This Is How Much Debt the Average American Has Now—at Every Age

- More Than 33% of Men Say They've Faked a Vacation Photo

- 9 Ways to Outsmart Debt Collectors

- The Big Mistake More Car Buyers Are Making

- We're in Our 20s, Have $65,000 in Savings, and Want to Buy a Home. Can We Afford It?

- This Generation Has a Huge and Growing Student Debt Burden. It's Not Who You Think

Americans have fallen back in love with debt.

Total household debt—a category that includes mortgages, student loans, and car loans along with credit card and other debt—dipped in the wake of the Great Recession, but it has since steadily rebounded in the years since. Overall, Americans' debt hit a new high of $13 trillion last year, surpassing the previous record set in 2008 by $280 billion, according to the New York Fed.

Money dug into data from the Federal Reserve's Survey of Consumer Finances to examine just how much debt—and of what types—Americans were carrying at every age.

As it turns out, people's peak earning years also appear to be their peak debt years. People between the ages of 45 and 54 reported the highest levels of debt overall, totaling $134,600. Those in the 35-44 age bracket carry the second-largest amount, at $133,100. If you are on the other side of the coin, and have extra cash, see our article on how to invest in stocks.

Here's how much Americans owe overall, broken down by age group:

Under 35: $67,400

35–44: $133,100

45–54: $134,600

55–64: $108,300

65–74: $66,000

75 and up: $34,500

That's to be expected, says John R. Salter, professor of financial planning at Texas Tech University. "The trend tends to follow when people have children and those kids' needs. We see that rise in debt at the time most people are looking for bigger homes to get more space for their family, buying cars for their children, or paying college tuition for them."

People may also feel more comfortable taking on debt in these years, Salter speculates: This stage of life is also typically when people feel established in their careers, a time when they seek out promotions and raises and therefore experience higher earnings.

The following chart, based on Fed data, breaks down average 2016 debt levels and types for all U.S. consumers.

It has, to some extent, an element of symmetry. For those just starting out, the under-35 group, the total average debt was $67,400. That's pretty close to the $66,000 average debt for those between the ages of 65 and 74. Both groups are sitting just outside those peak earning years, and are less likely to have child-related expenses to contend with. (We'll get to the 75+ cohort in a minute.)

Yet the types of debt held by the two groups were vastly different.

Households run by those under age 35 carry the most education debt—a function of their age as well as recent surges in education expenses and financing, something that older generations were less likely to face. The average millennial household owes $14,800 in student loans.

For those in the 65-74 category, on the other hand, the second-largest source of debt was tied to real estate that was not a primary residence—presumably vacation homes or investment properties.

Debt levels drop off sharply for those 75 and older, who owe less than $35,000 on average—most of that in the form of a mortgage. Even so, some experts note, that five-figure debt level is still jarring.

"We're seeing people carrying much more debt than previous generations into retirement," says Ron Rhoades, professor of finance at Western Kentucky University. "Before, most people would have already paid off their 30-year mortgage before retiring—but those generations also weren't taking advantage of home equity lines of credit and refinancing options. Paying off such a loan really aids cash flow in retirement and makes your financial situation less precarious."

Some fretted that younger families will be carrying even more debt as they age, compared with today's 60- and 70somethings.

"Younger people are taking on debt at a higher rate and paying it off at a lower rate," says Lucia Dunn, an economics professor at Ohio State University who has studied consumer debt. "When they reach age 75, the debt picture for them will look a lot different than what we currently see. When you project out these trends, it is not so optimistic."

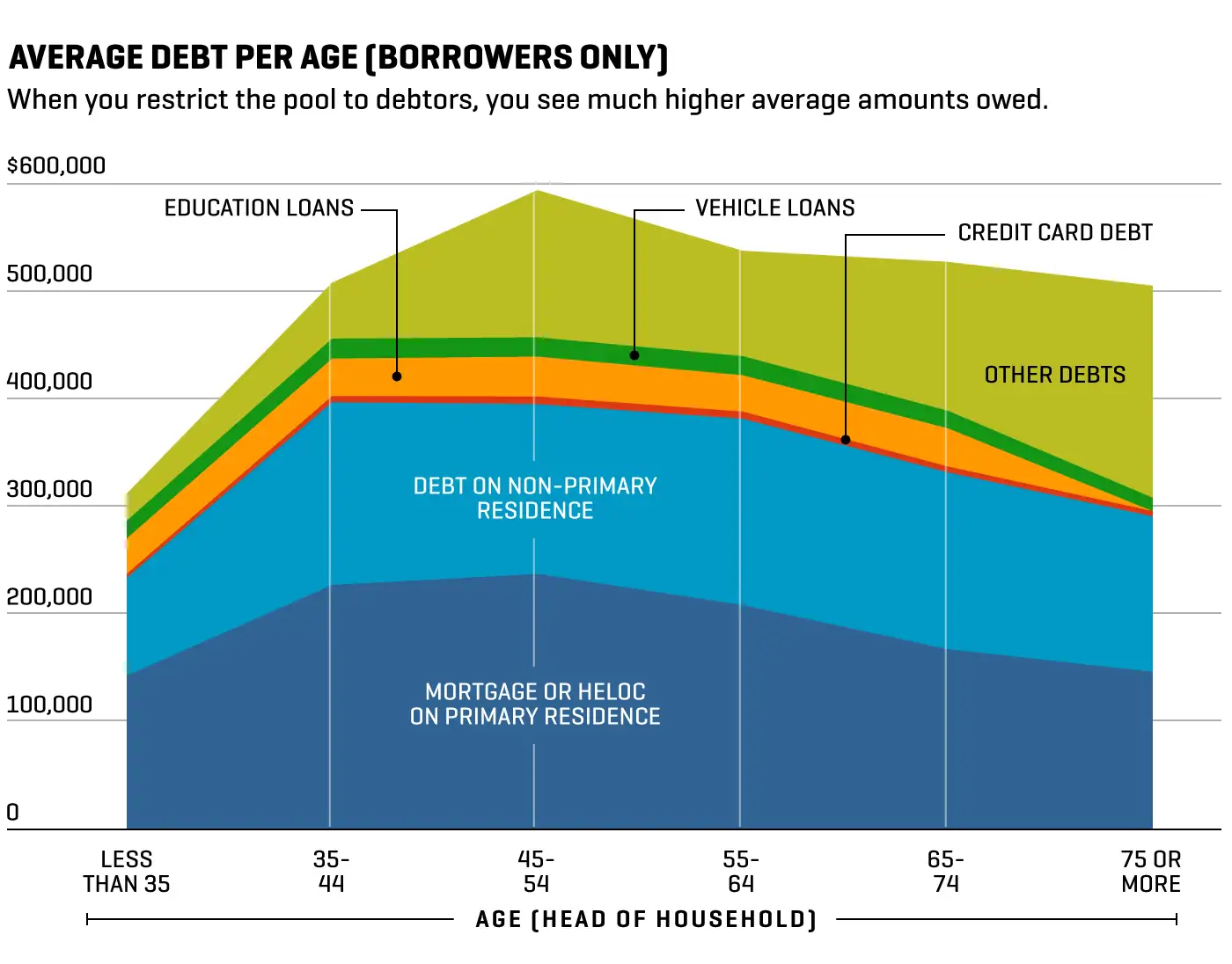

The above data considers debt levels across all Americans—mixing in both borrowers and non-borrowers, and averaging out the debt levels across the whole group. So Money also looked at the Fed public data set that considered only the debt levels of those who do borrow. The results are below.

In this case, total debt loads rapidly rise after age 35 and taper only slightly as people inch toward retirement. Some areas such as education loans, vehicle loans and credit card balances remain relatively consistent across all ages—suggesting that for those who habitually borrow for car purchases, for instance, the amount borrowed doesn't vary much by age. (On the other hand, the share of people who carry vehicle-related debt peaks at 44% among 35- to 44-year olds, and slides to 13.7% among those 75 and older.)

Education debt follows a similar pattern. The average balances stay fairly consistent among age groups under 75, hovering in the range of $32,900 to $37,000. However, the share of each age bracket with education-related debt drops steadily with time. About 45% of people under 35 have education debt, but that figure drops about 10 percentage points for each subsequent cohort before bottoming out to nothing for those over age 75.

Another big difference between the charts is the large green band of "other" debt in the second graph, particularly among age 75 and older. This category, which includes loans taken out against a pension or life insurance policy, affects just 1.5% of the 75-and-up population, according to the Fed data. Yet the size of the balances owed hints at the budgeting struggles many retirees face as they try to live off a fixed income.

Other differences between the charts are less surprising. While relatively few people (less than 10% across all age groups) carry debt on a non-primary residence, for instance—something reflected in the relatively slim light blue band in the first chart—such loans and mortgages can be substantial, making that debt much more significant for those who hold it, as seen in the second chart.

Both Rhoades and Salter noted that all generations show a greater comfort level with debt in all forms. "This idea of saving for what you need and buying it outright has diminished as people have become more comfortable with financing," Salter says. That could pose a problem later on, he adds: "These norms come with the future risk that you will be able to pay it all off."