What to Do When Your Funds Veer Off Course

- What's the Difference Between Mutual Funds, ETFs, and Index Funds?

- There Are Now More Crypto Coins Than U.S Stocks

- The Best Time to Buy Bitcoin, Explained in One Chart

- This Two-Minute Viral Video Proves It's Impossible to Time the Stock Market

- AMC, GameStop and Hertz: What's Causing the Latest Meme Stock Swings?

ILLUSTRATIONS BY CHRIS GASH

BEING A STOCK PICKER takes real chutzpah. Not only must you think you're smarter than most investors who fail to beat the market, but you have to be willing to go against the crowd—and stick to unpopular picks in the face of mounting losses and criticism. Yet as anyone who has seen the hit musical Hamilton knows, the line between being bold and foolhardy can be astonishingly thin.

Recently one of the most respected funds in the industry arguably crossed that line, raising a question for investors: What do you do if your contrarian manager wanders too far off the beaten path? At issue is the Sequoia Fund, which made a surprising bet on Valeant Pharmaceuticals starting in 2010. At one point last year shares of the controversial drug company grew to more than 30% of the portfolio, a staggering weighting for a mutual fund, for which the abiding characteristic is supposed to be diversification. After questions about Valeant's sales practices arose, the bet turned out to be spectacularly wrong, leading to huge losses, redemptions, and a shake-up at the fund.

But Sequoia is hardly alone. History is replete with managers flouting convention—and being wrong. More than 20 years ago Jeffrey Vinik made the costly decision at Fidelity Magellan to sell hot technology stocks and buy bonds several years before the bubble burst.

Yet the situation is more complicated when dealing with a value-minded stock picker, who by definition is supposed to be stubbornly contrarian. How much rope do you give such managers? That depends on why they're off course, how far off course they are, and how the shift fits into their long-term strategy. To help you figure that out, Money took a close look at three respected funds that have strayed from their peers to assess when to forgive and when to cut ties.

Sequoia Fund

–––––

PERFORMANCE VS. PEERS

3-year rank: Bottom 1%

15-Year Rank: Top 15%

The Vision: Be like Buffett. Sequoia, in fact, was founded in 1970 by a longtime friend of Warren Buffett's, and most of the fund's original clients were referrals from the Oracle himself. You can't beat that pedigree.

Like Buffett, Sequoia's strategy is to buy solid companies at attractive prices and hold them for years, as any business owner would. The fund switches up only about 10% of its portfolio in a given year, making it nearly as patient as an index fund. Even better, Sequoia's oldest holding is Buffett's company, Berkshire Hathaway, which accounts for about 15% of the fund.

Read: America's Most Important Investor Has a Message for You

For the most part this strategy has panned out. Had you invested $10,000 in Sequoia 20 years ago, you would be sitting on more than $56,000 today—even after the fund's recent losses. That same $10,000 would have turned into less than $35,000 in the average large-growth stock fund.

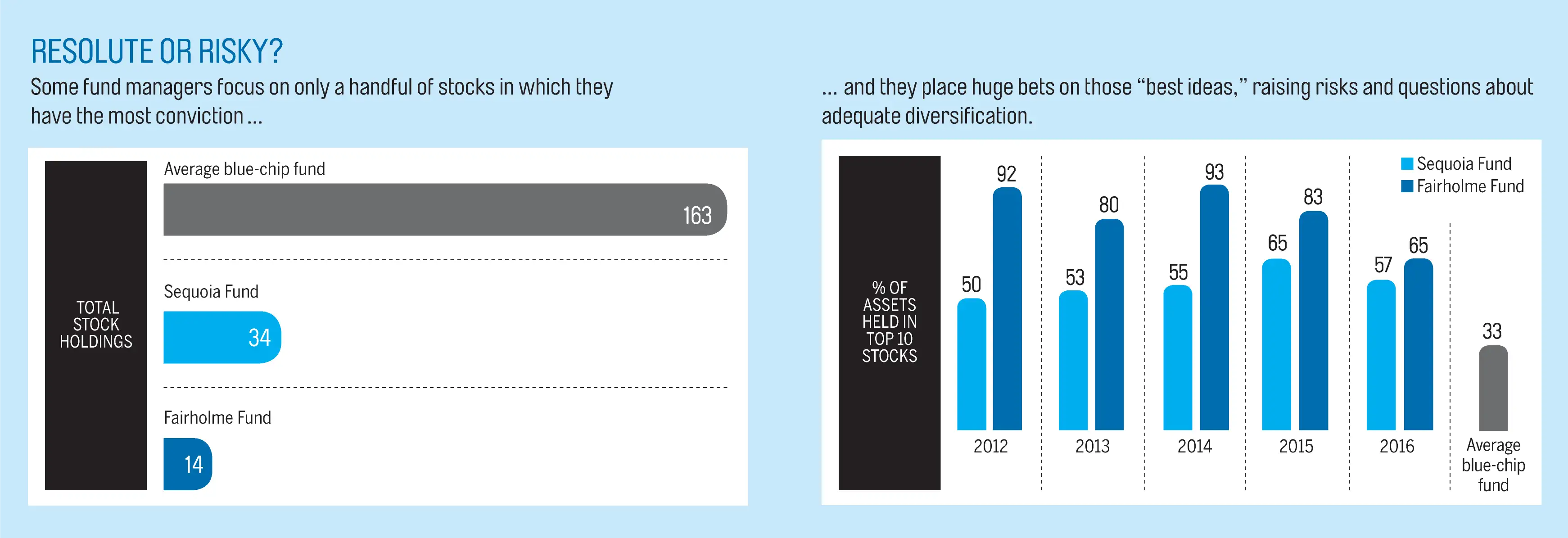

How it Veered: The fund may have taken Buffett too literally. America's most successful investor once joked that diversification "makes little sense if you know what you are doing." And for about 40 years the team at Sequoia seemed to have sufficient skill to place bigger-than-average bets on its top picks (see chart below).

As recently as last September this aggressive approach helped the fund outpace nine out of 10 blue-chip growth-stock funds over the prior 10 years, according to Morningstar. But after losing more than a quarter of its value in the past 12 months—owing in large part to the stunning 90% drop in Valeant's stock—Sequoia now trails 85% of its peers over the past decade.

"Anybody can play Monday morning quarterback," says David Frisch, a planner in Melville, N.Y. What's important, he says, is to understand if the manager's actions are a mistake or a problem with the process. That's what was troubling here. Sequoia's long-standing lead manager, Robert Goldfarb, maintained a huge stake in Valeant even after the stock lost more than half its value and after two of the fund's directors—whose job it is to represent shareholder interests—resigned over this bet.

Calculator: What is my risk tolerance?

What's more, all this was over a company that, at least in retrospect, seems far from being a classic staid Sequoia holding. A favorite among hedge funds, Valeant was a flashy and politically controversial stock. In 2010, Valeant used a merger with a Canadian company to relocate its headquarters to Quebec, which helped it cut its corporate tax rate. Then the company used that so-called inversion to acquire other firms, knowing that it could then cut their taxes too. It further boosted profits by buying existing drugs from rivals and hiking prices, which drew the ire of consumers and launched congressional probes, which eventually led to the stock's undoing.

Making matters worse, Valeant carries a significant amount of debt on its balance sheet, which meant it had less margin for error when markets turned against it. This is hardly the type of company you'd associate with Buffett.

The Verdict: As the fund's losses grew, investors yanked nearly $1.5 billion over the past year, prompting Sequoia to reopen its doors to new investors for the first time since 2013. This is a second chance for investors to get into a fund that's trying to prove itself again. For new investors, it's an opportunity worth taking.

For starters, Valeant was really the only troubled stock among Sequoia's top holdings. The rest of the portfolio is filled with high-quality businesses such as MasterCard and the industrial distributor Fastenal, with little long-term debt. And while "there is a perception that the whole team went off the rails, that isn't true," says Morningstar analyst Kevin McDevitt. "It was Goldfarb exercising his veto power, saying, "No, we are going to stick with this position."" And that manager stepped down in March and was replaced with David Poppe, who has been a co-manager at the fund for the past decade.

Read: Where to Find Quality Investments Now

Finally, Sequoia "owned up to" its mistakes, says New York City financial planner David Mendels, an investor in the fund. By the end of June, Sequoia eliminated its entire Valeant stake. In addition, the advisory firm in charge of the fund—Ruane Cunniff & Goldfarb—has put safeguards in place to prevent overreach again at Sequoia. "We know we made a misjudgment," says Poppe. "We touched the electric fence, and we will not do it again."

The fund now imposes a hard cap: No stock can make up more than 20% of the fund's assets. And no one manager will have the power Goldfarb enjoyed. Ultimate authority for strategy now rests with a committee of five.

At the same time, the company has been in the process of strengthening its bench. Even before Goldfarb's departure, Sequoia had been beefing up its research staff, doubling its team of investment analysts to 12.

This doesn't mean Sequoia is out of the woods. The fund must prove that it won't repeat past mistakes, while avoiding being gun-shy about making the types of contrarian bets that propelled the fund in the first place. "They do careful research and don't trade," says Mendels. "They had an overall process that worked for a long time," he adds, noting, "I don't think there is any reason it can't work again."

The Fairholme Fund

–––––

PERFORMANCE VS. PEERS

3-year rank: Bottom 1%

15-Year Rank: Top 1%

The Vision: Manager Bruce Berkowitz takes contrarianism to a new level. When he founded the fund in 1999, at the height of the dotcom bubble, he went against the tech-crazed crowd by betting on staid insurers and financial stocks. A few years later, he bought energy shares when oil was in the dumps and rode crude's climb to more than $140 a barrel. Had you invested $10,000 with Fairholme in 2000, you'd have amassed more than $35,000 a decade later, nearly triple what you would have had with the average large value stock fund. In 2010, Morningstar named Berkowitz its domestic stock fund manager of the decade.

In the wake of the financial crisis, Berkowitz acted just as you would expect: by snapping up tarnished names like American International Group, Bank of America, and more recently mortgage giants Fannie Mae and Freddie Mac. Yet the results this time weren't as good. Fairholme gained just 4.3% annually over the past five years, trailing the S&P 500 by eight points a year.

Berkowitz insists his contrarian bets will eventually work out, noting these investments were made after careful study. He spent three years making store visits and quizzing commercial real estate brokers to research Sears—another top holding—which he likes not necessarily because of its retail outlook but for the real estate.

How it Veered: It's not the stocks Berkowitz owns that are raising eyebrows. It's the size of his bets. At one point two years ago, AIG grew to half of his entire fund. Meanwhile, he has routinely concentrated more than 80% of his assets in his top 10 picks. The fund has brought that figure down a bit this year, but something else is worrisome. This $2.8 billion equity fund is betting on only 14 stocks. That's less than 9% of the shares held by the typical blue-chip stock fund.

To be fair, Berkowitz's huge gamble on AIG has succeeded. Five years after Fairholme bought it, AIG stock posted annualized returns of 16.6%, outpacing the 14.7% gains for the Russell 1000 Value index. Though not a home run, "AIG worked out okay," says Morningstar's McDevitt. The same, though, can't be said for Berkowitz's other financial sector investments. "The bet that did not work out," McDevitt says, "was on banks like Bank of America."

The Verdict: Berkowitz is regarded as one of the industry's sharpest minds. Yet his own results prove that when you bet on a dozen or so distressed stocks, you have to be right on most of those ideas. And that hasn't been the case lately. Over the past three years Fairholme has been flat while the S&P 500 gained 10.5% annually.

Unlike the team at Sequoia, Berkowitz does not believe he has erred, so there's been no change in policies. The fund "is not process based," says planner Mendels. "It's Berkowitz based." And the manager is willing to wait more than a decade for his bets to pan out—too long for older investors with less than a 20-year horizon. Fairholme first bought Sears in 2005, and since then the stock is off about 90%. Yet he's still willing to wait.

Read: Why Young Investors Should Ignore the Market Jitters and Get in the Game

This is really a fund "appropriate for someone who is 25 and can continue to invest over years" if not decades, says Maryland financial planner Drew Cook. Why should young investors bother? Remember, Berkowitz was one of the few stock pickers who made big money in the market's "lost decade" from 2000 to 2010. But be cautious.

Fairholme shouldn't serve as your core value fund. It holds too few stocks for that, and Berkowitz's idiosyncratic approach has turned what was once a blue-chip fund into a small-stock fund whose average stock is worth just $1.2 billion, vs. $78 billion for its category peers.

FPA Crescent

–––––

PERFORMANCE VS. PEERS

3-year rank: Bottom 19%

15-Year Rank: Top 2%

The Vision: Morningstar classifies FPA Crescent along with traditional balanced funds, portfolios that typically offer investors a mix of stocks and bonds to reduce overall risk. But longtime manager Steven Romick has never viewed the fund quite in that light. Romick and his co-managers are all about finding good values, no matter what asset class they're dealing with.

Ultimately the fund seeks to "generate equity-like returns over the long term" while taking on less risk than the market, according to its mission statement. Sound too good to be true? The fund has beaten the S&P 500 by more than three points annually over the past 15 years.

How it Veered: A typical balanced fund keeps close to 60% of its assets in stocks and about 35% in bonds, leaving the rest for cash and alternative assets. Romick's fund, by contrast, has less than 5% in fixed income with more than 36% parked in cash.

FPA has openly stated that Crescent is willing to hold cash from time to time. But even Romick admits the fund's 36% stake is larger than normal. He says 25% is more typical. And since cash is paying next to nothing, this weighting explains why Crescent trails the average balanced fund by about one point annually, and the S&P 500 index by six points, over the past three years.

Calculator:

Crescent's big cash stake may seem conservative, but you can't paint this fund as staid. Romick is willing to bet on junk bonds, as he did recently when energy companies were hit by low prices. Most balanced funds focus on higher-quality fixed-income securities. Romick also short-sells, or bets against, stocks—a potentially risky strategy.

The Verdict: This fund is worth buying, especially if you're worried about a shaky market. Exotic strategies should always give you pause, but some of Romick's seemingly risky moves are designed to make the fund safer.

Junk bonds are used instead of stocks, not to replace fixed-income holdings. And he typically shorts stocks to hedge bullish bets, not for short-term gains. For instance, his largest short position—against Chinese tech company Tencent—is offset by a bullish one in Naspers, a South African media company that owns a stake in Tencent.

As for his cash, "it's a value discipline," says Colorado Springs financial planner David Haraway. Romick is simply waiting for better bargains to present themselves in the stock and bond markets. But that means his defensive cash pile could be used to go on offense if the markets sink and good values start presenting themselves.

The downside is that this disciplined approach is leading to underperformance. But "with the cash buffer you end up with less volatility from year to year," Haraway says. Over the past 15 years, Crescent has gained 2% more than other balanced funds in up months while losing 25% less than its peers in down months. That's a combo worth veering off path for.

How Other Funds Go Rogue

–––––

Value-stock fund managers aren't the only ones who surprise investors with bold and unconventional approaches.

You don't have to look too hard to find other funds that have gone astray.

Your Bond Fund Owns What? When Bill Gross left Pimco two years ago, he launched Janus Global Unconstrained Bond. While the fund's name hints at an unconventional take on fixed income, it implies bonds. Yet 25% of the fund sits in cash and stocks.

Last year, Puerto Rico began threatening to default on some of its debts. That's when investors in some single-state muni bond funds far removed from the island—such as the Oppenheimer Rochester Maryland Municipal Fund and Oppenheimer Rochester Virginia—learned that their funds held more than a third of their assets in Puerto Rico's debt.

Read: How to Strike a Balance With Bonds

Your Stock Fund Owns What? Equity funds can surprise investors in a myriad of ways too. The $111 million Monetta Young Investor Fund, for instance, is an equity portfolio that has been swapping out individual stocks for exchange-traded funds, which make up roughly half its portfolio now. Monetta asserts the strategy makes the fund less risky. "It's diversified," says co-manager Robert S. Bacarella.

That's true. ETFs are funds that typically hold hundreds of stocks. But it also means investors are paying to cover for not only Monetta's investment management and marketing costs but also the fees on those underlying ETFs. The all-in cost is more than 1.2% of assets a year, according to the fund's prospectus.

Those Bets are How Big? Meanwhile Sequoia and Fairholme aren't the only funds making focused bets. Putnam Capital Spectrum has more than 20% of its holdings in one stock—Dish Network—and more than 50% in its top five picks.

How can fund investors mitigate these risks? Planner David Frisch says investors should treat niche or contrarian funds as they would adding individual stocks. In other words, if you own them, hold them as modest supplements to your core portfolio.