Mutual Funds: Not Dead Yet

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

In many industries, new competition is disrupting the way business is conducted. Think department stores and cable television. Now the $12 trillion mutual fund industry is threatened too.

Since 2007, mutual fund assets have grown less than 50%, while the collective amount invested in exchange-traded funds—baskets of securities that can be traded like individual stocks—has more than tripled, to $2 trillion.

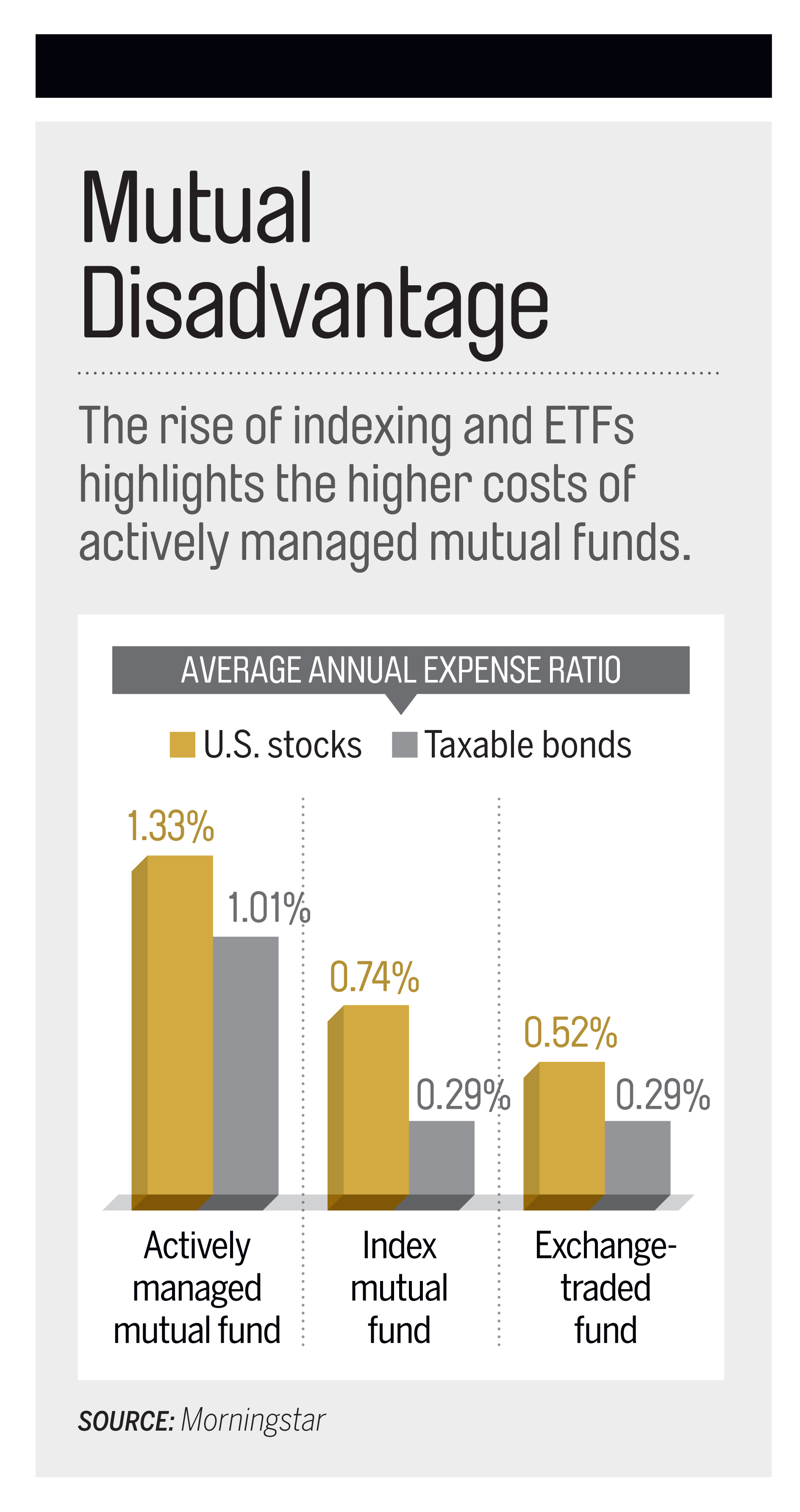

Traditional mutual funds are suffering from the growing popularity of low-cost passive investing. Last year investors poured nearly 10 times as much money into index portfolios, which simply buy and hold all the securities in a sliver of the market, as they put into actively managed funds. And the vast majority of ETFs are index portfolios, many charging lower expenses than mutual funds.

Meanwhile, ETF-like investments could gain traction in the realm of active management.

So far, few actively managed ETFs have been launched because the Securities and Exchange Commission requires them to divulge their holdings in real time — something stock pickers are wary of doing.

However, the SEC recently greenlighted an ETF-like vehicle that solves the disclosure problem. Exchange-traded managed funds, or ETMFs, will be required to reveal their holdings only a few times a year, like traditional mutual funds.

Eaton Vance, which won approval for its NextShares ETMF structure and is licensing it to other money managers, expects to launch its first ETMFs this year.

Because ETFs and ETMFs are traded on an exchange and don’t require back-office and marketing functions, they can charge less. Eaton Vance expects that on average a NextShares ETMF could cost about 0.63 percentage points less than a mutual fund version. So while the average actively managed mutual fund charges $133 a year for every $10,000 you invest, ETMFs may cost just $70 a year.

Still, mutual funds have been around for 91 years and aren’t going the way of the dinosaur tomorrow.

A big reason is that 401(k) plans, which control more than $4.4 trillion in assets, have yet to embrace ETFs. Until that happens—and until ETMFs arrive in full force—here are ways you can still put traditional funds to good use.

Satisfy Your Core Stocks

When it comes to the bulk of your equity portfolio, it doesn’t matter if you use index ETFs or index mutual funds as long as you pick a cheap option. “Low cost is low cost, period,” says Dave Nadig, chief investment officer of ETF.com.

As you can see from the chart below, though, not all index mutual funds charge rock-bottom prices.

Fix the Bond Problem

Money has warned of the risks of putting all your bond money into traditional index funds and ETFs. Those portfolios are obliged to load up on what are now the most expensive parts of the fixed-income market: U.S. Treasuries and agency-backed mortgage debt that the Federal Reserve bought in droves to stimulate the economy.

Jeff Layman, chief investment officer at BKD Wealth Advisors, says his firm has switched from passive core bond funds to active managers, who have the leeway to diversify into less frothy parts of the market. With few exceptions, most actively managed high-grade bond portfolios are mutual funds. A good option is Money 50 pick Dodge & Cox Income , which charges just 0.43% in annual fees.

Fill a Niche

For narrowly focused assets, Samuel Lee, editor of Morningstar ETFInvestor, says you can find traditional mutual funds with deft active managers who have the flexibility to “avoid horrendous transaction costs.” Surprisingly, some of these funds charge lower expenses than ETFs. For example, he prefers Vanguard High Yield Corporate , an actively managed fund that charges 0.23% a year, over SPDR Barclays High Yield ETF, which charges 0.40%.

Commodities are another area where mutual funds may make more sense. ETFs that invest in physical commodities or futures contracts are less tax-efficient than a regular fund that owns commodity-related stocks.

Collectively these investments represent just a minority of your overall portfolio. Still, it means the death of the fund may be exaggerated—for now.