The Secrets to Making a $1 Million Retirement Stash Last

More than three decades after the creation of the 401(k), this workplace plan has become the No. 1 way for Americans to save for retirement. And save they have. The average plan balance has hit a record high, and the number of million-dollar-plus 401(k)s has more than doubled since 2012.

In the first part of this four-part series, we laid out what you need to do to build a $1 million 401(k) plan. We also shared lessons from 401(k) millionaires in the making. In this second installment, you'll learn how to manage that enviable nest egg once you hit retirement.

Dial Back On Stocks

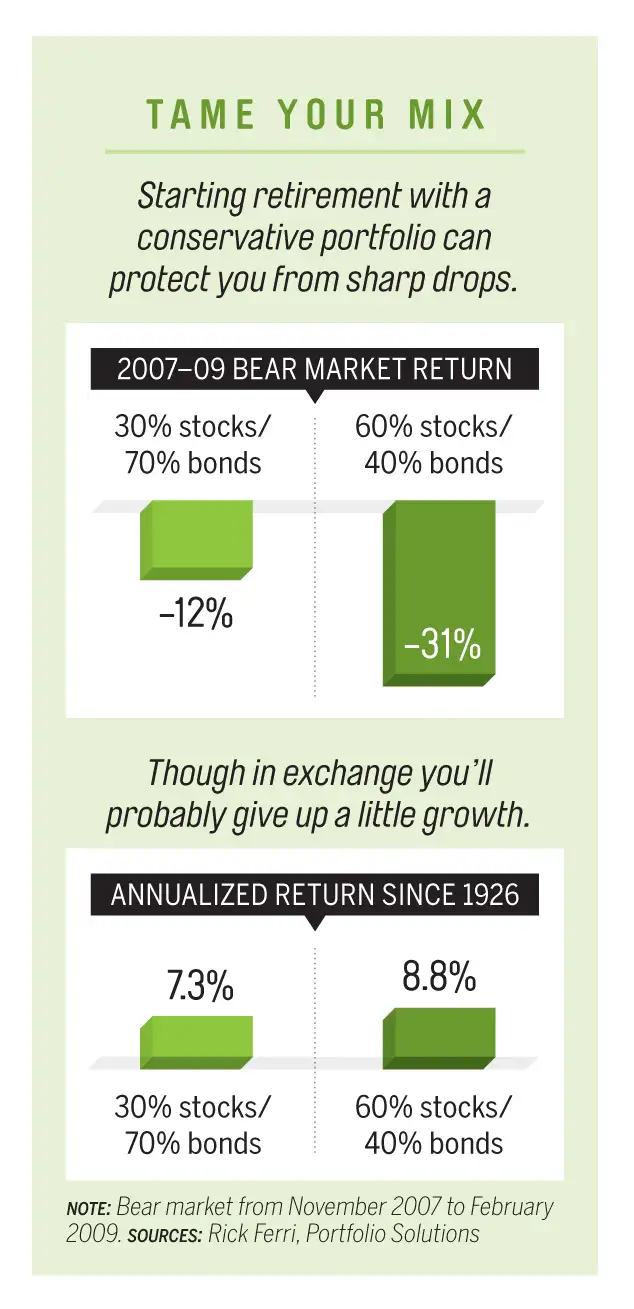

A bear market at the start of retirement could put a permanent dent in your income. Retiring with a 55% stock/45% bond portfolio in 2000, at the start of a bear market, meant reducing your withdrawals by 25% just to maintain your odds of not running out of money, according to research by T. Rowe Price.

That's why financial adviser Rick Ferri, head of Portfolio Solutions, recommends shifting to a 30% stock and 70% bond portfolio at the outset of retirement. As the graphic below shows, that mix would have fallen far less during the 2007–09 bear market, while giving up just a little potential return. "The 30/70 allocation is the center of gravity between risk and return—it avoids big losses while still providing growth," Ferri says.

Financial adviser Michael Kitces and American College professor of retirement income Wade Pfau go one step further. They suggest starting with a similar 30% stock/70% bond allocation and then gradually increasing your stock holdings. "This approach creates more sustainable income in retirement," says Pfau.

That said, if you have a pension or other guaranteed source of income, or feel confident you can manage a market plunge, you may do fine with a larger stake in stocks.

Know When to Say Goodbye

You're at the finish line with a seven-figure 401(k). Now you need to turn that lump sum into a lasting income, something that even dedicated do-it-yourselfers may want help with. When it comes to that kind of advice, your workplace plan may not be up to the task.

In fact, most retirees eventually roll over 401(k) money into an IRA—a 2013 report from the General Accountability Office found that 50% of savings from participants 60 and older remained in employer plans one year after leaving, but only 20% was there five years later.

Here's how to do it:

Give your plan a shot. Even if your first instinct is to roll over your 401(k), you may find compelling reasons to leave your money where it is, such as low costs (no more than 0.5% of assets) and advice. "It can often make sense to stay with your 401(k) if it has good, low-fee options," says Jim Ludwick, a financial adviser in Odenton, Md.

More than a third of 401(k)s have automatic withdrawal options, according to Aon Hewitt. The plan might transfer an amount you specify to your bank every month. A smaller percentage offer financial advice or other retirement income services. (For a managed account, you might pay 0.4% to 1% of your balance.) Especially if your finances aren't complex, there's no reason to rush for the exit.

Leave for something better. With an IRA, you have a wider array of investment choices, more options for getting advice, and perhaps lower fees. Plus, consolidating accounts in one place will make it easier to monitor your money.

But be cautious with your rollover, since many in the financial services industry are peddling costly investments, such as variable annuities or other insurance products, to new retirees. "Everyone and their uncle will want your IRA rollover," says Brooklyn financial adviser Tom Fredrickson. You will most likely do best with a diversified portfolio at a low-fee brokerage or fund group. What's more, new online services are making advice more affordable than ever.

Go Slow to Make It Last

A $1 million nest egg sounds like a lot of money—and it is. If you have stashed $1 million in your 401(k), you have amassed five times more than the average 60-year-old who has saved for 20 years.

But being a millionaire is no guarantee that you can live large in retirement. "These days the notion of a millionaire is actually kind of quaint," says Fredrickson.

Why $1 million isn't what it once was. Using a standard 4% withdrawal rate, your $1 million portfolio will give you an income of just $40,000 in your first year of retirement. (In following years you can adjust that for inflation.) Assuming you also receive $27,000 annually from Social Security (a typical amount for an upper-middle-class couple), you'll end up with a total retirement income of $67,000.

In many areas of the country, you can live quite comfortably on that. But it may be a lot less than your pre-retirement salary. And as the graphic below shows, taking out more severely cuts your chances of seeing that $1 million last.

What your real goal should be. To avoid a sharp decline in your standard of living, focus on hitting the right multiple of your pre-retirement income. A useful rule of thumb is to put away 12 times your salary by the time you stop working. Check your progress with an online tool, such as the retirement income calculator at T. Rowe Price.

Why high earners need to aim higher. Anyone earning more will need to save even more, since Social Security will make up less of your income, says Wharton finance professor Richard Marston. A couple earning $200,000 should put away 15.5 times salary. At that level, $3 million is the new $1 million.