The Social Security 'Penalty' That Can Pay Off in the End

- What's the Maximum Social Security Benefit in 2017?

- Donald Trump Wants to Radically Change Medicaid. Here's What the Program Actually Does.

- Retire With Money: Your Social Security Timing is Critical

- Why the Social Security Trust Fund Should Invest in Stocks

- The Huge Retirement Penalty for Being a Mom

Early retirees are sometimes warned about imperiling their Social Security benefits by earning too much money from continued work. But some people approaching retirement may be more concerned about this risk than they need to be because they don't understand the rules.

Seventy-six percent of people ages 45 through 64 know that collecting a paycheck while receiving Social Security can reduce benefits before a person's full retirement age (FRA), according to an AARP survey last year. But 57% of that group think recipients never get that money back.

That isn't true. If you hope to retire early, here's what you need to know about the Social Security "earnings test" and how to make the right moves.

Know the earnings-test math

This rule applies to those who claim benefits before FRA, which ranges from age 66 to 67 for most people today. If your earnings from wages or self-employment exceed $15,720 a year, your benefits will be reduced by $1 for every $2 you make above that. (This limit is adjusted periodically for inflation.)

Calculator: Social security retirement income estimator

There's a less onerous rule in the year you reach FRA: You can earn up to $41,880 in the months prior to your birthday month without penalty. Above that amount, Social Security will withhold $1 for every $3 you bring in.

The good news: Once you reach your FRA, the test goes away. And Social Security will increase your benefit to account for the number of months you lost some or all of those payments.

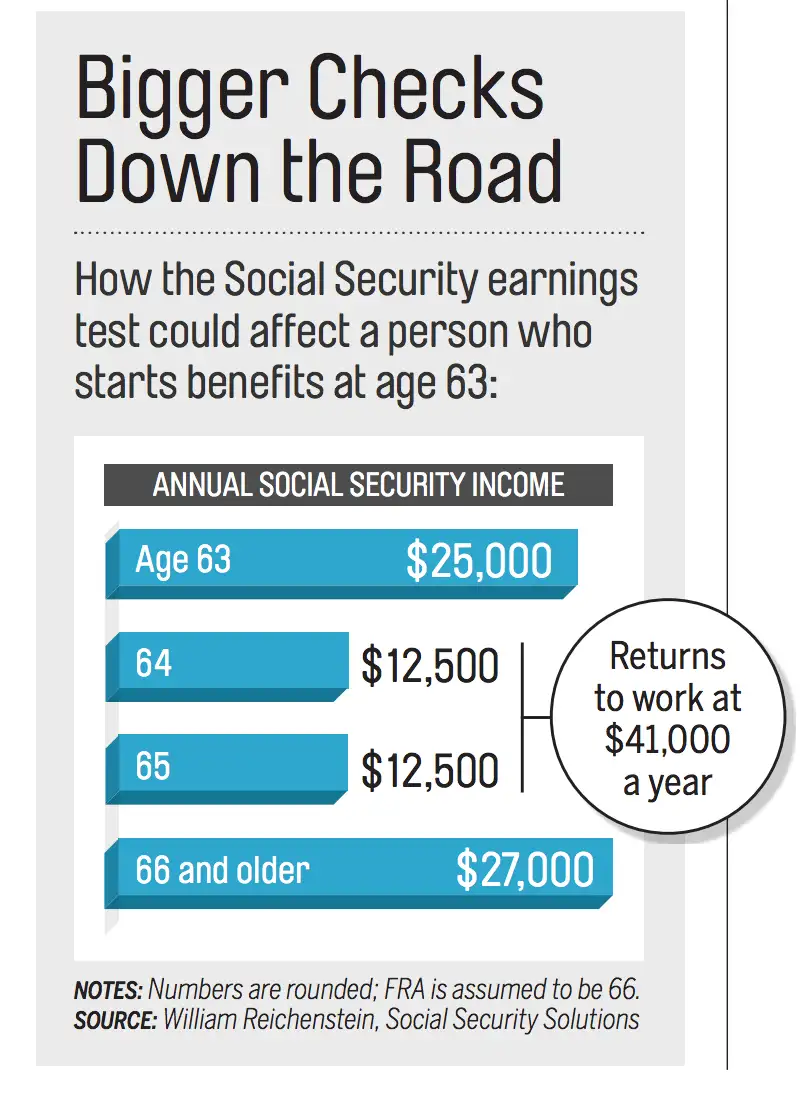

Say you claimed at 63 and got a yearly benefit of $25,000, before going back to work for two years at $41,000 a year. As the graphic shows, you would see a 50% benefit cut—but at 66, your benefit would be adjusted upward to $27,000 a year, says William Reichenstein, director of research for Social Security Solutions. Assuming you live till about 79, you will then have received the full amount that was withheld and still get a bigger benefit going forward.

Rethink your timing

If you applied for Social Security less than 12 months ago and then went back to work, you could withdraw your application and reapply at a future date. But to qualify for this do-over, you must repay all the benefits you have received.

Why do it? Your benefit will increase by 7% to 8% a year for each year you delay from 62 to 70. So it's generally best to wait as long as possible, says financial planner Jim Blankenship, author of A Social Security Owner's Manual.

Read: How Couples Can Get the Most Out of Social Security Now

Another reason to defer Social Security while still working is that your pay may make it more likely that part of your benefit will be subject to tax. That kicks in when a broad measure of your income—including interest on tax-exempt municipal bonds and half of your Social Security—exceeds $25,000 for an individual or $32,000 for a couple filing jointly.

If you are working and continue Social Security for now, you have another option starting at FRA: You can suspend your benefit and then start again, with a larger monthly benefit, up to age 70.