6 Secrets to Surviving Year One of Your New Business

This story is part five of a five-part series on the best way to launch your own business.

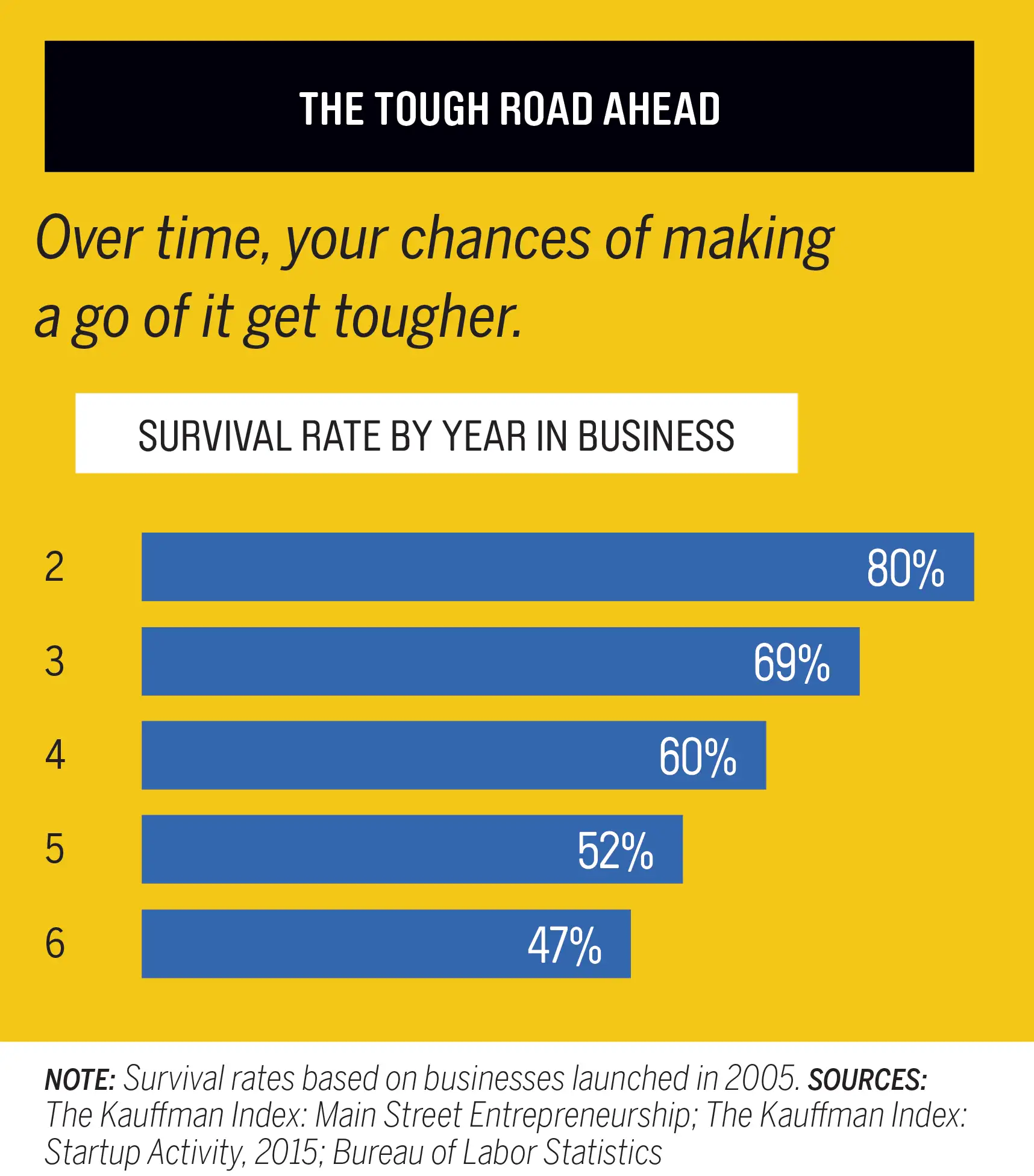

Reaching the one-year mark in a business often means mastering something that you won’t learn as a member of the steady-paycheck crowd: cash flow. “Running out of cash is one of the leading causes of small-business failure,” says Steve King, partner in Emergent Research, a firm in Lafayette, Calif., that studies the freelance economy. That can happen even if you’re at breakeven or profitable.

Staying afloat for a full year will let you make an educated decision about whether to soldier on or move on. Give yourself the best chance by taking these six steps:

Master the ebb and flow

Before you launch, ask others in the industry when you’ll typically be paid, and use that info to do a cash-flow projection, says CPA Lou Grassi, who advises many entrepreneurs as CEO and managing partner of Grassi & Co. If you have to wait 90 days, for instance, you’ll need to have other funds for overhead. Grassi, who started out serving construction businesses, quickly realized that his income would be concentrated in five months of the year. To even out cash flow, he came up with subscription pricing, breaking annual bills into monthly retainers. “A lot of customers liked it,” he says.

Surround yourself with smarts

On a tight beginner’s budget, you might be best off working from home. If you can free up the funds, though, you may find it helpful to rent an office that puts you in contact with an advisory team experienced in guiding startups. Co-working spaces are hubs for free agents where you can rent a desk or a small office. At an incubator or accelerator, which often provides office space as well as advisory services, you may be asked to pay rent or provide equity.

All give you access to mentors and learning from your peers, says Jack D. Beasley, managing director of the USC/Columbia Technology Incubator and senior program manager at the Office of Economic Engagement at the University of South Carolina. “They have gone through the same things you have gone through and can help you avoid mistakes.”

Fire money-losing clients

When you first launch, you’re eager for any business. But after six months or so, you’ll figure out that some clients aren’t worth it. If they don’t pay you enough to cover your time and costs—or don’t have a marquee name you can use as a calling card to win other business—replace them.

Tap credit cards sparingly

Fund as much of your growth as you can out of revenue so that you don’t build up debt that you can’t handle if the business shuts down. The safest route is to pay overhead out of savings or cash flow and defer big purchases until you have the money in hand, even if that means turning down an order.

With a small-business credit card, you will most likely have to offer a personal guarantee, so you could be stuck with the bill even if the business files for bankruptcy protection. Making small purchases on your card and paying them off monthly, on the other hand, builds up business credit with less risk.

Keep spreading the word

Perhaps you are getting the bulk of your work through word of mouth. Still, you need a website so that your operation looks legitimate. A site doesn’t have to be fancy, but if it is going to be an important route to new business, invest in advertising on search engines. Google Adwords has the highest conversion rate. The average cost per click in the U.S. is $1 to $2, according to Wordstream, a provider of online advertising tools. Raise your profile on major social media, such as LinkedIn, Facebook, and Twitter, by posting regularly.

Be willing to cut your losses

The history of entrepreneurship is filled with inspiring stories of people who ignored the evidence that their business was failing and achieved great success. But for mere mortals, there often comes a point when it makes sense to pivot. Set benchmarks you plan to meet when you start, says Beasley, and review them with a team of advisers or mentors regularly.

Take the tax man into account too. The IRS lets you deduct expenses from a business that is not turning a profit for only a few years—typically three, notes enrolled agent Crystal Stranger, president of 1st Tax in Honolulu and author of The Small Business Tax Guide. “After about two years in business is usually when I tell clients it might be time to throw in the towel,” she says.

If your business is in the red past the typical point when startups in your field become profitable—and you don’t take significant action to change your business model by, say, hiring a consultant—the IRS could deem it a hobby, which can trigger a higher tax bill. Remember: Even if this business doesn’t work out, it doesn’t necessarily mean it’s your last.

Read the previous stories in this series.