Will Our Emergency Fund Count Against Us for College Financial Aid?

Q: I've been socking money away in CDs for our emergency fund, but I worry that when we eventually fill out financial aid paperwork for my daughter's college, the money will be considered in determining her aid. Is there a way to protect it, or are we going to have to use it to pay for college? —Chelle Parks, Colorado Springs, Colo.

A: Kudos to you for both saving for emergencies and thinking toward future expenses, not an easy feat.

The good news is that you probably won't have to worry about spending much or any those emergency savings for college.

The federal government's financial aid formula considers only a portion of your assets in determining your eligibility for aid, notes Paula Bishop, a CPA and college financial aid adviser. Up to a certain level, your assets are covered by the government's asset protection allowance. And any money you have in a retirement account is totally off limits.

"People are so worried about how much money they have to report for financial aid, but you've got to have a lot saved before you're dinged in a big way," Bishop adds.

In your case, dear reader, it's tough to say how much of your assets will be protected when applying for financial aid, since we don't have any specific numbers. But the following guidelines may help.

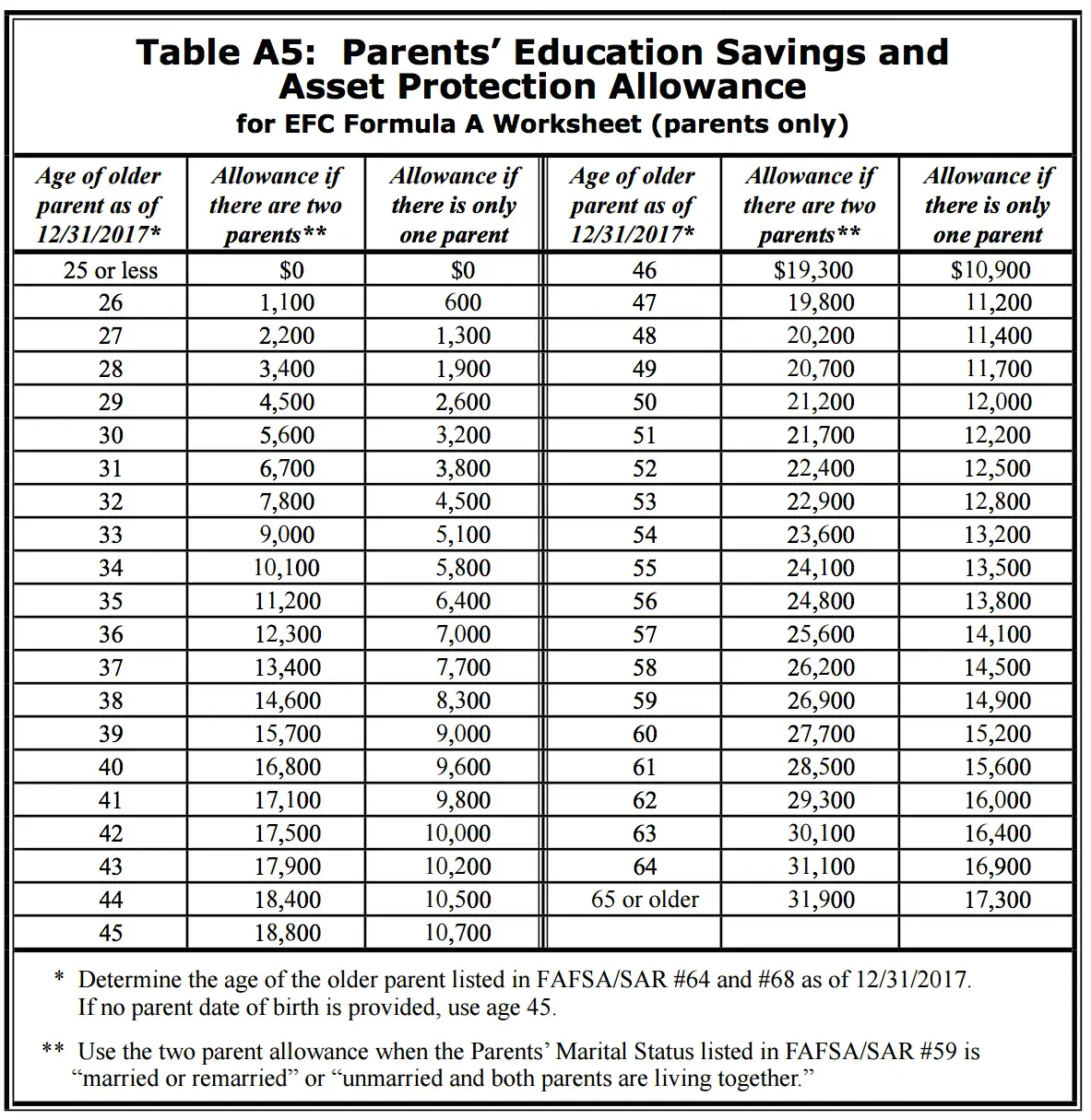

After you fill out the Free Application for Federal Student Aid, or FAFSA, the government calculates what it calls your Expected Family Contribution toward college costs, taking into account your asset protection allowance. Currently, according to this EFC formula sheet, the allowance ranges from $1,100 to $31,900 for parents, based on age and marital status. The older you are, the more of your money qualifies for asset protection (more still if there are two parents in the picture instead of just one).

Bishop gives this example:

"Say someone saves $100,000 and it's the only non-retirement money she has. Assuming you're sending your child to a public college, they'd probably subtract out $25,000 as protected assets, which means you've now got $75,000 available to the formula used to determine financial aid. The run rate on those assets is 5.64%, which means they're only expecting you to pay $4,230 a year toward college" out of your assets.

(Your income also figures into the equation, of course. Most families will be on the hook for $8,728 plus 47% of any adjusted gross income over $32,300.)

The Federal Student Aid office in the Department of Education offers the handy chart shown here to help you figure out how much of your assets will be protected.

If you keep your emergency fund in CDs, you'll list it under "reportable" assets when you apply for financial aid, along with other assets like stocks, bonds, and brokerage accounts..

Some assets, however, are considered "non-reportable" for FAFSA purposes. Those include the equity in your family home and the value of any small business with fewer than 100 employees.

In theory, you could reduce the amount of money you're required to report by paying down debts or moving it into a non-reportable category, such as a retirement account. But your options are limited. For example, if you're under age 50, you can contribute only $5,500 to an IRA in any given year.

To be sure, life insurance is another way to invest money in a way that is non-reportable to the FAFSA. But this strategy is fraught with its own set of risks, including high fees and lousy products as a 2013 Money investigation found.

The bottom line? Don't let concerns about aid eligibility deter you from saving as much as you're able to for college. "It's best to sleep tight and still save money for college like you would otherwise," Bishop says.