These Sneaky Trusts Are Hiding in Your 401(k)

- 3 Easy Ways to Start Saving for Your Retirement in 2022

- Americans Think They'll Have Enough Money for Retirement. Most of Them Are Wrong

- The Father of the 401(k) Says This Is the Key to Retirement Today

- Your Old 401(k)s Could Be Costing You Thousands. Here's When and How to Consolidate

- The 401(k) Term That Confuses People the Most — and What It Really Means

There's a stealth investment vehicle that's making its way into more 401(k) plans: the collective investment trust (CIT). You might own one or more, especially if you work for a large company, and not even know it.

Also known as collective investment funds, these holdings are similar to mutual funds in owning baskets of securities. But they are open only to retirement plans and some other institutional investors, and they aren't subject to the same disclosure rules and other requirements as mutual funds. That leads to the primary attraction of CITs: lower fees.

While the trusts are not new—in fact, like mutual funds they've been around for many decades—they've been growing in popularity. Recent lawsuits filed by retirement-plan participants accusing companies of having excessive 401(k) fees have put a spotlight on what savers pay. Also, the onus on plans to lower fees has grown over the past decade owing to a requirement that plans disclose all fees to participants.

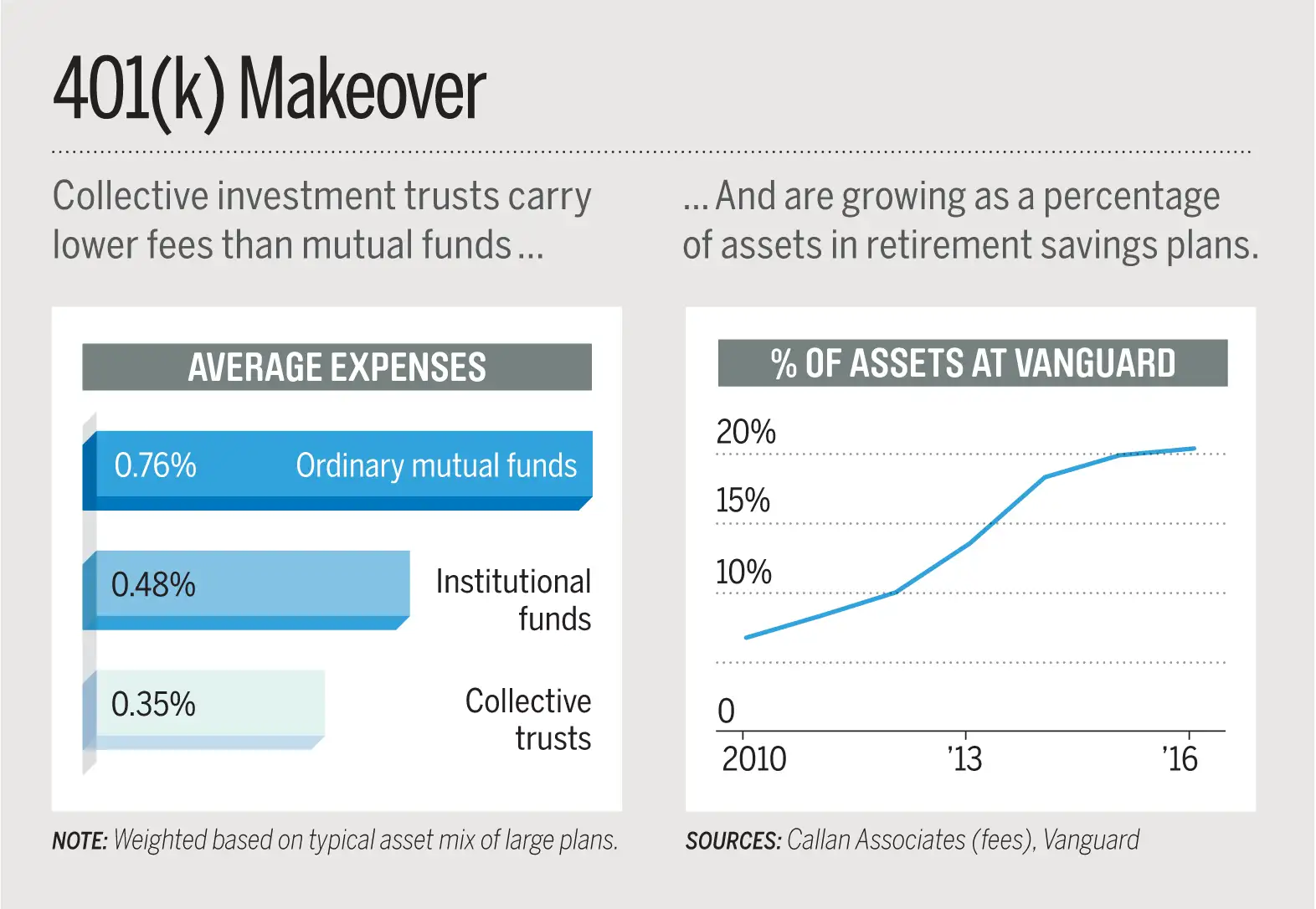

In 2016, 65% of larger 401(k) plans included at least one trust on its menu, vs. 48% in 2012, according to Lori Lucas, defined contribution practice leader at Callan Associates, an investment consulting firm. "The financial services industry has seen an increased use of trusts due to fee sensitivity," says Kevin Jestice, head of institutional investor services at Vanguard.

Here's what you need to know if you own a collective investment trust now, or may in the future:

How to Spot Them

The tip-off that some of the options in your 401(k) are CITs? On the list of investments, look for "Trust" or the abbreviated "Tr" in the name—and also the absence of a ticker symbol. Don't assume your investments are funds because you see the names of big fund companies like Vanguard and Fidelity; they are also big providers of CITs, typically through their own trust-company subsidiaries.

As investments, trusts "look and feel a lot like a mutual fund," Lucas says. For example, a trust could track the S&P 500 stock index, just like an index mutual fund. There are also target-date trusts: Some plans might offer the Vanguard Target Retirement 2030 Fund, and others, the Vanguard Target Retirement 2030 Trust. You can typically move money into or out of a trust daily, just as you can with the funds in a 401(k).

The Cost Savings vs. Funds

Some 401(k)s have trimmed their expenses by switching from ordinary mutual funds for individual investors to lower-cost institutional funds—and cut them again by switching to CITs. As seen in the graphic below, a typical mix of CITs in a large 401(k) plan might cost 0.35% of assets in annual fees, less than half the cost of ordinary mutual funds, according to Callan. A 0.35% expense ratio is equal to just $350 a year on a $100,000 balance.

The very cheapest institutional funds and CITs are far cheaper than the averages—under 0.1% or even under 0.05%, says Michael Miller, managing director of the PFE Group. Trusts are typically a hair cheaper than the funds.

Potential Drawbacks

Trusts can have a disadvantage when it comes to transparency and the ease of reviewing all of your investments in one place. "These aren't investments you'd generally see in the newspaper," says Bob Salerno, a senior vice president at Fidelity. You can't look them up on websites like Yahoo Finance either.

Instead, you'll have to log in to your account on the website of the financial company that administers your 401(k) plan. Much of the information you'll see on the trusts is likely to be similar to what is provided for the mutual funds in the plan. For instance, you will often be able to see how a trust has performed compared with an index benchmark or category average, says David Blanchett, head of retirement research for Morningstar.

Another downside to collective investment trusts is that it's harder to integrate them into online portfolio management tools. For example, Personal Capital offers free financial software that allows users to track investments held in multiple accounts and at various firms. The software automatically grabs data about the securities inside mutual funds, but for CITs the user would have to manually add a ticker symbol for an equivalent fund to use as a proxy, a spokeswoman says. Ditto for investors using Morningstar's portfolio tracking tool.

Similarly, portfolio management firm Betterment says it can't advise clients about the CITs inside their 401(k)s as it does about mutual fund holdings in those company plans.