Don't Be Fooled by Credit Score Inflation

Have a 900 credit score? Before you lord it over your friend who can only claim a mere 750, make sure you're comparing apples to apples.

In the September issue of Money, I wrote "The quest for the perfect credit score," which chronicled the efforts of three people reaching for a perfect 850 credit score.

Since then, I've received letters from several readers who seem to have these credit score superstars beat. One wrote, "I was a little amused by the...individuals with credit scores in the range of 806 to 813...The last time I checked, my Experian score was 924, with no special effort on my part."

Comments like this one underscore a larger problem: the confusion around credit scores and scoring models.

In this story, we looked at each user's FICO score, which operates on a 300- to 850-point scale. But there are competing scoring models on the market with different scales, such as the relatively new VantageScore, a creation of the three major credit-reporting companies, Equifax, Experian and TransUnion. The VantageScore scale starts higher than FICO's and ends higher, too, ranging from 501 to 990. We stick with the FICO score (for my story, we used Equifax's version) because the vast majority of lenders still use that model and its 850-point scale.

So how can you compare apples to apples when it comes to scores from different models? Unfortunately, no magical, publicly available website exists to convert your score from one system to another. Part of the problem is that while each scoring model is designed to measure roughly the same thing — how much risk a company would take by lending you money — each uses different inputs and formulas to get the job done. It's like a high school senior trying to use his score on one college admissions test, the ACT, to figure out his score on the SAT. The only way to get a definitive answer is to take the other test.

That being said, there are ways to get an approximation of your credit score under different models.

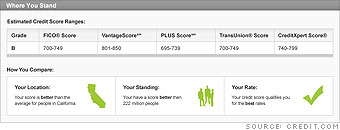

One option is to get a free "credit report card" from Credit.com, a company that offers various credit- and credit-card-related services online. Plug in your social security number and other identifying information, and you'll get — along with a general assessment of your credit profile — an estimate of the range in which your credit score falls under each of five different scoring systems, including FICO, VantageScore and Experian's PLUS Score. The highest number on the PLUS Score scale, by the way, happens to be 830, so the reader who mentioned a 924 Experian score was probably referring to a VantageScore number.

If you already have a specific score under one model and you're looking for the rough equivalent in another, we at the magazine have cobbled together a back-of-the-envelope converter — for FICO and VantageScore, at least. It's based on certain materials released by each of the companies — a blog post in FICO's case and a white paper in VantageScore's. Each contains a snapshot, as of two or three years ago, indicating what percentage of the population was assigned to various credit-score ranges under its system. (I used more recent 2010 FICO numbers in my September story, but for this exercise we wanted something closer in time to the VantageScore data we had, dating from before the economic meltdown.)

Some of those ranges match up rather closely, as you can see above in our multicolored bar graph. For example, 25% of VantageScore credit ratings fell in its lowest range of scores, 501 to 639. Meanwhile, 24% of FICO scores fell between its minimum rating of 300 and 599. So it seems safe to say that a VantageScore of 639 is in the same ballpark as a FICO score of 599.

Using the same logic with FICO-VantageScore chart, our letter-writer's score of 924 is probably in the same neighborhood as a FICO score in the low 800s. That's no slouch score, but it's also not so wondrous that one could rub it in the face of the high scorers in my September article.

Whatever the validity of this conversion chart, the lesson here is to understand which model is being used when you're judging a credit score. Don't be misled by grade inflation.

And if you know your credit scores under different models, tell us about it in the comments section below.

Find Money on Facebook.