How Much Money Would You Need to Ditch Your Job—Forever?

The American Dream is traditionally defined by a climb up the socioeconomic ladder to a comfortable middle-class life: a small business built from scratch, a house in the suburbs, a two-car garage, and the first generation of college-educated kids.

But another type of American Dream has now developed: The freedom to upturn your desk, give your boss the finger, and retire on the spot—without making a lifestyle sacrifice, of course.

In some circles, the wealth required to burn any bridge you want has a name: “f--k you money.” That's because, well, backed by the First Amendment and a large fortune, you can yell that without consequences to pretty much anyone, save for a judge, a plumber, or a tax assessor.

The term pops up often in popular culture—for example, memorably employed by the actor John Goodman in the 2014 film The Gambler (audio NSFW, unsurprisingly).

For many people, f--k you money is the essence of success. “[If] you have, as performers will call it, ‘f--k you’ money,” Johnny Carson once said, “all that means is that I don’t have to do what I don’t want to do.” Having f--k you money is the logical extreme of a certain conception of American freedom: complete ownership over yourself and your time. The freedom to retire at any time is a far more flexible proposition than owning your own business.

Where did the phrase come from?

Like most vulgar expressions of the more decorous—at least publicly—pre-Internet era, the phrase's origin is difficult to ascertain. Google Books, which searches an extensive digitized catalog, shows a printed debut in 1971 in The Show Business Nobody Knows, a book by Earl Wilson, a gossip columnist who was known for exposing JFK’s broad interpretation of his marital vows. Wilson, like Johnny Carson, pegs its origin to showbiz and names perhaps the earliest adopter as none other than comedian Red Buttons.

The year after Wilson’s book was published, screenwriter William Froug (Gilligan’s Island and The Twilight Zone) found reason to include it in his own book, The Screenwriter Looks at the Screenwriter. Froug mentions his colleague Walter Newman's belief that “keeping his overhead to a minimum gains him the freedom that every writer the world over longs for. In Hollywood it's officially known as ‘F--k-You’ Money.”

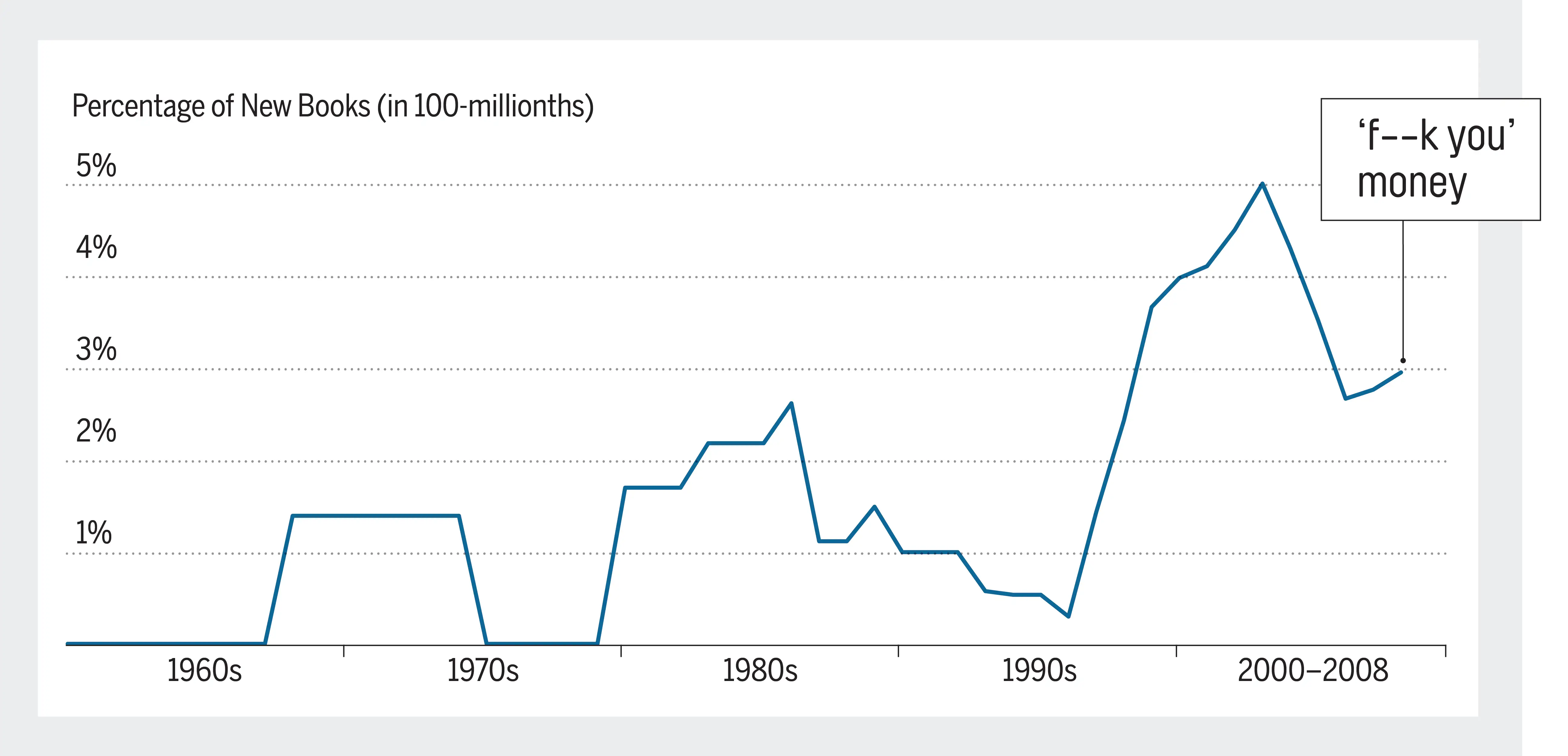

Though the phrase must have caught on quickly, it never achieved mainstream recognition. But that same year, a character in Gerald A. Browne's novel 11 Harrowhouse pegged it to a specific sum: $200,000 in a Swiss bank account. The phrase seemed to gain traction after that, at least in certain circles, according to Google’s Ngram Viewer.

The chart below, based on Google data, indicates the percentage of books published each year in which the expression appears.

The usage of “f--k you money” tracks the S&P 500 with an impressive degree of correlation. There’s the same boom in the mid-’80s before the drop around '87, and a steep and steady climb in the late '90s before a decline beginning in 2002. The relationship may be a coincidence. But at some point between Red Buttons and the Showtime show Billions (in which f--k you money has prominent placement), the term was co-opted by Wall Street and, to a lesser extent, Silicon Valley.

That makes sense. All three milieus have two major things in common: big egos and fast-growth fortunes.

It might not actually be that much money

To drop an f-bomb on an employer sounds like a luxury, but it might not be the long shot it seems.

To get a ballpark estimate of the money you'd need, multiply the annual expense of maintaining your preferred lifestyle by the number of years you're likely to live. Err on the long side so your later years won't be marred by poverty. For example, if you want to storm out of your office at 40 and plan on living another 50 years with $60,000 in annual walking-around money, simple arithmetic indicates you'll need $3 million. It's a ton, to be sure, but it's not Vanderbilt money.

For a more precise calculation, however, you have to account for inflation, which reduces your purchasing power over time. On the upside, you should also account for the money you could make by investing the nest egg you'll be tapping over your 50-year retirement. In this example, an investor taking only moderate risks in the market could get by with just $2.1 million and still have a 90% chance of making it to 90 without having to curb spending in the golden years, according to Vanguard's simple retirement nest egg calculator.

Cut a few luxuries, and even more is possible. If you can live on just $25,000, you’d just need $850,000 to quit at 40 and live until 90 in probable financial security.

Find your nest egg target

The calculator below will give you a rough estimate of how much you need—the default return of 2.5 percentage points over the inflation rate is a good starting place, based on a portfolio that's more conservative than a 50/50 bond/stock mix, which is already a fairly conservative approach. For a more in-depth picture of how a nest egg might grow, check out Vanguard's far more thorough retirement calculator. The company's tables of historic gains with different allocations are always an interesting read.

On mobile, thumb up on your screen to scroll down on the tool

Our tool avoids what the conventional wisdom of the past has dictated—the 4% rule. This is what author Lee Eisenberg used for a worksheet that purported to deliver what he called "the New York Number," a concept similar to "f--k you money," but for living in New York City. Quitting work at a younger age, however, means a longer retirement, and the traditional rules for a 25-year cookie-cutter retirement may not apply. (Even for 65-year-old retirees, there's considerable doubt as to whether it's actually a safe rule. Last year, retirement expert and professor Wade Pfau told the New York Times that "we are in uncharted waters" when it comes to the 4% rule.) It pays to be conservative about how much money you'll need.