The New College Grad's Guide to Money

- Is Debt Settlement a Good Idea?

- Who Doesn't Have to File Taxes This Year? Details for Retirees, Students and Gig Workers

- Pell Grants Will Soon Help Students Pay for Job Training Programs

- From Loans to Jobs, Here's How the Fed Rate Cut May Affect Your Wallet

- 5 Things to Know About the Trump Administration’s Plans to Limit PSLF

The shift from college to the working world has always been a blur of living-on-your-own excitement and what-do-I-do-now anxiety. That's truer than ever today, with 70% of 2016 grads owing for their education (the average college debt is about $30,000). So while you've set yourself up to make a decent salary (you hope), you've never faced this many expenses, and you're probably starting out in the hole.

Scary? A little. But you really can learn how to handle yourself on the road to smart money management. This guide, featuring questions submitted to Money from recent and soon-to-be graduates, can help.

Tackle Student Loan Debt

Question: How much of my salary should I devote to paying off my student loans? —Alejandra Carraza, class of 2016, Fort Pierce, Fla.

Answer: Let's prioritize: Eat first, then pay rent, then worry about the loans. Financial planners say not to spend more than 15% of your salary (before taxes are taken out) paying off your loans, but plenty of people can't even manage that. In fact, the federal government recently expanded its student loan repayment options so that anyone can limit his or her monthly bill to 10% of income after paying for essential living expenses. To qualify for lower payments, you'll need proof of your income, like a pay stub or tax return. For more information, go to StudentAid.ed.gov.

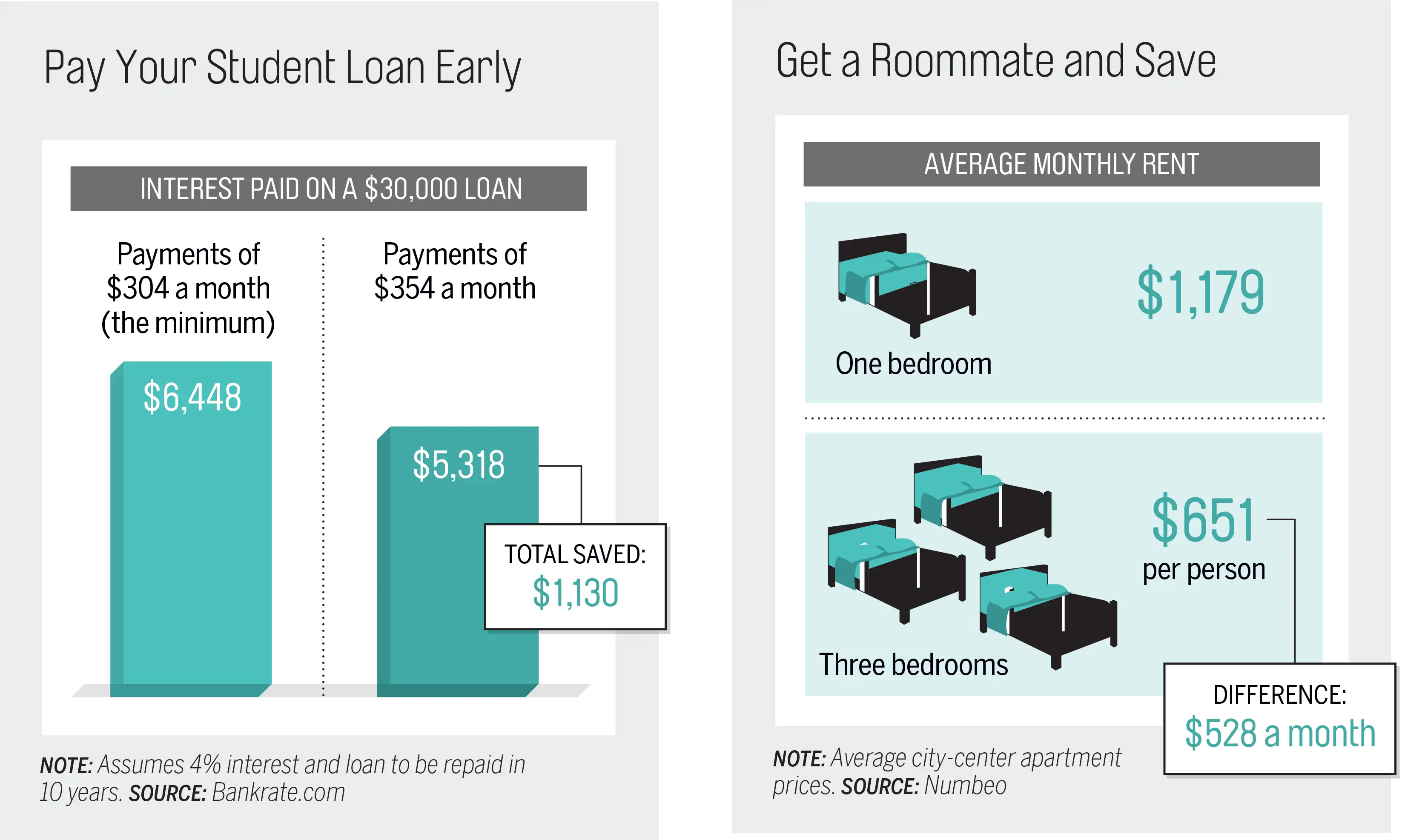

On the other hand, you may get ahold of extra cash from time to time, particularly at raise or year-end bonus season. That's a good time to pay down some extra principal, which will cut your overall interest costs and trim the length of your loan, says Myles Newborn III, a financial planner in Stony Point, N.Y. Pay off private loans first; they tend to have higher interest rates. And tell the company that sends your monthly bill to apply extra payments to the loan with the highest interest rate. Otherwise the money will be split equally among all loans.

Tip: Use some of your annual tax refund to pay extra on your loans, and don't forget to deduct your student loan interest (up to $2,500 a year) from your taxes.

Tool: You can estimate your monthly payments, calculate total interest paid, and compare various government repayment options on the Department of Education's StudentLoans.gov website.

Save for a Major Purchase

Question: I'd need to drive to my dream job, but I can't afford a car. How can I save up enough to buy one? —David O'Brien, class of 2016, St. Leo, Fla.

Answer: This one will require some math—specifically, keeping a budget. Start by jotting down all your essential living expenses: rent, utilities, transportation, food. They should eat up only half your take-home pay. Loan payments should be about 15%. That will leave roughly a third of your salary (after taxes are taken out) for savings and the occasional fun run. The best way to stay disciplined is to squirrel away your cash before you can even touch it.

Tip: Bump up your savings by earning extra money through flexible side gigs. Search for odd jobs through Taskrabbit, Gigwalker, or Airtasker. Don't have time for a second job? Get a roommate to cut your expenses.

Tool: Use apps such as Mint (free) to create a budget. Follow your spending over a month or two. Then look for areas to cut, such as dining out.

Budget for Health Insurance

Question: I have health insurance through my company, so I don’t need to budget for this, right? —A composite question based on several we received.

Answer: Your paycheck will still have a deduction if you enroll in your employer’s health insurance program. And health insurance premiums (that’s the amount you pay each month to be insured) can eat up a noticeable part of a small salary. ADP research found that for earners in the $30,000 to $45,000 range, health plan premiums cost 5.8% to 6.9% of income. On average, single workers contributed $1,071, or about $90 a month, for employer-sponsored coverage in 2015, according to the Kaiser Family Foundation.

If your employer doesn’t offer health insurance, you can buy it through the Health Insurance Marketplace. Bronze plans, which have higher co-pays and deductibles but less expensive monthly premiums, are usually a fine choice for someone who’s young and healthy, says Erin Hemlin, national training director with Young Invincibles, a nonprofit organization that advocates for healthcare and economic policies that benefit young adults.

But if you expect to have medical work done in the coming year or you have a chronic illness, you’d be better off with a silver plan, Hemlin says.

The average marketplace shopper was able to get a plan for a monthly payment of $75, with the help of tax credits for workers earning less than $46,000.

Finally, if you’re not working or are working part-time, you might qualify for Medicaid for free if your state is one of 32 that approved Medicaid expansion. That would be a good option for someone enrolling in graduate school, Hemlin says. Not sure if your state participates? Check the Status of State Action on Medicaid Expansion Decision table on the Kaiser Family Foundation website.

Tip: You may be able to save some money by staying on your parents’ health insurance plan for a few more years. But check to make sure the plan’s network is available where you live. Also compare costs first, as plans for single adults are often much cheaper than family plans. So it might be less expensive, in total, for you and your parents to insure separately.

Tool: Healthy Young America, an app from Young Invincibles, offers a crash course in health insurance. It includes a glossary of terms, FAQs about how to get coverage, a calculator to estimate your costs, and the ability to search for nearby doctors—though it won’t tell you whether those doctors are in your network. For that, try Zocdoc to search doctors and schedule appointments.

Bargain for Higher Pay

Question: How can I negotiate a fair salary with my limited experience and income history? —Tom McMorrow, class of 2018, Moorestown, N.J.

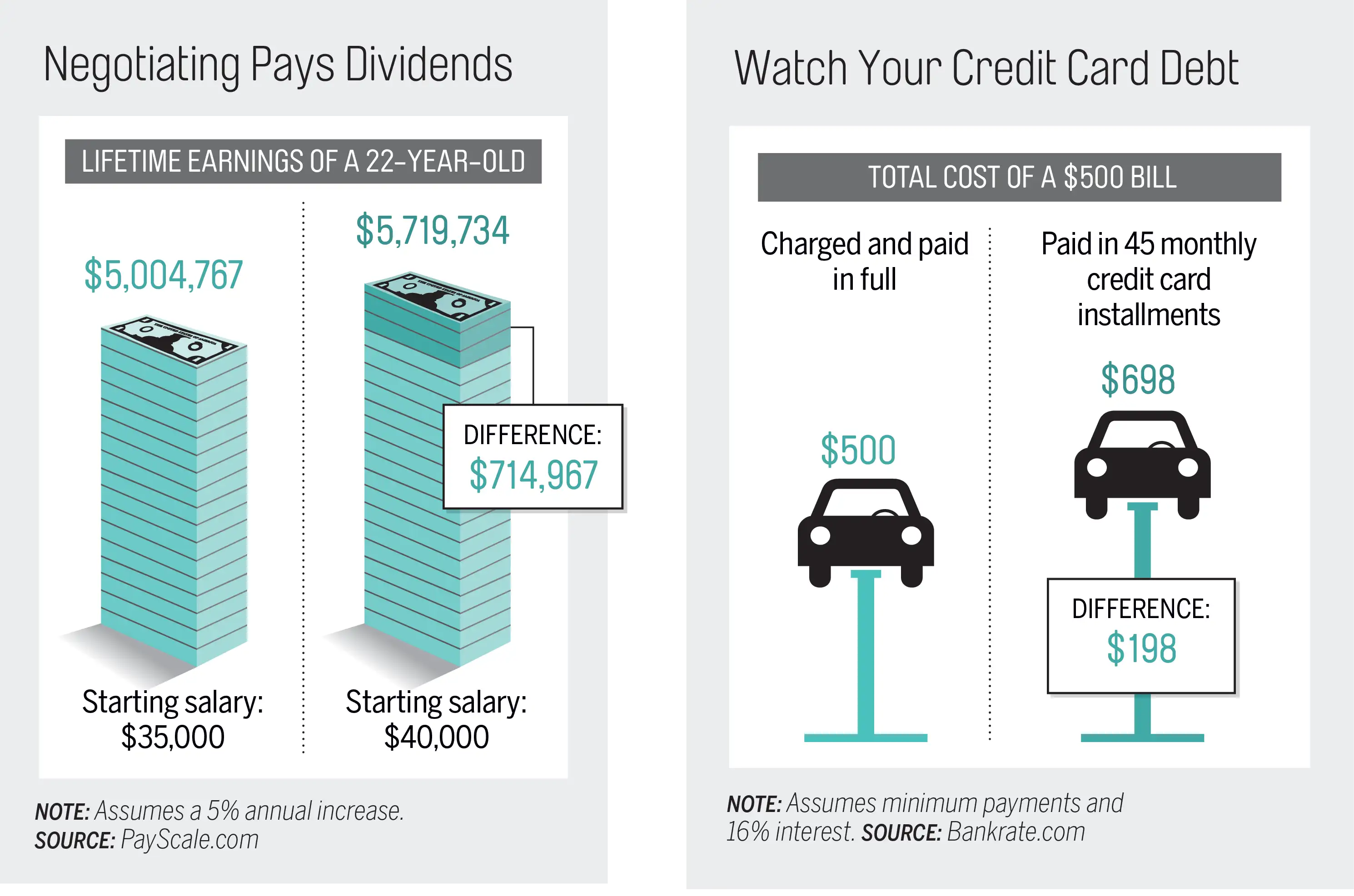

Answer: Rule one (stolen from the Boy Scout handbook): Be prepared. Websites such as Glassdoor, PayScale, and Salary.com contain intel on hundreds of companies, down to the specific job titles in specific cities. That said, you'll be in much better shape if you let the interviewer start the salary discussion. If you throw out the first number, you might undersell yourself with a price that's at the low end of what the company is willing to pay. If the interviewer tries to coax you into making the first move ("What salary range are you looking for?"), deflect him or her—nicely. ("Why don't you tell me your expectations for the job so I can get a sense of what you're looking for?")

When you do start talking numbers, back up your request by touting the specific goals you can help the company reach with your skills. "It is your job to explain what you're worth, and why," says Robin Pinkley, a professor of management and organizations at the Cox School of Business at Southern Methodist University

Tip: To boost your confidence and get ready for anything that's thrown at you, rehearse your talking points with a friend.

Tool: For more pointers, check out the "Negotiating Your Salary" video on Lynda.com (free for a 10-day trial).

Create an Emergency Fund

Question: How much should be earmarked for urgent expenses, and where do I put the money? —Heidi Smith, class of 2015, Cranston, R.I.

Answer: You eventually want to have banked three to six months worth of expenses in case you lose your job. But it's okay to start small-. For now, you're looking to cover unexpected expenses—say, a car repair or your best friend's last-minute destination wedding in Hawaii—without using your credit card. A good goal: Save $1,000 your first year out of college by putting aside $85 a month.

Tip: Open a separate savings account and set up an automatic deposit after each pay period so that you can't even be tempted to spend your stash.

Tool: Have a little fun-—and maybe win a gift card or two—by joining SaveUp. Linked to your savings account, SaveUp is a free website that rewards you with points for every dollar your save. The points can then be used to enter lotteries that pay cash prizes, gift cards, vacations, and more.

Save for Retirement

Question: Do I need to put aside money for retirement now, or can I wait until I'm in my thirties? —Lina Saud, class of 2015, Princeton, N.J.

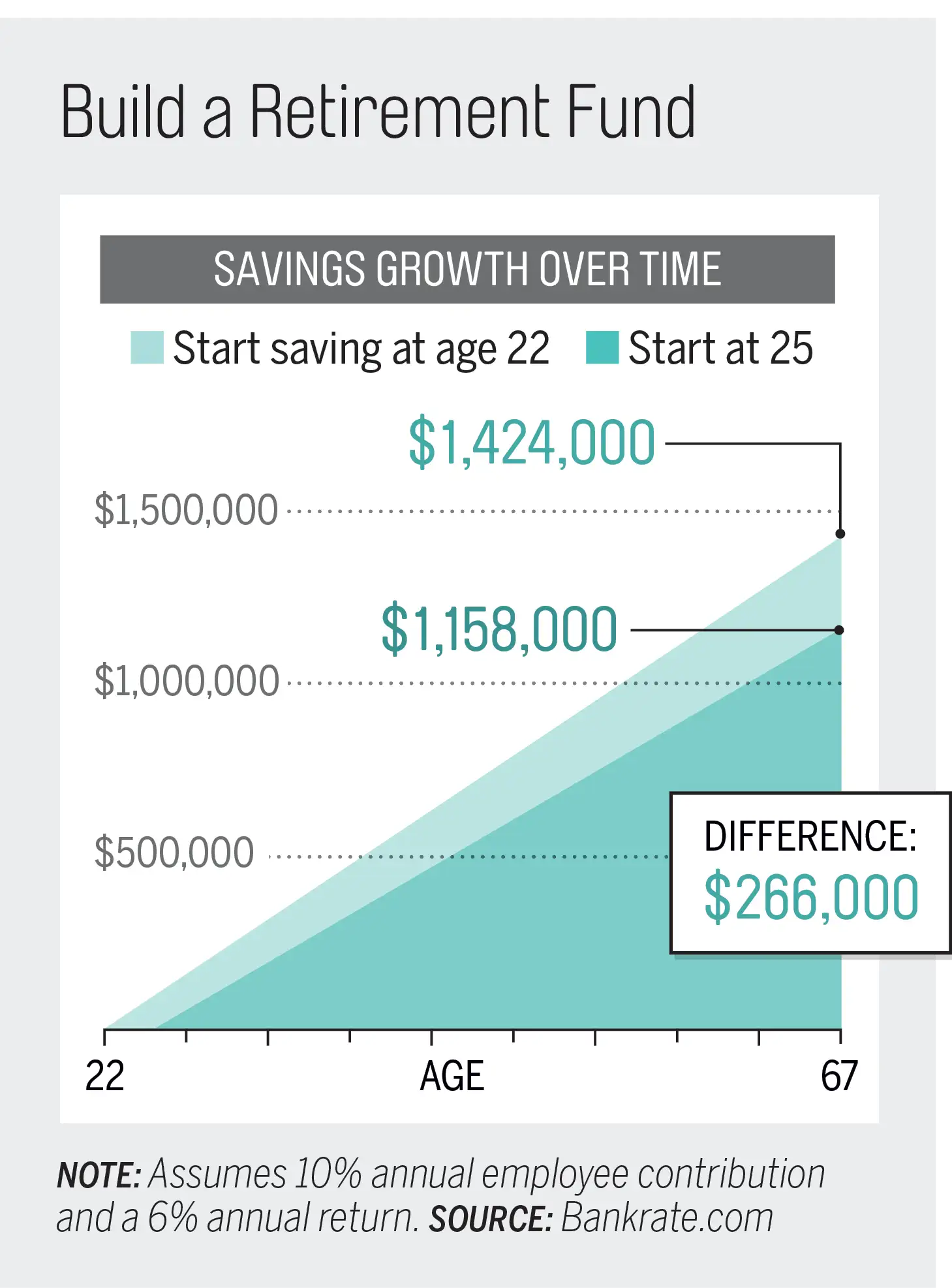

Answer: Start now. "You have the power of time on your side," says Denver financial planner Bob Morrison. "Leverage that." That said, don't freak out. Anything you put away is better than nothing. Set aside just $500 a year (about $10 a week) over your first five years, and you'll have nearly $30,000 more at retirement than if you had saved nothing then. If your company has a program that matches your contributions to a 401(k) retirement account, take advantage of that. It's like free money (albeit money you can't touch for another 40 years). And it's a smaller chunk out of your check than you may realize. Unlike your salary, the government doesn't take taxes out when you put money into a 401(k), so funneling $100 to your account takes only about $85 from your take-home pay.

If your company doesn't have a retirement plan, open a Roth IRA, which allows your contributions to grow and be withdrawn tax-free. They're offered by most banks and investment companies; Vanguard and Fidelity, which offer many low-cost investment options, are good places to start. Look for funds with low costs or "expense ratios" below 0.5%.

Tip: Bring your lunch four out of five days a week, and you'll save $800 to $1,000 a year on average. That's a good bit of your first year's retirement contribution.

Tool: Use our retirement calculators to see how fast your savings can grow. You'll be feeling rich in no time.

Save for Your First House

Question: How can I balance being a renter with simultaneously saving for a down payment on a house? —Tom McMorrow, class of 2018, Moorestown, N.J.

Answer: Start by making sure you’re not busting your budget by spending too much on rent. Rent and associated bills (like utilities) shouldn’t take up more than a third of your income before taxes are taken out. You should also prioritize paying off any credit cards and having some emergency savings set aside before putting away money for a house.

Once you’ve done that, redirect the amount you were spending toward those goals to your new goal, a house fund. If you get a raise or a bonus, sock away that cash for your home, too.

It may also help to open a separate savings or conservative mutual fund account, one that’s primarily invested in bonds, since saving for a home is a relatively short-term goal, says Scott Moffitt, president of Summit Financial Group in Loveland, Ohio. (See the next question for more on mutual funds.) Aim to save at least 20% of the cost of the house before you buy.

Tip: Planning for a house is great, but don’t rush to buy. To make up for the closing and legal costs of buying a home, you’ll want to be sure you’re going to stay put for at least five years. When you do buy, Moffitt recommends budgeting an extra 5% of the purchase price for annual upkeep and maintenance—expenses that longtime renters may overlook.

Tool: If you’re open to relocating, focus your job hunt on parts of the country with affordable housing as well as quality jobs. A good place to start: the American Institute for Economic Research’s Employment Destinations Index, which ranks cities based on wages, employment opportunities, and living costs.

Get Started Investing

Question: I know I should be investing in stocks, but how do I actually begin buying them? How do I pick companies to invest in? —Morgan Wolf, class of 2016, Jacksonville, Fla.

Answer: Successfully investing in individual companies’ stocks requires a lot of time and energy to research and manage your portfolio, says Bill Pratt, an author of personal finance books for college students and a vice president of The Money Professors, a group of finance professors focused on financial literacy on campus.

Even then, picking the winners is incredibly hard. And odds are, your long-term returns won’t beat the market.

So, for most busy people, investing in an index fund, which simply mirrors the stocks or bonds in a popular market index, such as the S&P 500, is a better bet. Because your money is spread across many different companies, index funds offer built-in diversification that insulates you from the risk of a particular stock or industry losing value.

You can buy an index fund through a brokerage firm or directly from a mutual fund company; the latter will tend to have fewer fees. Look for a low-cost fund with a minimum initial contribution you can afford.

Many funds have fees of less than 0.2%, but you may have to pay slightly more if you don’t have a lot of money to start with. For example, Vanguard’s 500 Index Fund has a 0.17% expense ratio and a $3,000 minimum initial contribution. The company’s STAR Fund’s minimum is $1,000, but the expense ratio is double, 0.34%.

If you don’t have a lump sum for a large initial contribution, look for funds that allow you to make smaller, automatic monthly deposits. Or, consider managing your investments through newer services, such as Betterment or Wealthfront (these are Internet companies sometimes called robo-advisers), which have modest account minimums.

Tip: Investing is a great way to build long-term wealth, but only after you’ve checked off other, more basic financial boxes, such as paying off credit cards and building an emergency fund.

Tool: Check out the Money 50, our annual list of the best mutual funds and exchange-traded funds to invest in. And use our investing calculators to compare different types of investments, assess your risk tolerance, and more.