How to Make Smart Choices for Your 401(k) at Retirement

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

It's one of the biggest financial decisions you'll ever make: choosing what to do with your 401(k) at retirement. That account may be the largest asset you will rely on for income in later life. You could leave it where it is or roll the money to investments inside an IRA. The right decision could give you hundreds of thousands of added dollars over a 30-year retirement.

Exercising extreme care is more important than ever. On Wednesday, the Department of Labor postponed implementation of parts of the fiduciary rule, which had been scheduled to go into effect on April 10, until June 9. In February, President Donald Trump had asked the department to consider whether to revise or roll back the rule, an Obama-era measure intended to protect retirement savers from self-interested brokers giving poor advice.

Here's a three-point plan to help you make smart choices for your nest egg.

1. Look, But Maybe Don't Leap

Start by comparing your 401(k) and IRA options. Some 46% of retirees left their money in their plan when they stopped working, while 44% rolled the funds to an IRA, a 2016 survey by the Employee Benefit Research Institute found. In 2014 alone, Americans ages 60 to 64 moved $113 billion from 401(k)s into IRAs, according to the Internal Revenue Service.

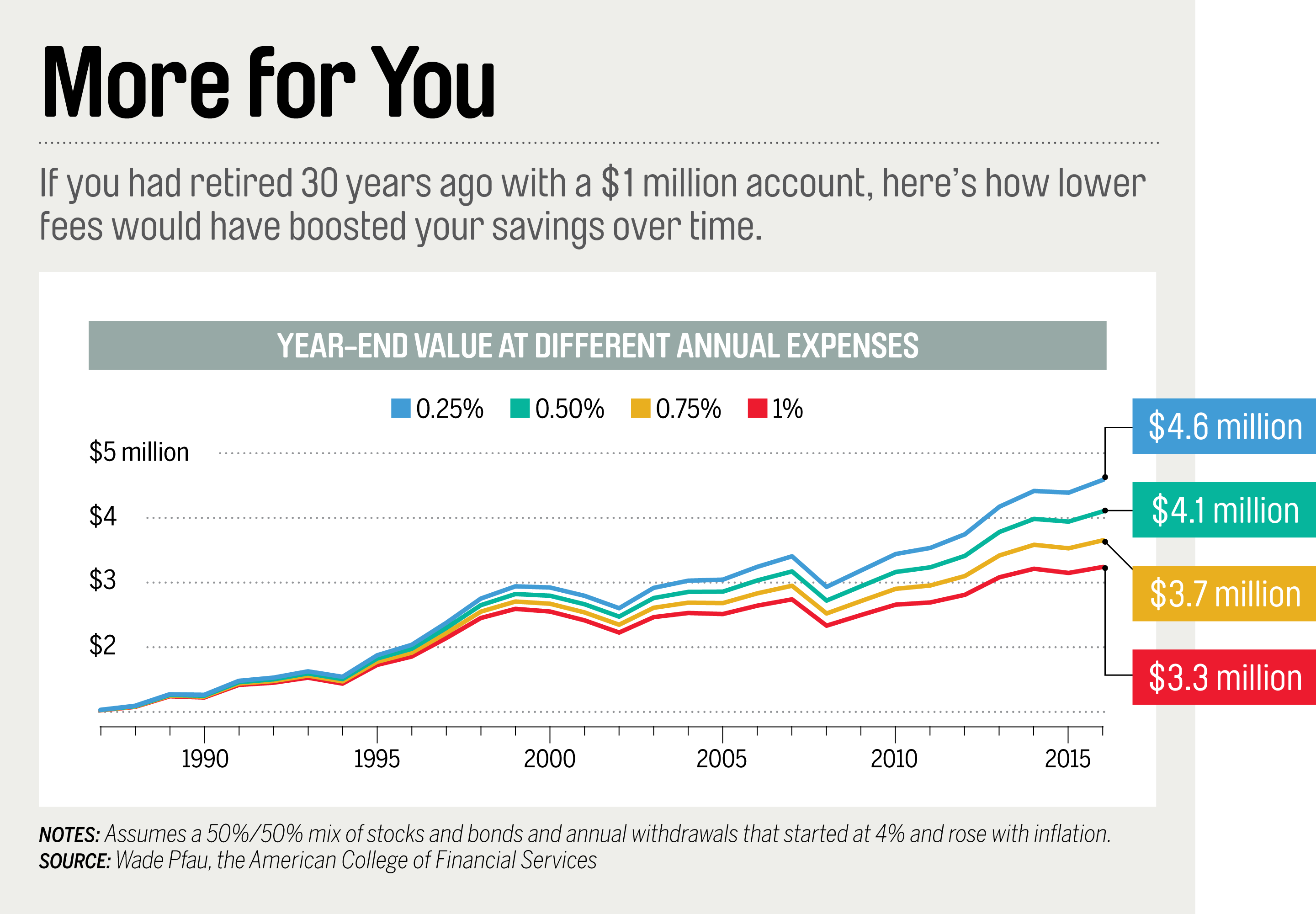

If you work for a small company, where expenses built into the 401(k) can top 1% of assets a year, you can probably save big by switching to an IRA and buying super-cheap index funds and ETFs. On a $1 million account, going from fees of 1% to 0.5% would save you $5,000 in a single year. There may be some savings, but far less, if you work for a large company that has numerous low-cost funds on its menu.

You'll have lots more investments to choose from with an IRA: The average 401(k) offers 28 options, according to a report by BrightScope and the Investment Company Institute, while the average IRA investor at Fidelity, for example, can choose among more than 10,000 funds from hundreds of fund companies.

Still, there may be attractive options inside your 401(k) you can't replicate on your own. In particular, many 401(k) plans include stable-value funds, which aim to protect your principal while also delivering an interest rate, currently around 2%, that is higher than what other cash equivalents offer.

These accounts, which include backing from a bank or an insurer, generally aren't available outside 401(k) plans. If you have access to one, you might want to hang on to it, says Dana Anspach, founder of Sensible Money, a financial planning firm in Scottsdale.

2. Check the Exit Routes

With an IRA, you call the shots on when to take money out and how much to withdraw. Many workplace plans haven't offered such flexibility—some have required you to withdraw all your money at once if you want any at all.

That's changing, though, says Rob Austin, director of retirement research at Aon Hewitt. Some 61% of large 401(k)s now allow people to withdraw a fixed or varying monthly amount. Most large plans can also adjust withdrawals starting at age 70½ to ensure retirees take the minimum distributions required by tax law.

If your 401(k) will be your primary source of income, you'll likely want the flexibility of monthly withdrawals, Austin says. If your plan doesn't offer that option, an IRA might be a better choice.

3. Write Your Own Fiduciary Rule

The fiduciary measure would require any adviser working with retirement savers to put those clients' interests first rather than simply make "suitable" recommendations. Whatever the fate of the rule, you can resolve that any adviser you hire be a fiduciary. "They're the ones you can trust to be looking out for your best interest," says Robbie Hiltonsmith, senior policy analyst at Demos, a nonprofit public policy group. (Search at napfa.org or garrettplanningnetwork.com for a fiduciary planner.)

Recognize, though, that there is no guarantee of competence and that even fiduciary advisers can have conflicts of interest. A planner who would charge a fee to manage your money in an IRA, for instance, collects zero on the dollars that stay in your 401(k). Be wary if an adviser is pitching you an investment plan that assumes returns of more than 7% a year for stocks, Anspach says. That person may be working too hard to clinch a deal "instead of educating the client about risks," she says.