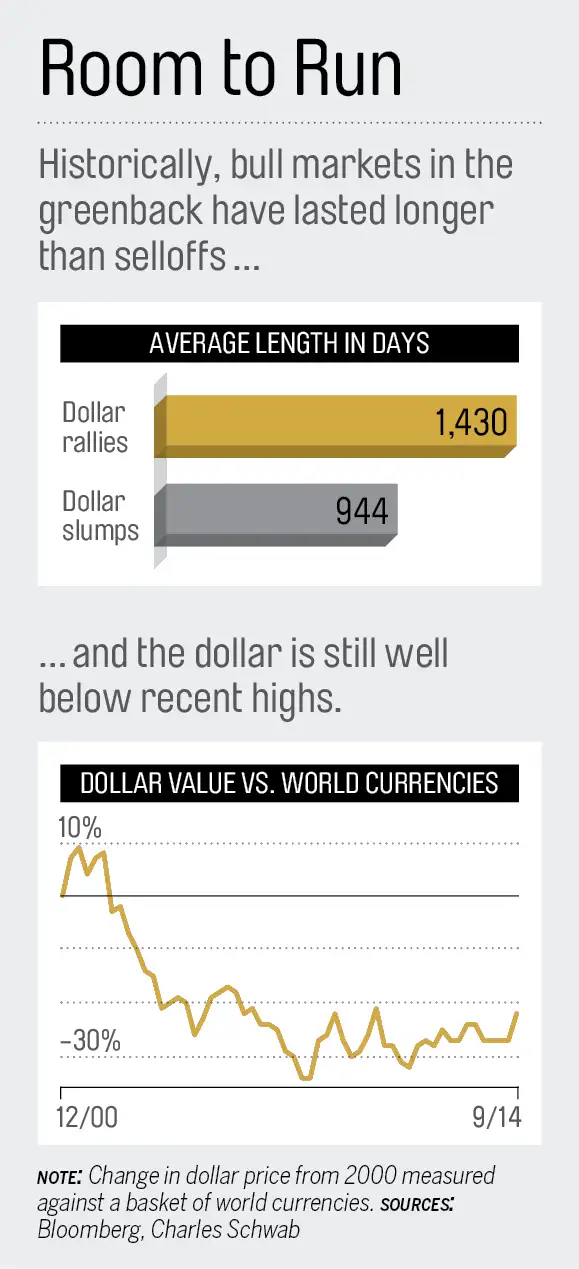

After getting pushed around for much of the 2000s, the once-wimpy buck is fighting back. The dollar has gained nearly 20% over the past 3½ years, compared with an index of global currencies. It’s now at multiyear highs against the euro and yen.

This is good news because it represents a global vote of confidence in our economy. Investors worldwide snap up bucks when they want to buy things denominated in our currency—including U.S. bonds, stocks, and other assets. The dollar’s current rally got going in 2011 and 2012, as the U.S. economy fitfully grew while Europe and Japan slipped into double-dip recessions. That has made America look like a better relative investment, says Brian McMahon, chief investment officer at Thornburg Investment Management.

And as our recovery gains strength, interest rates should nudge higher, making bonds more attractive to yield-seeking overseas investors. So the dollar could keep bulking up from here.

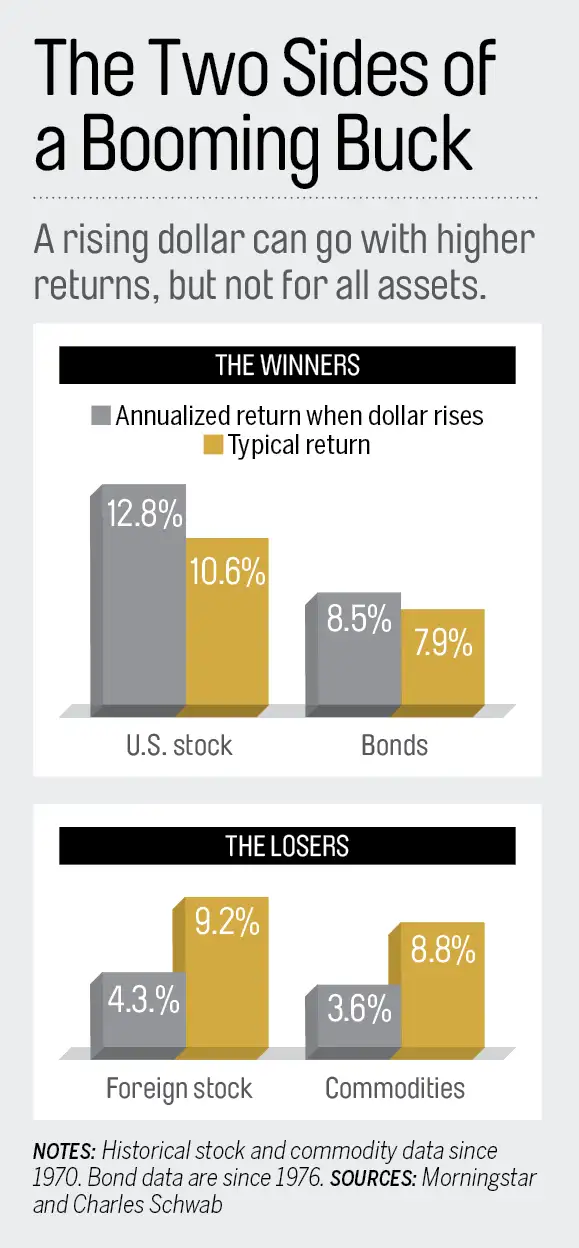

Dollar rallies have historically corresponded to a strong stock market, but “in any shift in a currency, there are going to be winners and losers,” says Liz Ann Sonders, chief investment strategist for Charles Schwab. You probably have some of both in your portfolio. So here’s a rundown of how things are likely to play out, asset by asset:

U.S. STOCKS

Bet on the American consumer … In part, the dollar boom is a reflection of the same trends that are benefiting any stock that’s sensitive to an improving domestic economy. GDP grew at an impressive rate

of 4.6% in the second quarter.

Yet the dollar isn’t just a mirror of U.S. strength. Its rise will also help lift some parts of the -economy. “The big winner is the U.S. consumer,” says Mark Freeman, chief investment officer for Westwood Holdings Group. One reason: A rise in the dollar tends to correspond to a drop in oil and other commodity prices. Since April 2011, the price of a barrel of crude oil has fallen by around 25%. Lower costs for energy leave consumers with more money to spend on other things.

Transportation stocks, including rail, freight, and airlines, benefit both from lower fuel costs and from consumer demand—more buying means more stuff is being shipped. A simple way to get exposure to the biggest names in these groups is through an index fund like iShares Transportation Average ETF.

… But not on U.S manufacturers. You can make room for a transportation-oriented ETF by lightening up on your exposure to U.S.-based multinationals.

For years, when the U.S. economy was sluggish, it made sense to bet on firms, such as Procter & Gamble , that sell a lot to fast-growing markets abroad.

But a strong dollar will make it harder for such companies to compete with foreign rivals outside the U.S. This is why large exporters such as Ford and tobacco giant Philip Morris International have cut expectations for profits this year. Industrial companies were once expected to grow earnings 24% in the third quarter. Now the forecast is 8% growth, according to S&P Capital IQ.

Be careful with dividends. In recent years, with interest rates very low, investors have turned to high-dividend-paying stocks to boost their income. So those stocks have boomed. But the rising dollar is signaling a steady shift to higher rates, says Freeman of Westwood Holdings.

Here’s why: Although U.S. bond yields remain low, they are significantly higher than what investors are now getting in many overseas markets. (Ten-year German bonds pay 0.9%, vs. 2.4% for Treasuries.) And the recent momentum in the dollar suggests traders expect U.S. bond yields to stay attractive—a reasonable bet given that the Federal Reserve is signaling that it will start gradually raising rates in 2015.

Better bond yields will be bad news for some high-income stocks, since many investors will switch from stocks that are attractive mainly because of their dividend checks. Income investors should go beyond just grabbing the highest yields and shift to companies that can also increase their payout steadily.

Susan Kempler, a portfolio manager at TIAA-CREF, points to Apple , which yields just 1.8% but sits on more than $160 billion in excess cash. Such companies can be found in T. Rowe Price Dividend Growth Fund, which has beaten nearly 80% of its peers over the past decade.

FOREIGN STOCKS

Don’t give up …International investing tends to grow in popularity when the dollar sinks. That’s because when the buck loses value, Americans can make money on international stocks simply on the currency exchange. When the dollar rises, on the other hand, that’s a drag on returns.

So Americans’ attraction to foreign investing is likely to cool, says Scott Clemons, chief investment strategist at Brown Brothers Harriman. Yet this is precisely why you shouldn’t turn your back on international equities now.

For one thing, valuations abroad, especially for European shares, are low. Doug Ramsey, chief investment officer for the Leuthold Group, notes that U.S. stocks have historically been cheap—as measured by price relative to past earnings—compared with global shares. Recently, though, U.S. stocks have jumped to a 20% premium. On valuations alone, he says, “foreign equities should produce total returns of about two percentage points annualized above the U.S. over a seven-to-10-year horizon.”

You can gain European exposure through a broad-based fund that invests globally (so you’re still diversified) but with big positions in Europe. An example is Oakmark International, which is on our Money 50 recommended list of funds. The fund keeps more than 75% of its assets in European equities.

… But tread lightly in the emerging markets. As the dollar strengthens, expect rockiness in emerging markets as global investors reassess their portfolios.

Once rates start to climb in the U.S., says Kate Warne, investment strategist for Edward Jones, investors will shift to a more conservative mode, since they won’t have to take as much risk to earn a return. Many are likely to pull money away from emerging-markets investments. Warne says her company recommends that investors keep only 5% of their total portfolio in emerging-markets equities.

BONDS

Don’t assume the worst …

One cause of the strong dollar—-expected rising rates—may have bond investors shivering. When rates rise, the value of older bonds in your fixed-income funds will fall, reducing your total return.

But take a breath. A gradual rise wouldn’t be a catastrophe if you hold conservative short- and intermediate-term bond funds. Meanwhile, a strong dollar also brings some good news for fixed-income investors. Inflation, a major enemy to bond investors, is held in check by the rising dollar, thanks to lower commodity prices.

… But hedge your foreign exposure. As with stocks, American investors have used foreign bonds as a way to profit from a weak dollar. Indeed, the currency effect added about two percentage points to foreign bond fund total returns since 1985, according to the Vanguard fund group. But a strengthening dollar going forward would mean the currency trade hurts, not helps.

You can still maintain foreign fixed-income exposure for diversification, but in a way that hedges your bets. A few funds lessen the impact of currency shifts by essentially buying dollars in the open market every time they buy

a foreign bond. One solid option is Vanguard Total International Bond Index, which charges just 0.23% of assets a year. Sometimes you are better off playing just the investment and not the currency it’s wrapped in.