Do These 3 Things Before You Head South for the Winter

You may not want to make a permanent exit from a locale where friends and family are near. But as the weather cools, many people in colder states start daydreaming about a retirement that includes months-long fun in the sun as a snowbird.

"You can live a more relaxed lifestyle," says Diahann Lassus, president of Lassus Wherley, a financial-advisory practice in New Providence, N.J., and Bonita Springs, Fla., that counts many snowbirds among its clients.

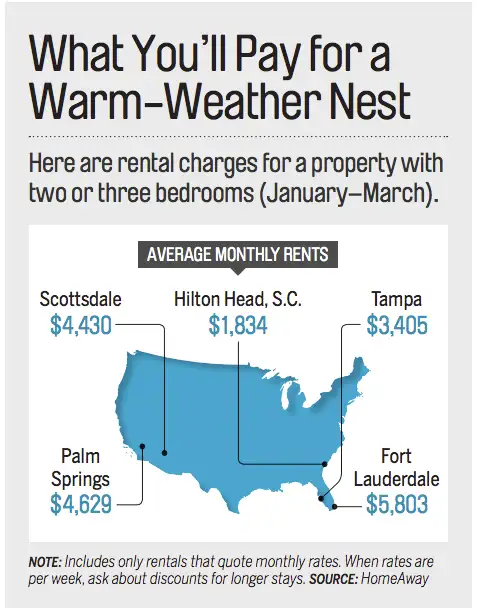

It's a big change in your life and finances, so spend at least one full season renting before you buy. And follow these tips to manage medical costs, get a grip on housing costs and other expenses, and possibly save on taxes.

Get flexible health coverage

Retirees on Original Medicare, also known as Part A and Part B, can visit any doctor or hospital around the country that accepts Medicare. Medigap supplement plans are similarly portable.

By contrast, with Medicare Part C, also known as Medicare Advantage, you may have more restrictions. About two-thirds of these plans are HMOs, many of which confine coverage to a specific network of doctors and hospitals in a particular locale. While plans must pay for emergency and urgent-care treatment out of network, they won't cover routine care in your second destination.

If you're in a Medicare HMO, you can switch to a different Medicare Advantage plan or to Original Medicare during open enrollment, from Oct. 15 through Dec. 7 each year.

As an under-65 snowbird, you should research the doctor and hospital choices of your current plan or ones you are considering.

You should hand-carry your medical records each time you relocate, says Rosemary Laird, executive medical director of the Florida Hospital for Seniors. It's also a good idea to keep hard copies of your advance health care directives in both spots.

Factor in new expenses

When snowbirds look at the potential cost of buying a second home, they often focus on the mortgage bill and property tax but fail to consider some less obvious costs. For example, Florida property owners have to run their air conditioners nearly year-round to avoid mold, regardless of whether the home is occupied, Lassus says.

If you're thinking of buying a property and then renting it out when you're not there, plan to pay from 10% to 15% of your rental income in fees to the property manager. A steady stream of renters can wear down a property, so budget for regular carpet replacement and painting.

When you're enjoying the Arizona sun in February, someone will have to shovel your snow in Illinois—unless, of course, you decide to sell your current house and rent in that area. That's an often-overlooked but attractive option for snowbirds who want to retain ties to their home communities without the hassles of maintaining a property there, Lassus says.

Some snowbirds pay for plane tickets for visiting family, plus food and entertainment costs during their stays, says Ron Weiner, a financial adviser in Boca Raton, Fla.

Read: Smart Reasons to Start Renting in Retirement

Be strategic to lower taxes

Home may be where the heart is, but it's also where you pay your state income taxes. If your second state has a more favorable tax climate, it may be possible—but not necessarily easy—to make that your home for tax purposes. The challenge is proving to your current state that you're no longer a resident there.

Karen Tenenbaum, a tax attorney in Melville, N.Y., says many of her snowbird clients want to switch their permanent residence to Florida to take advantage of the Sunshine State's lack of a personal income tax. One test New York uses to determine residency is whether you have a permanent home in the state for more than 11 months of the year and spend 184 days or more in New York during the year.

If you intend to claim your snowbird destination as your permanent home, change your car and voting registration to the new state, open bank accounts there, and get a new cell phone number, says Kelley Long, a member of the AICPA's National CPA Financial Literacy Commission.

Maintain a detailed calendar of the time you spend in each location and save plane tickets, Tenenbaum says. If you're audited, you could be asked for credit card bills to document where you were.