This Couple Wants to Have a Baby in a Year. Can They Afford It?

- We're in Our 20s, Have $65,000 in Savings, and Want to Buy a Home. Can We Afford It?

- This Generation Has a Huge and Growing Student Debt Burden. It's Not Who You Think

- This Is How Much Debt the Average American Has Now—at Every Age

- This Last-Minute Tax Move Could Save You Thousands. Here's How to Do It

- The 10 Best Places to Live in the South

Lauren and Warren Hicks are big planners. They're the kind of people who like to know every dollar needed and every risk possible before making a decision.

That approach worked well when they bought their home in Houston a little over a year ago—but it's leading them into a black hole of worry when it comes to beginning a family.

“When we bought a house, we spent a lot of time figuring out how much we could afford on the mortgage and down payment. But with children there is no real way to know how much you’ll need. We know it is costly, but not really knowing is scary,” says Lauren Hicks, age 29.

“We worry we’ll blow right through our savings,” adds Warren Hicks, 30. "I think about how much we make and how adding an expense of, say, $1,200 a month would affect us—especially if Lauren takes time off work."

The pair want their offspring (ultimately, they're hoping for three) to live a comfortable lifestyle. “I was very lucky,” says Warren. “My parents paid for my college education. I had a better childhood than many people, and I would like to be able to give that to my kids as well.”

The couple hope to have their first child within the next two years. But anxieties and unanswered questions—How much will it cost? How would we care for our newborn? Can either of us afford to take time off?—have the Hickses stashing money in savings without any real plan or target in mind.

“I almost feel like we’re just hiding money away, but that it could be working harder for us, that we could be doing something smarter with it,” says Lauren. “We want to prepare and make sure we’re in a good place before we do that. We’re very cautious people.”

With two CPAs in their extended families, the Hicks are well schooled in the importance of saving. Together the pair have managed to stash a little over $202,000 in a mix of retirement accounts: From the outset, they've aimed to put 10% of salary into retirement savings; they've also benefited from their employers' 401(k) matches and a booming stock market, and maxed out their Roth IRAs.

They carry no student loan or credit card debt, but with a year-old home purchase, the couple has nearly $360,000 left to pay off on their mortgage and subsequently very little equity in their home.

Lauren currently brings in $95,000 a year as a senior marketing manager; Warren earns $75,000 a year working in pipeline logistics for an oil company. Being the higher earner creates a lot of pressure, she says: “I feel I carry more responsibility for the household because I earn more," she says. "I’m just anxious … If I’m out of work and we don’t have my salary coming in for two months, what will that mean for us?"

Like many companies, her employer covers maternity leave through short-term disability payments. She’ll earn 60% of her salary for six weeks—eight weeks if she has a c-section—and then 40% for another two weeks after that. Beyond that, she'd be taking time off without pay.

Money asked financial planner Scott Hamilton to run through the couple's finances and help them figure out the best path forward for their current savings and future earnings.

What to Do Now

Hamilton praised them for their savings discipline; he felt that, with a few tweaks, they could afford those baby breaks and still remain on course for other goals—like funding their retirement savings, building up education accounts for future children, and paying off their home.

Here are his suggestions.

• Bulk up an emergency fund.

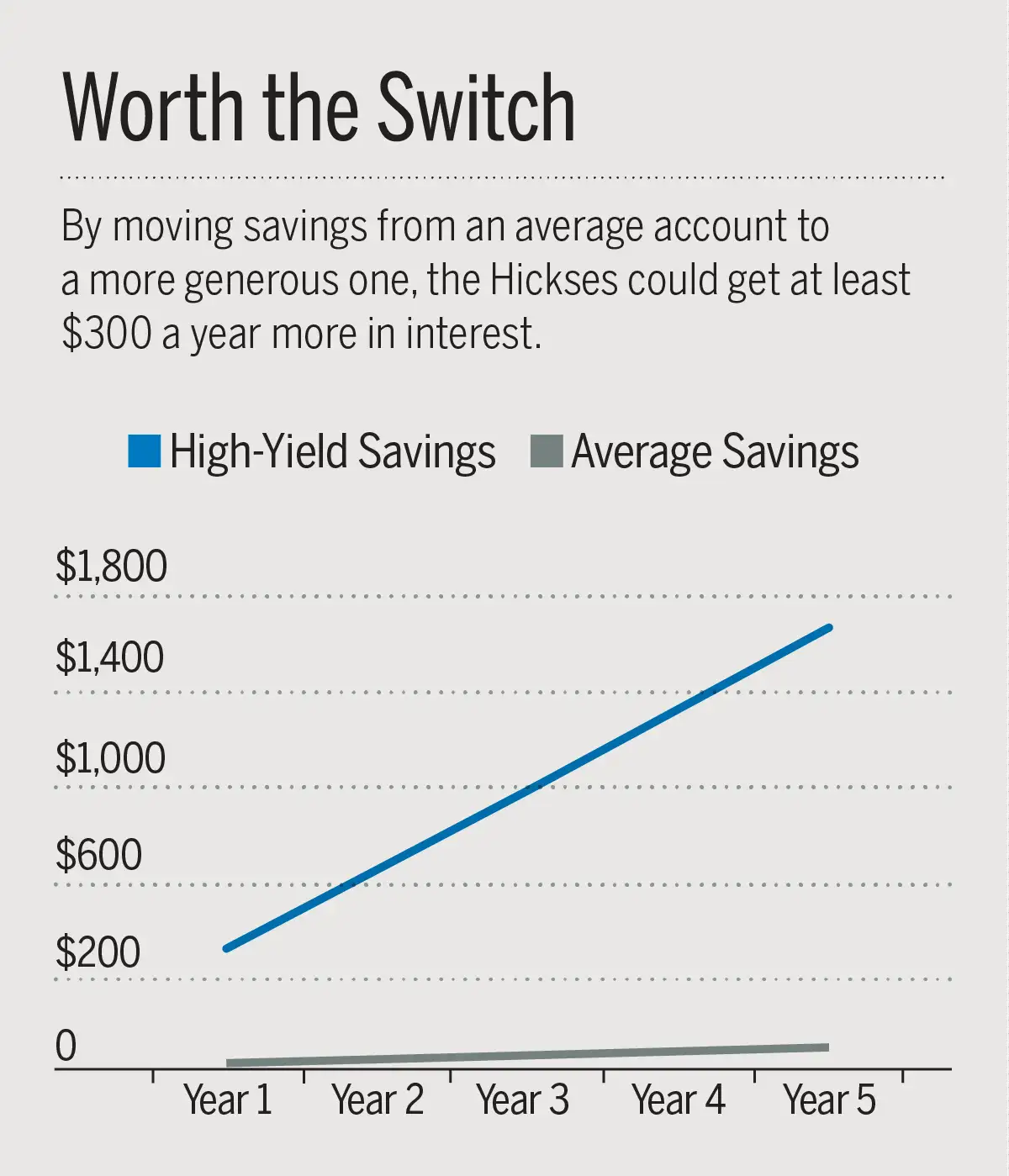

The first move the Hickses need to make: Drastically beef up their cash on hand. While the pair have been saving diligently, most of that money is in retirement accounts, such as 401ks, IRAs, and a Roth IRA. Currently, they have only $15,000 in a checking account and $23,000 in a savings account—short of the $60,000 Hamilton estimates ought to be in their rainy day fund.

He also wants the pair to move that sum out of a checking account and into a high-yield online savings account with Marcus (from Goldman Sachs) or Ally, where they’ll see a higher interest rate return.

Hamilton expects that the couple will need to dip into savings when the baby comes, but believes they should be able to forgo Lauren’s income for up to six months without too much strain. They'll need to replenish their emergency fund post-baby, Hamilton warns, to ensure that same level of cushioning—especially if they have two more children, as they intend.

• Change their investing strategy.

The Hicks have already stored quite a bit away in a mix of 401(k) and Roth IRA retirement accounts. That's all great, says Hamilton, who estimates that if they keep saving at the current rate, they could both retire at 65. That would give them $84,000 to spend per year, after accounting for taxes and mortgage payments, provided they also downsize to a condo when Lauren reaches 80.

Hamilton recommends they change their retirement portfolio, though. It currently holds 83% equities, particularly large-caps, along with 2% bonds, and 14% cash. He would like them to add more mid-cap, small-cap and international ETFs to more broadly diversify their stock holdings. The Hickses should also up their bond holdings to about 15%, leaving about 14% in cash, to bring them closer to Hamilton’s recommended 70/30 split.

• Prepare for college costs.

Given the couple's current spending and other goals, Hamilton thinks the Hickses can plan to pay 60% of the estimated college costs for all three future children—if they all go to state schools, such as the University of Texas. (The rest of the money will come from scholarships or student loans.) To get there, they’ll need to open and begin funding three 529 accounts right at the birth of each child, cutting back on some day-to-day expenses, and diverting a bit of the money they've been putting into everyday savings. Hamilton likes the 529 plans offered by the state of Utah, because they offer low-cost investment options from Vanguard and DFA and are easy to use.

• Lock up the what-ifs.

The final tasks are largely paperwork. The Hickses need important estate planning documents, such as a will, power of attorney, and medical directives. And once they do start a family, Hamilton recommends a term-life 20-year insurance policy that will cover the mortgage, kids’ education and current lifestyle should something happen to either of them.

Reality Check: Can They Do It?

Lauren and Warren Hicks admit they feel a little overwhelmed at the thought of the changes Hamilton has suggested. Still, it's nice to hear that they are on the right track. “It’s good to have a gut check,” says Lauren. “I feel like we have a plan and a to-do list now. We know what we need to be doing.”

Warren adds that he wants to do some of his own research when it comes to readjusting their portfolio. “That is the area I know least about, so I want to learn more of the basics behind it—but then we will likely follow what Scott said,” says Warren. “But otherwise I’m 100% onboard with his advice.”

Changes he and Lauren plan to make immediately? Creating a will, a task they’ve been putting off, and building that emergency fund. They’ve already begun making changes to free up funds for that account—canceling several automatic subscriptions, curbing dining out and entertainment spending, and limiting their travel budget.

“It feels like a lot of money to save but it also seems like the right amount," Lauren Hicks says. "We’ve both been laid off in the past. We’ve seen the recent flooding here. It will make us feel more secure.”